As more people look to retire early, more people are looking for shortcuts in order to reach early retirement quicker. Some hate their jobs so much they are willing to retire early and live in poverty!

Instead of retiring early to live in poverty or near poverty, wouldn't it be better to find a different job to live a more comfortable life? I think so.

Post-pandemic, I've made the argument early retirement / FIRE is becoming obsolete. No longer do we need to grind so hard and sacrifice to get out ASAP. Instead, there are now a plethora of new ways to earn money. Knowledge workers can now work from home without really having to work, as witnessed by the crowded pickleball courts during the weekdays. Why ever quit such a job early!

My goal for this article is to help you think about early retirement in a more healthy and balanced way. FIRE FOMO is real. Instead of feeling an intense rush to try and retire as early as possible, consider the alternatives.

- Find a more enjoyable job with better hours that pays less.

- Start a side hustle or side business that brings in supplemental income.

- Encourage your spouse to work longer or harder so you can take things down a notch.

- Take a sabbatical to recharge and rethink what you want to do with your life.

- Go back to school to change careers and take a break

Be careful sacrificing so much only to retire early and live a restricted life. And yes, I understand that retiring early to live in poverty can also be more eloquently called: Lean FIRE. But careful. Recreating the category of FIRE to suite your financial situation may simply be a coping mechanism.

My Original Desire To Retire At 25 And Poor

When I was 25, the September 11, 2001, terrorist attacks happened. This terrible event ignited my quarter-life crisis after only two-and-a-half years of working in finance.

I seriously thought about retiring with a ~$350,000 net worth and moving to Hawaii. There I'd be a fruit farmer on my grandparent's under-maintained farm. Due to a couple of lucky investments during the 2000 dot comb bubble and aggressive saving, I was able to amass a healthy net worth quickly for my age.

In exchange for clearing brush, watering trees, and doing general upkeep on the house, I could live for free in my grandparent's old house. Then I could make some extra income selling mangos, papayas, and pomelos down the street. The farm was only about eight acres in Waianae, a rougher part of town on Oahu.

For fun, I'd go surfing and hiking for free. Hawaii is truly a magical place once you have affordable housing.

A Modest Income And A Simple Life

Back in 2001, my $350,000 in investments could have generated about $17,000 a year in risk-free passive income. If I sold $10,000 worth of mangos a year, I'd have enough. Without dependents or rent to pay, early retirement is easier.

For three months, I daydreamed about living this simple early retirement lifestyle. Then one day I slapped myself silly and told myself to buck up.

Although having a nice tan and washboard abs would be sweet due to surfing every day, I wanted more. I wanted to see what else I could do with my education. In addition, I wanted to one day start a family with my girlfriend.

Throwing away a perfectly good career in finance so young was stupid. So I gutted it out for another 10 years until my investments could generate about $80,000 a year and cover my living expenses in San Francisco.

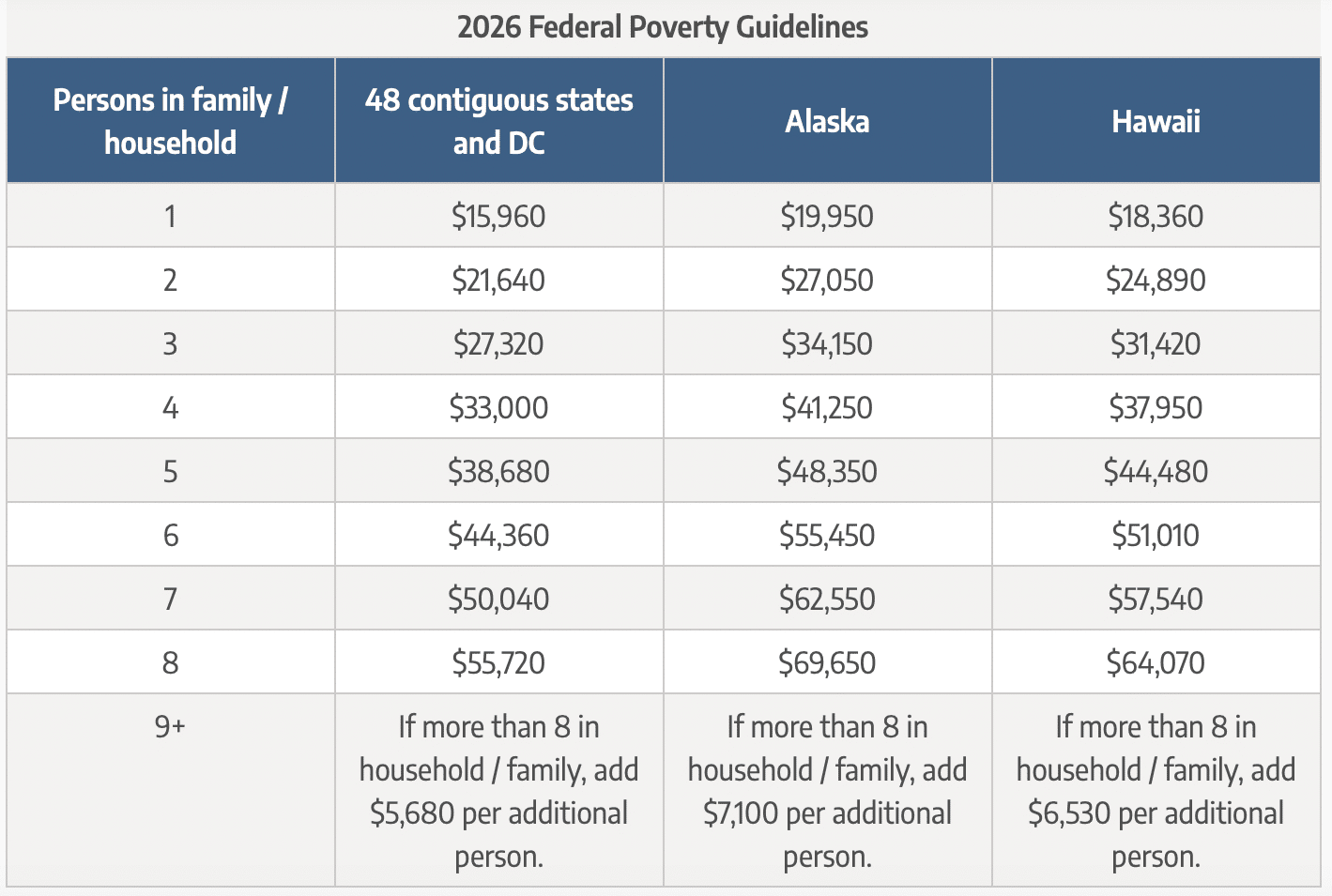

Given this post is about figuring out how much money is required to retire early and live in poverty, let's look at what the government's definition of poverty is.

The Federal Poverty Level Limits By Household Size

Below is the 2025 Federal Poverty Level (FPL). The numbers typically go up every year to track inflation.

In other words, in 2025 if you make $15,060 or less as an individual, you are considered the most impoverished. If you make $31,200 as a household of four, you are also considered living in poverty etc.

The more impoverished you are, the more you are eligible for federal government subsidies, such as healthcare subsidies. So long as your household income earns less than 400% of the baseline federal poverty level, you can receive subsidies. After a household income over 400%, you're on your own.

Minimum Amount Of Income To Feel Comfortable

The household income levels between 300% to 400% of FPL seem comfortable as long as the household doesn't live in an expensive coastal city like New York or Los Angeles.

For example, a couple with two kids making between $83,250 and $111,000 should be able to live a decent lifestyle in the heartland of America, where I've been investing in real estate since 2016.

The University of Texas, Austin, announced in 2020 that families earning less than $65,000 would not have to pay tuition. Meanwhile, families making up to $125,000 would also receive some type of tuition subsidy. Not bad!

Related: The Ideal Income Is The Student Loan Forgiveness Income Threshold

However, earning less than $111,000 as a family of four in San Francisco is tight. Rent for a three-bedroom house could easily cost over $4,500 a month in an average neighborhood. If you want to buy such a home, we're talking $1.5 – $1.8 million.

Note, I'm not here to argue which household income levels should receive extra assistance from the government. The government, with all its data and wisdom, is the decider of who is poor enough to receive assistance.

I'm here to highlight how big of a retirement portfolio you need to retire early in order to live in or near poverty, which the government and I define as 200% of FPL or less. Any household income under 200% of FPL seems tight, no matter where you live in America.

How Much Money You Need To Retire To Live In Poverty

Below is a chart I put together that shows how big of an taxable retirement portfolio you need by household size and percentage return if your household income is 100%, 150%, and 200% of the Federal Poverty Level limits.

Again, if your household income is over 200% of FPL, I no longer consider your household living in poverty.

As an individual, in order to retire early and live on a household income equal to 200% of FPL and a 4% rate of return or withdrawal rate, you would need to amass $679,500. In other words, $679,000 in taxable investments at a 4% rate of return is required to generate $27,180 a year in gross income (200% of FPL).

If you are a household of six and want to earn retirement income equal to 100% of FPL, then you would need to amass a $929,750 portfolio at a 4% rate of return or withdrawal rate. 100% FPL for a household of six is $37,190.

If a couple wants to have two children and earn up to 150% of FPL in early retirement, they need to amass between $832,500 and $2,081,250 in their after-tax portfolio based on a 5% to 2% withdrawal rate or return rate. A household of four earning 150% of FPL is $41,625.

Personally, I like to match my withdrawal rate to the risk-free rate of return so I never run out of money. Once you achieve financial independence, you never want to go back to the salt mines.

The Inconsistency Of Accumulating A Lot Of Money To Then Live So Frugally

The chart above shows the objective numbers required to retire early and live in or near poverty, as defined by the federal government. However, it is highly unlikely a household would be willing to accumulate so much capital just so they can stop working to live so poorly.

There are certainly exceptions. For example, one Financial Samurai reader who experienced money trauma did something similar. As an individual, she retired early with about $600,000 right before the bear market and relocated to Taipei from Seattle, where the cost of living is lower.

In general, something really has to be wrong with your job, your life, your physical health, or your mental health to make such an abrupt change in lifestyle. But that's life. Eventually, we all face hardships where we must make difficult choices.

Quitting the money can be very hard to do. And the more you make, the harder it is to quit!

Is It Worth Living In Poverty To Retire Early?

For the first 13 years of my life, I grew up in emerging countries like Zambia and Malaysia where I was surrounded by poverty. Some of my best friends in Kuala Lumpur would share one room and a bathroom with three other family members.

Seeing so much poverty for so many years made me focus on school because I was afraid of becoming poor. Fear, in my opinion, is one of the most important ingredients necessary for achieving financial independence.

When I came to America in 1991, I decided not to take my good fortune for granted. I hit the books, studied hard, got really lucky, and saved and invested as much of my luck as possible.

There are benefits of benefiting to retiring early to live in poverty though. And that could be a greater amount of happiness for longer. If you truly hate your job and are suffering, physically and mentally, retiring early without a lot of money may be worth it. Because greater happiness is incredible.

But I think retiring too early is dangerous, especially if you want kids in the future.

Unwilling To Live Near Poverty Just To Retire Earlier

Even though money doesn't buy happiness, we must earn enough to cover all our basic living expenses before we can really believe in such an ideology. I personally would not be willing to retire early if I had to live in or near poverty. Instead, I would just find a more relaxing job.

Although my work was extremely stressful for 13 years out of college, it enabled my wife and me to own a comfortable home in San Francisco, take 5-6 weeks of vacation a year, drive a safe vehicle, and raise a family.

For the now four of us to live on only $55,500 a year (200% of FPL) would require sacrifices. First, we may have to leave San Francisco. Second, we may have to start living with my parents in Hawaii to save on rent.

Although plenty of readers have stated they have no problem living at home with their parents as adults, we do. Our parents value their privacy. And after decades of living apart, we're all set in our ways.

Third, we'd have to pull our son from a Mandarin language immersion school. I actually wouldn't mind because there are some great Mandarin immersion public school alternatives.

Then we could also get free money to pay for college. Now that I think of it, make we should go into poverty sophomore year of high school for my son!

Ways To Improve Early Retirement Life

One alternative to living a more comfortable early retirement is increasing our withdrawal rate. But this is difficult to do because we've been in the habit of saving and investing for so many years.

The proper safe withdrawal rate in retirement is dynamic. Although it's easier to make more passive income in a rising rate environment, perhaps another recession is on the horizon. Hence, saving more aggressively may be more prudent.

The other alternative, which is what many early retirees do nowadays is freelance or take on side hustles to make up for any earning shortfall. It's always nice to make supplemental retirement income by doing something enjoyable.

Although we've lived entirely off our investments since 2012, I've been accused of not really being a retiree because of Financial Samurai. That's totally understandable, which is why since 2013, I haven't told anybody in real life that I'm retired. In 2022, I introduced the term, “fake retirement” to embrace the criticism.

But isn't it funny that if Financial Samurai was smaller, I'd get more approval from the Internet Retirement Police?

I can't help the size of this site. I just write whatever and let the search engines and word-of-mouth do its thing. The lesson is to never stick out because a hammer will try to bang you down.

Retiring With Poverty Income For A Family Of Four

If we didn't move in with my parents, here's what I think our budget would look like in early retirement. It is based on a household of four living on $55,500 a year, or 200% of FPL. Any passive income less than 200% of FPL would be too little. I'd rather keep working.

Looking at this 200% of the FPL budget actually makes retiring near poverty more doable. Although a two-bedroom apartment is smaller than our current house, we could make it work if our kids share a room.

We wouldn't have money to pay for sports, music, or art lessons after school. Thankfully, my wife and I would teach these activities to our kids. The pandemic gave us 18 months of homeschool experience. Further, I was a tennis coach and my wife knows how to play piano and the violin.

Staycations or road trips are fine for now since our kids are still young. Once our daughter turns five we plan to get on a plane and see the world.

If we were to try to live on $55,500 a year in early retirement, we would try to pay off our primary residence mortgage first. Once the property is paid off, living on near-poverty income is easier. We could spend more on food, entertainment, and travel.

Retiring Early To Live Near Poverty Is Feasible

After going through this exercise, I've concluded retiring early on an income equal to 200% of FPL is possible! Having a taxable investment portfolio worth nearly $1,400,000 to generate $55,500 a year in passive income provides a nice cushion. If you don't have kids, then retiring early is even easier.

But would you really be willing to live super frugally if you had $1,400,000? Again, it depends on how much you hate your job and your life circumstances.

My father-in-law retired in a cabin in the woods and is happy. He lives a simple life with no WiFi and clutter. His monthly expenses are just $500 – $700 on average. He's one with nature and isn't bothered by the hoards of people who live in a city like San Francisco.

Ideally, my family of four would need to earn at least 300% of FPL ($83,250) in early retirement to feel comfortable. At a 3% – 4% safe withdrawal rate, we'd need a portfolio of $2,081,250 – $2,774,000.

But man, having over $2 million is a lot of money! At this level, I would think I'd want to live it up more than what a 3% to 4% withdrawal rate lifestyle would enable. As a result, I'd continue to generate supplemental retirement income online by making money online and writing books.

Be Patient With Early Retirement

Instead of rushing to retire as soon as possible, go through the numbers and see if everything makes sense. To give up a well-paying job to live like a pauper is probably not ideal. If it takes less than 10 years of working to retire richer, I would go with that option.

One of my early retirement regrets is retiring too soon. I would have been financially better off if I had accumulated several more years of income. It's only after you've permanently left the workforce for a while that you realize how truly long post-work life is.

For those people willing to live in or near poverty to retire early, I say more power to you! Living a simple life without much desire or possessions is the key to enlightenment according to the Buddha.

If you don't have kids and want to FIRE, don't waste your precious money and energy doing things that don't build wealth! Not having kids is your FIRE super power! Kids cost a lot, but more importantly, take an enormous amount of energy if you want to care for them properly.

Be Prepared For Unexpected Expenses In Early Retirement

Just know there's a chance your expenses will increase as you age, especially the earlier you retire. Worst case, you can always just go back to work.

In fact, after buying a true forever home in 2023, we cut our passive income by $150,000. We are technically no longer financially independent and I will have to get a consulting job to make up for the shortfall. We could live on less, but we choose not to.

The math really doesn't lie, no matter how our emotions make us feel. If you can survive off poverty wages until Social Security kicks in, you're golden! Based on my calculations, living entirely off Social Security in retirement is possible!

At the end of the day, it's up to each of you to figure out what works best for you and your family.

Readers, would you be willing to retire early to live in or near poverty? Why or why not? What is the lowest FPL level you'd be willing to accept to retire early? How much money are you trying to accumulate to retire early? Do you think young folks retiring with the amounts in my chart are making a mistake?

A Conversation With Bill Bengen On Retiring Early

Bill Bengen is the creator of the 4% Rule, which recommends a 4% safe withdrawal rate in retirement to not die without money. Bengen now believes a 5% safe withdrawal rate is OK, meaning that we can lower the traditional retirement age from 65 to perhaps 55.

Related posts about retirement:

Living Paycheck To Paycheck Off A $5 Million Retirement Portfolio

Preparing For A 50-Year Retirement With Vanguard's New Return Assumptions

Coast FIRE: Another Term For An Employee Who Saves For Retirement

Recommendations For Retirement

Stay on top of your net worth with Empower, the web's #1 free financial app. Track your cash flow and x-ray your investment portfolio for excessive fees and inappropriate risk exposure. Then use its retirement calculator to plan for the future.

Also check out Boldin for even more retirement planning functionality. Boldin is 100% focused on helping you reach retirement and staying retired once you get there. My favorite tool of theirs is their Roth Conversion tool. It helps you model out how much money you should convert to save on taxes in retirement.

For more nuanced personal finance content, join 65,000+ others and sign up for the free Financial Samurai newsletter. Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009. Everything is written based on firsthand experience.

I thought the “original definition” of FIRE was to be able to remove your salary (i.e. retire) and continue the lifestyle that your salary afforded prior to retirement?

That was what all the initial teachings were about. They taught people to not always be upgrading their lifestlyes. Everytime you get a bonus or a salary increase, don’t upgrade your lifestyle. Maintain your lifestyle and save. Later, you should be able to continue to maintain your lifestyle, without your salary. That is FIRE.

It seems along the way, for a variety of reasons the “original” FIRE has been contorted by many. People desperate to retire early have come up with things like lean-FIRE. And now, on this very website, we have a story of the fundamental principles of FIRE also being broken – a significant upgrade to lifestyle, is now preventing FIRE !

We all need to get back to the basics and educate those out there without so much deviation from the initial principles of FIRE. And with that we can get back to teaching the average person the discipline and the way to achieve FIRE – right now a person learning all this for the first time would get horribly confused. Lean FIRE? Or hey, I will just keep upgrading my lifestyle, because that now seems to be what others do! NO, FIRE was about maintaining your lifestyle (not downgrading, nor upgrading), so that you could later stop earning an earned income and MAINTAIN your lifesyle. We really need to get back to the basics.

I thought the “original definition” of FIRE was to be able to remove your salary (i.e. retire) and continue the lifestyle that your salary afforded prior to retirement?

That was what all the initial teachings were about. They taught people to not always be upgrading their lifestyles. Everytime you get a bonus or a salary increase, don’t upgrade your lifestyle. Maintain your lifestyle and save. Later, you should be able to continue to maintain your lifestyle, without your salary. That is FIRE.

It seems along the way, for a variety of reasons, the “original” FIRE has been contorted by many. People desperate to retire early have come up with things like lean-FIRE. And now, on this very website, we have a story of the fundamental principles of FIRE also being broken – a significant upgrade to lifestyle, is now preventing FIRE !

We all need to get back to the basics and educate those out there without so much deviation from the initial principles of FIRE. And with that we can get back to teaching the average person the discipline and the way to achieve FIRE – right now a person learning all this for the first time would get horribly confused. Lean FIRE? Or hey, I will just keep upgrading my lifestyle, because that now seems to be what others do! NO, FIRE was about maintaining your lifestyle (not downgrading, nor upgrading), so that you could later stop earning an earned income and MAINTAIN your lifesyle. We really need to get back to the basics.

Wow- so at that income level your hypothetical family would only have to pay $60 in healthcare costs? Is that because you’d essentially get a big enough ACA subsidy to cover the majority of the cost on a deductible plan? Still surprised it’s that low!

It is a really unusual thought exercise you have gone through here. I’m sure it will be helpful to those thinking about FIRE. I read some of other bloggers who have FIREd and they talk about living on $45K a year and it always amazes how they can do it and still have an enjoyable life. They always makes me feel like I’m spending way too much in my retired life.

On the other hand, I read the FS and I feel I’m practically frugal by comparison. The important thing I stress is by comparison. We can’t help but compare ourselves to others in our community. I grew up in Shanghai in the 70s and we were three generations in a 2 room unit with no indoor bathroom or kitchen. With everyone else living the same way, I didn’t feel poor, I felt normal. I played with my friends and had a great childhood. I didn’t feel poor until we got to LA in early 80s and you start to see how others live.

Like you said, some people just want a simple life with simple pleasures and they don’t need a lot of money to achieve that. Your Hawaiian fruit farm life with your grandparents would sound like a dream to someone out there. We will be happier if we can manage our expectations and choose our comparisons wisely.

Yes, every lifestyle and desired lifestyle is different. And we are always at different stages of our lives as well.

I wouldn’t mind going to my grandparents food farm now and living a simple life with my family. Did so at 25 years old, I think I would’ve regretted not building my net worth larger to have more options later.

It’s always a balance and a race against time. The sooner we can find enough, the better!

Is there any article that describe amount you need to retire which is net of primary home equity? Most of your articles talk about net worth but it is a bit confusing as home equity can make up majority of it. I am trying to figure out how much you need to retire if you pay off your home already, both for early retirement and retire at average retirement age with social security.

Here is an article about target net worth amounts by age and work experience. You can include your home equity or not. At the end of the day, your primary home equity is valuable, and should be a part of your net worth.

https://www.financialsamurai.com/net-worth-targets-by-age-income-work-experience/

IMO, if you choose to retire early, good for you. However, if you retire early government benefits should be completely unavailable to you until you reach the appropriate age(s). Be self supporting, pay your own bills, have a great time. But you shouldn’t be able to retire when you can work and then have it subsidized by the government. That doesn’t pass the smell test.

Besides Social Security, what other government benefits shouldn’t be accessible? Health care subsidies?

I believe the original poster is referring to ACA discounted rates. For red, see the blogger Root of Good.

I’m currently living at 300-400% of FPL. I save the rest for retirement, a house (outside of my HCOL area) and three years of expenses. My hope is to be able to afford to completely retire and never have to work after retirement to make ends meet. Second option is to work part-time while retired.

I’d rather continue to work then retire and struggle to make ends meet.

I currently have enough saved that it is conservatively projected to keep me in the middle class (along with social security) when I retire. Saving for a house and three years of expenses are my next goals. Having a paid off house keeps expenses down. If it doesn’t make sense to buy I can spend more in another category. Three years of living expenses are a buffer for a bear market, or if I want to retire three years early. Once I’ve hit all three goals I’ll widen the three years of expenses to five, six, etc.

I’m also saving more in Roth 401K than Trad 401K now because my salary is high. This would let me shift to Trad 401K if my salary were lower and reap the tax benefits.

I haven’t been able to resolve the argument on Roth versus Trad. so I’m splitting my bets and balancing between the two.

Sounds like a good plan! Living off 300-400% FPL and saving the rest is a good balance. With a paid off house, living gets much easier.

I’m looking at remote working from overseas where 200 percent of the FPL is a upper middle class income. For reference I have no spouse or children and my relatives are all financially self-sufficient at this point in their lives. My plan is to invest the difference and semi- retire within 10-15 years but keep working as I genuinely enjoy my job.

The sad reality is to achieve that type of early retirement out lined in your chart you don’t have to work hard and save up. You can literally quit working and collect welfare and change almost every line item to government subsidized. When a guy at my office realized this he quit working and moved in with his parents. Not my preference but reality.

Hmm, I didn’t think about that strategy. Good point! Alas, I don’t think anybody really wants to go that path.

Everyday is a gift. When I entered the workforce in 1983 my goal was to retire at 55. What I found to be the real game changer was achieving financial security. Meaning I could go to work unencumbered. That allowed me to work without financial stress and actually quickly advance. Didn’t work week ends and was always home by 5 for the most part. Going to work became a lot easier and more enjoyable. I “fake retired” at 56 leaving my VP job and started consulting which was even better. I have no employees, mainly work from home (sometimes on the beach) and set my schedule. At 62 I am winding the consulting work down and increasing our travel. For me personally I found not focusing on the retirement day but finding a way to make each day better was the ticket. Financial Security helped!

Your article has certainly put quite a lot of people to think about the quality of their life post early retirement, including me. So much as to delay my retirement from 2 to 4 years when I am 42 years old. As I have gotten older, I do like a few finer things in life and less inclined to rough it in dorm rooms or hostels. An extra 2 years means a safe withdrawal rate of 2.5% post retirement for me as per some new calculations despite my increased new budget. Can’t wait for your next article.

Sounds like a plan, and 42 is still quite young! It’s the anticipation of retirement or doing something new that is very exciting.

Related: The Ideal Age To Retire To Minimize Regret And Maximize Happiness

Very true. I was earning $40K gross when I started my nursing career in 2008 and despite pay increases and overtime, I was still getting around $70K gross in 2019. Thankfully, doing up houses on the side and having flatmates helped my savings. Due to working 60+hrs weekly in Covid 19 areas in 2020-2021, it increased to $120K – $150K gross. Last year despite taking time off for health reasons, I still grossed $100K. I have only just now reached a decent payrate, and retiring now with a 4% withdrawal rate is not optimal. Instead working less hours, taking small holidays, working on my health and fitness while still taking advantage of 4 more years of free healthcare and retiring with a 2.5% withdrawal rate is the plan now. Your book which I have finished reading now also helped in making my decisions so keep writing please.

Will do. Congrats on working less and still making $100K! If you could spare a nice review of my book on Amazon, I’d appreciate it!

One big expense you forgot is health insurance. I think it unwise to go without that.

True. Luckily, as you’ll see in my post, the closer you get to 100% of FPL, the cheaper/more affordable your health insurance.

That’s the point. Why pay for health insurance when certain retiree’s can obtain free health care for life from their employer upon retirement for their self and their spouse and not pay for a monthly premium ever.

Wow, this article really got me thinking about the bigger picture when it comes to early retirement. It’s so important to consider not just the amount of money we have saved, but also the quality of life we want to live. Thanks for sharing such an insightful and important message.

Great discussion. If there’s one thing I’ve learned in my travels, it’s just how well off we are in the US even if we don’t feel it or appreciate it day to day. There are a lot of places in the world that have widespread poverty challenges. It’s very humbling.

There’s a post you’ve written about how you shouldn’t depend on anyone in retirement, especially the government. I think it’s the new 3-legged retirement stool post that talks about you, you, and you. I totally agree with that philosophy and certainly don’t plan on social security being there to support me when I’m of age. If I do collect, fantastic! But I’m not counting on it.

I don’t want to retire with money stress so I won’t fully retire until I’m confident I can maintain my lifestyle through passive income and then later live off of my retirement accounts.

I am glad you brought up the realities of living in another country. I find it quite short sited when people think they will just leave America with their American funneled resources, buy a little place somewhere and lived the dream. What they fail to appreciate is both a historical perspective and a current perspective. No other country has provided the level of safety as America in the last 100 years. By that I mean property rights, bill of rights, economic prosperity and peaceful transfer of power. In the 70s countries were still nationalizing property all over over the world. That means, you may have bought the property and the government simply takes it from you. Sorry, you lose. Two years ago, I fell in love with Cusco after hiking the Inca trail. Today, it is closed to all tourists and bordering on outright violence. Don’t get me started on House Hunter’s International contestants buying land in Mexico. I was reading articles about Eastern Europe being the under discovered paradise of retirement. Not so much now as refugees poor into Poland, Prague and Greece nearly destroying those nations.

Many talk about living the dream outside of America because of all its issues but America as a leader of the world pays a HUGE price to provide an unprecedented umbrella of peace. We are not perfect. We need to do better in many areas. But democracy is messy. Our last earthquake saw 165 fatalities. Compare that to the earthquakes in “paradise” southeast Asian countries. That is because we have strong governmental with strong regulations. When my little boy had a fever of over 105, I drove him three blocks away to immediately get the medicine he needed. None of it was tainted. He did not get an infection from the hospital. I thanked God I lived in America.

So make your own decisions but don’t fail to appreciate the unprecedented luxury even those living in poverty level have in America – clean water, paved streets, public education with free food programs. Maybe if people were grateful for that they would be willing to work a little longer to continue to put back into the kitty so the next American generation can enjoy the same.

I think Coast FIRE is an attractive way to ease into your financial independence lifestyle. Once you’ve hit FI, you don’t have to save for retirement anymore. You can work just enough to sustain your life. The pressure is off to save for retirement. You can do something you like, keep your mind sharp and engaged, and you will still have structure to your life. Personally, this is how I’m living right now.

Currently, we spend about 200% FPL and live a pretty comfortable lifestyle. It really depends on how you set up your life. Our housing and transportation expenses are much lower than the average household. This frees up our resources to spend on travel and various other niceties.

I think you can have a comfortable early retirement on a smaller budget if your house is paid off. That’s a huge part of the cost of living.

Can someone please clarify:

If you have a million in assets (or probably just a few thousand), you can draw that 4% poverty income off your portfolio, but it would disqualify you from any benefits.

If you really want to live off of this level of income, you’re better off having no accumulated wealth.

This sadly demonstrates why in many cities you’re better off being city supported poor than working and middle class.

I know a zoomer who decided to work less and take advantage of this fact. He just got reduced internet, food stamps of roughly $450 a month plus goes to the food bank every week, goes to the pet food pantry, gets a free gym membership, and just told me yesterday he had not paid his utilities since spring and got an emergency program to pay off over $1000 in utility bills for him-which apparently he can do twice a year. He also qualifies for LEAP to get his utility bills reduced. He’s looking at other benefits like the savers credit .The city will give him a sales tax rebate once a year since he is on food stamps. All up, the benefits he receives will be worth around $1200 a month. He is also on a waiting list for UBI if it ever gets implemented.

I wonder how many people have figured this out and are working less? I think it’s sad to give up on your life in your 20’s and take this route, but for some people who feel they will always be very middle class and not a tech bro with an outsized retirement account, he has retired at poverty level in his 20’s without having to save anything.

“If you have a million in assets (or probably just a few thousand), you can draw that 4% poverty income off your portfolio, but it would disqualify you from any benefits.”

This is incorrect. Your government benefits largely depend on the income you generate, not your wealth. This is one of the reasons why multi-millionaire retirees can still receive healthcare subsidies. Several personal finance writers do exactly this.

There is a name for what your friend is doing: parasite

Being Coast FI with some cushion is freeing in itself. You can relax a little, save a little less, but definitely keep adding to that portfolio! We are in our mid 40s and phasing down; after 5 more years of working and saving, then husband will step back and downshift. I only work 30 hrs so I will keep doing that til I don’t want to any more.

Agree. And I like the plan! I think around 45 is the best age to retire or take it down. You guys will truly enjoy taking things a little easier.

I’ve found working 15-20 hours a week is my sweetspot.

> In general, something really has to be wrong with your job, your life, your physical health, or your mental health to make such an abrupt change in lifestyle.

Lots of positive reasons to move overseas – adventure, family, sunshine, higher quality of life. Something doesnt have to be wrong.

Good post. Agree with your thoughts on ratcheting back or switching jobs rather than calling it quits totally. Like the Viking Spirituality: inevitability of death and misfortune should (will) not paralyze us.

I think more credit needs to be given to “Fake Retirement“. Why do you think people with jobs like supreme court justices, bloggers, sports analysts, professors, etc.., work so long? Because: 1. They have a low-stress job, 2. They, most likely, love what they do, and 3. They most likely don’t have to put in a whole lot of hours to do the job.

All the retirement experts advise us to do SOMETHING after we retire, right? They say it’s good for your health. Then, being a Blogger isn’t your job, Sam. I think it’s more of your retirement project. It just so happens to pay you very well. That’s how I look at my “fake retirement” job. I went from working 70 hours a week on my pre-retirement job, to now working on average 15 hours a week on my post-retirement job. And, although it doesn’t pay what my first job paid, it DOESN’T HAVE TO.

I think Fake Retirement is the way to go….IF!! your fake retirement includes have a low-stress, low-hours “job”.

Correct. Retire to something, not just from something.

Being able to do something you enjoy doing after retirement and getting paid for it is seriously the best combination. Because for many of us, we would do these things for free for a list a number of hours a week.

What you say about 15 hours a week is actually right in my target zone for how many hours I want to spend writing and spending time on Financial Samurai a week. The maximum number of hours is 20 hours a week. But if I could do 15 hours a week, by averaging 2 to 3 hours a day during the weekdays, and two hours over the weekend, that is ideal.

What is it that you are doing post retirement for 15 hours a week?

I teach online. I kind of fell into this gig. It started out as a traditional job, but the pandemic changed everything. Now most adult (graduate) students want to take their courses online only. I just happened to be in the right place at the right time.

As you’ve said before about getting wealthy, I was extremely lucky.

Great thought exercise! I love to plan and run different scenarios before making big decisions. Looking at how we could adjust and adapt to different financial situations in retirement is fun and a helpful way to reaching an ideal reality in the future. I’ve never regretted being a bit over prepared for big decisions and changes in my life, but I have regretted being under prepared. Thanks for the helpful insights.

I have enjoyed your blog for many years. I hope I can express my thoughts in the right way.

You stated: “Any household income under 200% of FPL seems really tight, no matter where you live in America. I’m confident all of you agree.”

I have to disagree with this statement. In fact, I disagree with a bit more as well. Please allow me to explain:

I live in a relatively low cost of living area, but not as low as, say, the Midwest. (For example, median homes – 3000 sq ft – are going for about 450k where I live right now.) My wife and I have 4 children, and so for us, 200% of FPL is $74,380.

I work for a small college, and we are not all that well compensated (salary is still under 60k) despite a decade of teaching. Due to health situations with our youngest son, my wife is unable to earn consistent income. So we have learned to make do on just my income.

The biggest key is to be wise with what you have. And what we have is time. A career in teaching is not a good way to make a lot of money, but it does give you a lot of flexibility. I have learned to be a jack-of-all-trades, which saves me a lot of money. Thankfully, I enjoy the breadth of education and skills that comes with it. Home remodels? Materials are the only cost in cash I pay. Carpentry, electrical work, plumbing, drywall, etc.. are all doable if you take the time to read and watch videos and chat with your local building authorities, and learn by doing. Car repairs? As long as it is not a transmission job or major engine overhaul, I’ll sort it out. Cost of food? Basic staples are not that much money, if you take the time to cook yourself, which both my wife and I enjoy. Travel? Locally, you can do a lot on foot or by bike, but if you must take a car, our 05 Civic still gets great gas mileage. Education? I don’t think public schools are all that great, but when you take the time to supplement at home by encouraging reading, math problems (for fun!) and other engaging learning activities, I think our kids are going to do just great. Recreation? We live by and love the great outdoors. Camping in beautiful places beats a theme park hands down, as long as you have a little fortitude.

With this approach to life, I am able to max out my 403b at work, which is on top of a 14% automatic pension. I also max out my Roth IRA most years. Thus, we are really living on closer to 30-40k/year. I don’t know if I’m ready to claim financial independence yet, but I am close, and am not yet 40. But I won’t have $6-$8 million portfolio when I do. I think living off of approximately $40,000-$45,000/year (inflation adjusted) will be perfectly manageable.

Honestly, I may end up continuing to work for a while. I’ve not found a vision for the other thing I’d rather do that isn’t what I’m doing now. But it would feel great to be doing so while knowing that I am FI and could walk away at any point.

The best part to me in all this is that just about all of these things are great teaching moments for your kids. They learn to be hard-working, problem-solving, creative-thinking, money-conscious individuals. I know our life is not for everyone. And I definitely don’t recommend jumping from a more extravagant life to a frugal life cold turkey. But I do want to offer the perspective that frugal living is more than consigning yourself to a miserable life in abject poverty.

Thanks for the feedback! Towards the end of the post, where I put together a budget for a household of four, I mentioned that I agree about the feasibility of living off 200% of FPL. It helps to see the numbers, pay down debt, and earn supplemental retirement income.

“ Honestly, I may end up continuing to work for a while. I’ve not found a vision for the other thing I’d rather do that isn’t what I’m doing now. But it would feel great to be doing so while knowing that I am FI and could walk away at any point.”

This part of your comment you make is actually very important though. Because thinking you can retire officer in an amount is different from actually pulling the rip cord and living off a certain retirement amount.

You have to overcome your fear and make a change. Otherwise, as I discuss in this post, is your financial independence number real? FI is about having the confidence to change your life for the better, whatever that means.

Something to think about!

Hi. I am 73 and work 25 hours/wk as a lawyer. My dr. told

me “Chuck keep going.” Maybe, you could write an article about not retiring. I would NOT want to retire and then worry about money. To each their own.

Glad you’re still working. And it’s also good to hear you’ve overcome your previous health issue to be able to keep working.

Just discovered your blog. Great content. I totally feel this post. I’ve worked since I was 14 (56 now) and don’t want to live in poverty in retirement after saving/investing since I was 27. If I have to move to another country, I will, but I will definitely live my best life. The world is my country. I’m FI in my location (rich in a few other great countries) but still work because I enjoy it and I’m good at what I do. I tell friends that I have the best part-time job because I telework most days (since COVID) and it’s stress-free. Not having financial worries is the best feeling. I vacation, spend time with my daughter, stay fit, indulge in my hobbies and enjoy my social life…all financed by my salary while my investments continue to appreciate. I’m very grateful for what I have and my station in life. Life is good.

Welcome! And I’m glad life is good.

Don’t mean to brag, but I live in a simple12x12 “cabina” in Central America by a jungle creek with a queen size bed, hot plate, refrigerator/freezer, microwave, flat screen tv, cable, WiFi, a fan, I have a sweet little swimming pool to cool off in and view the sun setting over the ocean any time I want, I’ve got a mountain bike I can hop on to go to one of THE most beautiful beaches in the country anytime I want, I can use the bus, Uber or taxis when I want, I can get fresh pineapples for a buck and change, coconuts (LOVE coconut water for a recovery drink after a good bike ride) for about fifty cents, avocado for around the same, I get to see and hear parrots and all kind of cool jungle birds every day, the only I have to do when I wake up in the morning, is decide what I want to do that day, and I’m doing it on (drum roll please)….wait for it….1200 bones a month from social security. Ahh, it’s a life but somebody’s gotta live it :-)

That sounds awesome! I want to do something similar when I’m that age.

My friends dad died in Central America more than 5 years ago… They’re still trying to get his body and give him a proper burial.

Congrats….but no thanks.

Bruce you’re living my dream! Are you in CR? Send us some pictures of the abode. I would love to make that move but getting resistance from the mrs.