After four months and one week, I finally was able to refinance my primary residence mortgage! I went through the hardest mortgage refinance ever. And with rates elevated, refinancing a mortgage will continue to be hard for many.

I originally wrote this post in 2019 to chronicle the difficulty of my mortgage refinance journey. In 2025, refinancing a mortgage continues to be difficult as lenders are being stringent with whom they approve after the boom years during COVID.

The Hardest Mortgage Refinance Ever

My original loan was a 5/1 ARM at 2.5% that began on August 1, 2014, and reset to 4.5% on August 1, 2019. The loan amount was $990,000 and the payment was $3,920 a month.

My new loan is a 7/1 ARM at 2.625%. The loan amount is $700,711 and the new monthly payment is $2,814.41. There was no cost to do this refinance. In fact, I was paid a $220 credit.

A $1,105.59 monthly cash flow improvement helps counteract new preschool and healthcare costs. But it's not enough, which is why I need to find new ways to save and make money.

My ultimate plan is to pay off our primary residence by October 1, 2026, and never get another mortgage again. Mortgage rates would have to drop another 0.5% for me to even consider going through another refinance.

This refinance was my hardest mortgage refinance ever due to the time it took, the various curve balls faced, a self-inflicted wound, my general frustration with an unfamiliar lender, and a very snippy title officer.

But it's over now and I wanted to share some takeaways to potentially help you make a better refinance decision.

Low Interest Rates Make A Big Difference

When you refinance a mortgage, you often reset the 30-year amortization schedule back to zero. Therefore, if you want to pay off your mortgage based on your previous amortization schedule, you'll need to pay extra principal on top of your normal monthly payments.

What you'll notice from my amortization schedule below is that despite the reset, 46% of my payment goes to paying down principal. Not bad. This is interesting because you always hear that during the initial years, most of your mortgage payment goes towards paying interest.

In fact, by year four, the split between principal and interest reaches parity. And by year five, a greater percentage of the mortgage payment goes to paying down principal than it does to interest.

If my mortgage rate was at 4.5%, my monthly payment would be $3,550 instead of $2,814.41. But $2,628 of the $3,550, or 74% of the payment would go towards interest. By historical standards, 4.5% is not considered a high mortgage rate.

In other words, refinancing when rates are low not only improves your monthly cash flow, but also significantly boosts the percentage of your payment going towards principal. It's like getting a two-for-one special. Well-qualified borrowers are getting much lower mortgage rate offers than headline averages.

Once you've successfully closed on your mortgage refinance, request your amortization schedule to crunch your own numbers. I plan to pay down $80,000 a year in extra principal to have a zero balance by 2026.

Lenders Are Still Extremely Strict

Both Citibank and Wells Fargo told me that in order to get their best mortgage rate, I would need an 800+ credit score.

When I got my last mortgage in 2014, Citibank said 760+ was good enough to get its best mortgage rate at the time.

I've always been generally aware that lenders had gotten stricter since the financial crisis. However, because of a huge bull run, I hadn't expected my banks to be that stringent.

Even after squeaking by with an 804 credit score, both banks still put me through the wringer by requiring an enormous amount of documentation.

I say both banks because I initially spent two months trying to refinance through Citibank. However, after Citibank made it clear it wouldn't be giving me the lower rate it originally promised, I cancelled 10 days before closing with no penalty.

This is the self-inflicted wound I mentioned. But it was done out of principle and a little bit of stubbornness.

A Long And Uncomfortable Mortgage Refinancing Process

In other words, my entire mortgage refinance process really took over six months to complete!

Although I was still vetted like a suspected spy in FBI custody, it felt good knowing that both banks had been extremely thorough with my finances. If banks were this thorough with me, then they must also be extremely thorough with other mortgage applicants as well.

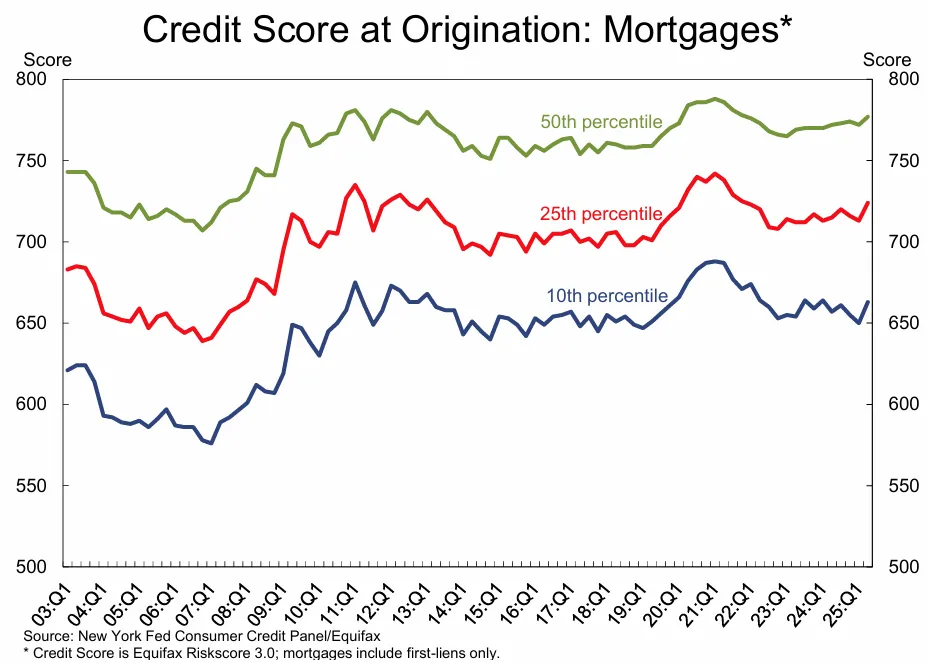

We know from the latest New York Fed data that the average credit score for approved mortgages is ~760. Based on my latest refinance saga, I absolutely believe it.

Given the stringent standards used to qualify someone for a mortgage between 2010 – 2019, during the next downturn, I just don't see the same amount of carnage for the housing market. Sure, we might see 10 – 20% corrections, but not the 30% – 50%+ corrections we witnessed during the last financial crisis.

Finally, both Citibank and Wells Fargo required me to have an 80% loan-to-value ratio or lower. In other words, I needed to have at least 20% equity in my home after independent appraisers did their evaluations.

My Title Officer Just Shipped It In

The weekend before I was scheduled to sign all the documents, I discovered the title company was expecting me to pay $9,662.43 at closing. Just looking at the number didn't make sense because my monthly mortgage payment, including principal and interest, was $3,970 at the new reset rate.

I first had the mortgage officer explain the big number. Then I had the title officer basically rehash what the mortgage officer wrote, even though they were both on the email chain. Both of them stuck by the numbers even though it was obviously wrong.

Luckily, I did the math and made them realize they had double-counted one month's worth of mortgage interest which I had already paid. A critical mortgage mistake. They also were using an old payoff statement which had a higher balance. They missed this key point because the refinance took so long.

This frustrating incident made me realize that some lenders and title company officers aren't aware of their own errors or really don't care. So long as you pay them more at closing, that's what matters. Further, this incident made me realize now handicapped borrowers are when it comes to understanding all the numbers. No wonder why so many homeowners got in so much trouble during the last downturn.

Took So Long To Fight To Pay The Correct Amount

I had to spend at least an hour researching the numbers and calculating why they were over-charging me by at least $4,551.26 at closing. And once I mathematically got to the bottom of the overage charge, they didn't even apologize.

Instead, the title officer was actually annoyed she had to redo the final refinance statement and said, “I do not work weekends” even though she sent the initial final statement on a Friday afternoon and expected me to sign the documents by Monday morning.

If you don't work weekends, don't do this. The title officer was pressuring me to go through with the signing even though I was uncomfortable with the numbers. The title officer was also like the teacher in grade school who made you feel bad for asking a question.

If you do not understand the numbers, do not sign the documents! Ask for a clear explanation. You have a right to understand!

Ultimately, I was able to reduce my payoff at closing to $5,111.17 from $9,662.43, a significant $4,551.26 difference.

This experience might shed light on why there is mortgage fraud happening by borrowers all the time. To get a mortgage at the lowest rate, borrowers need to jump through so many hoops.

A No-Cost Refinance Still Costs Money At Closing

Although my mortgage refinance cost me no money, I still ended up writing my new lender a check for $5,111.17. Sounds like a lot for a no-cost refinance right?

So what is going on when a homeowner who finishes a no-cost refinance still has to pay thousands of dollars at closing? For the uninitiated, it may seem like the lender is trying to rip you off with some sneaky fees. Perhaps the lender is thinking that you'll acquiesce since, after so many months, you're so close to the finish line.

I had some similar concerns, especially when the title company wanted me to write a $9,662.43 check at closing. But rest assured, the lenders are not trying to rip you off, at least not directly. By law, the lender has to refund any overage to you within 30 days.

Let me demonstrate using the final fee schedule of my loan as an example so you can see all the refinance costs and credits for yourself.

Mortgage Statement Analysis

As you can see from the final refinance statement, there are a lot of fees when it comes to refinancing a mortgage. The only fee that could have been avoided if the bank had been more efficient, is the $875.89 Rate Lock Extension fee.

The credit of $6,131.22 covers all fees plus gives me a $220 balance due. The reason I had to come up with a $5,111.17 check at closing was due to:

- Having to pay the entire year's homeowner's insurance premium of $1,267.05.

- Having to pay $3,844.12 in mortgage interest at 4.5% from 9/1/19 – 10/11/19. The statement says I only owed $3,464, which is why I have a $220 balance due.

Therefore, the $5,111.17 is money I owed anyway. I had previously elected to pay my annual homeowner's insurance premium in monthly installments at no extra charge. But in order to refinance, the law requires the annual homeowner's insurance premium to be paid in full.

Where the refinance delay cost me was paying a 4.5% interest rate from 9/1/19 – 10/11/19 instead of a 2.625% interest rate. I ended up paying $36.14 more in interest a day for 41 days, which totals $1,481.74.

Not anticipating two rate extensions was a critical miscalculation on my part. I naively trusted the loan officer's guidance of getting the refinance done within 2.5 months.

On the positive side, I still get 84 months at 2.625% on the back end starting on 10/11/2019.

If you have an ARM, the lesson is to try and complete your refinance a month before it resets rather than after it resets. Further, if you're close to completing your refinance with one bank, like I was, calculate the potential overage charges before you decide to go with another bank.

You will most likely also have to come up with cash at closing for your no-cost refinance, so be prepared.

Don't Make Any Large Financial Changes

During your refinance process, don't make any sudden and large financial changes. These include:

- Buying a car

- Making a big investment

- Big deposits or withdrawals

- Credit inquiries

- Change your income

- Change jobs

- Lose your job

- Changes to your revocable trust

Expect every single financial move to be scrutinized during the normal refinance window. If you end up having to extend your rate lock, then you need to be extra careful.

With each extension, I had to send new bank statements and brokerage statements. After sending new statements, I was then asked to explain a number of transactions.

In one e-mail from the mortgage officer, he asked me to explain 36 transactions that occurred in my checking account and savings account. These transactions included credits from my 18 real estate crowdfunding investments, capital calls for a couple private equity and venture debt funds, expense reimbursement checks, and various credits that came in from dividends and asset sales.

My stress continued because I had to get another credit check because the original one's validity expired after two months. This created unnecessary anxiety because I needed to get over an 800 again to keep my 2.625% rate. As some of you know, multiple credit inquiries in a short period of time can hurt your credit score. Luckily, my score came out the same at 804 again.

Refinance For Financial Flexibility

Several folks have asked why didn't I just pay off the $700,711 mortgage since I transferred over $1,000,000 to Wells Fargo to get the relationship pricing rate. I'd still have $300,000 leftover to invest.

When I thought I could only refinance at 3%%, I strongly considered paying down the mortgage to $500,000. Once I was able to get the mortgage rate down to 2.625%, however, I felt the rate was too low to pay off, especially since the yield curve was inverted.

At one point during the refinance process, I was able to get a risk-free 2.5% on my cash by opening up an online savings account or buying a 3-month Treasury bond. Although the cash rates are lower now, the difference is so narrow it made aggressively paying down the mortgage a suboptimal move.

Besides, I didn't have $700,711 in cash lying around, only about $200,000. I would have had to sell $500,000 worth of securities and pay taxes, which is always a downer.

I wanted to have more flexibility with my money by not sinking so much into our primary residence. If there is a recession on the horizon, I want to have enough cash to buy stocks, rental property, or commercial real estate somewhere in the heartland.

Finally, if I change my mind and want to aggressively pay down the mortgage I still can. Given the refinance didn't cost me money, I was giving myself maximum flexibility.

Always Take Action To Save Money

Although my latest mortgage refinance was a real PITA, I'm glad I went through with it.

Not only was I able to write a series of educational posts to help readers make better mortgage refinance decisions, but I'm also going to end up saving over $90,000 in mortgage interest expense over seven years.

Refinance your mortgage. Refinance your student loans. Take advantage of 0% APR credit card offers if you need a reprieve. Avoid borrowing money for a car. As we face an uncertain economic future, now is the time to take advantage of lower rates to strengthen your cashflow.

Invest In Real Estate More Strategically

Real estate is my favorite way to achieving financial freedom because it is a tangible asset that is less volatile, provides utility, and generates income. Stocks are fine, but stock yields are low and stocks are much more volatile.

The combination of rising rents and rising real estate prices builds tremendous wealth over the long term. Meanwhile, there are more ways to invest in areas of the country where valuations are lower and net rental yields are higher thanks to crowdfunding.

Check out Fundrise, my favorite private real estate investment platform open to all investors. With an investment minimum of only $10, it's easy to diversify into real estate and earn more passive income.

The real estate platform invests primarily in residential and industrial properties in the Sunbelt, where valuations are cheaper and yields are higher. The spreading out of America is a long-term demographic trend. For most people, investing in a diversified fund is the way to go.

I've invested ~$1,000,000 in private real estate so far, with over $400,000 in Fundrise, a long-time sponsor. My goal is to diversify my expensive SF real estate holdings and earn more 100% passive income. I plan to continue dollar-cost investing into private real estate for the next decade.

Why don’t you do a 30 year fixed instead and lock in the low rates vs the arm approach?

Glad you got through the process!

Thanks! Main reason is because I don’t want to pay a higher rate than necessary for the duration I plan to own or pay off the mortgage.

See here for more details: https://www.financialsamurai.com/why-an-adjustable-rate-mortgage-is-better-than-a-fixed-rate-mortgage/

That’s terrifying that they were charging you so many unnecessary fees.

Good on you to notice. When closing a loan there is always so much going on that you really want to just assume the numbers are right.

I’ve had some late nights going over numbers or legal agreements to make sure I didn’t get duped. I don’t think I have so far :|

Just closed on a jumbo (2m) with BOA/Merrill about 2 weeks ago on a second home. 7/1 @ 2.125% with a lender credit of $7k.

They were a pain in the ass to work with.

Couple things:

1. Your credit score isn’t the same as what u pull from the 3 major credit providers. Banks have their own algorithms they use to determine your score, which is usually about 20-40 points higher than the banks.

2. If you’re buying a house go down the path of a loan almost to the very end simultaneously with more than 1 lender. It might cost you 2 appraisals but the last thing you need is the prospect of losing a deposit plus the banks will get their crap together if they know you can switch at anytime.

The best rate I seem to be getting on a 940K jumbo loan for a 7/1 arm is ~3.5% with ~740 credit score. Is this considered a good rate or average rate? Although its no point refinance – I still have to pay around ~4K after appraisal ($600) and closing costs. Its a streamline refinance. How are you guys getting ~2.65% 7/1 arms?? Is it because of credit score >760 or because its a conforming loan amount? I’d love to know so when I refi again in 6 months.

Best rates require 800+ at many lenders.

Also, I used relationship pricing.

https://www.financialsamurai.com/the-difficulties-of-relationship-pricing-when-refinancing-a-mortgage/

Sam – Definitely feel your pain. We are “only” 2.5 months into our refinance and despite negotiating a fantastic rate (2.875%, 30yr on $1M remaining,) our rate lock expires end of November so we are very anxious about not finishing before then, or that the bank may be intentionally stalling as rates have gone up. Hard to believe everything the loan officer says.

*Update* – we finalized with BofA this week after just over 3.5 months, exactly on the day our rate lock expired. To protect ourselves , we didn’t back out of the competing lender’s process until the very last minute – their rate lock (3.125, 30yr) went until end of Dec and we kept pushing appraisal out (which they refunded today since it never happened). Net- Net completely miserable process, but worth it for such a great rate.

Congrats!

Thanks for the post Sam, why is your credit score so low? That was the one thing that stood out to me in this post…you being worried about your credit score. I am 38, own 3 properties (multiple refi’s of each one) and have had a bunch of credit cards over the years. I can honestly say my credit score has been 813-825 for the past decade or more. It has not been difficult to keep an extremely high credit score as long as you make your monthly payments every month without fail and keep a couple accounts for many years.

I have an amazing net worth of $500,000, which is huge for my age.

Not sure. Have you found yourself getting better rates at 813+ versus 804?

I was worried about my credit score taking a dip after getting my credit pulled so soon again due to the delay.

Any tips for helping me improve my poor credit score? Maybe it is an age thing given credit history is a big factor. How old are you and what is your estimated net worth? Those two factors might make a difference.

For some reason, I feel pretty great with my credit score though. Not sure why. Probably bc I got through the refi and don’t plan to do one again for a while.

When I was 35, I had a net worth of $3.5 million. I only had a 802 credit score too.

Perhaps you’re obsessing on the wrong score.

We are doing a streamline and they have told us at least 10 different prices for closing. They cant even give us a closing date as an fha case number hasn’t been assigned. They told us 2300 to close when we started. Now they say its 3100 on paper but over the phone it’s still 2300. They are telling me I have to sign that closing doc that says 3100 and are pissed because I refuse to sign it with the wrong amount on it.. if it said estimated or approximate, I would sign but it’s a definitive number. So nope! Streamlining is supposed to save us 48k over the life of the 30 year fixed loan. But my plan is to have it paid in 10. We have a bunch of equity but cant access it due to us being self employed. I wanted to utilize it to by investment properties but looks like I’ll have to do that the old fashion save my money way.

By law, they are supposed to refund you your overage charge within 30 days I believe. But yes, it is extremely frustrating to have a wrong closing pay off amount.

Glad to hear you closed. Quick question, how did you rate shop? Did you call up a couple of institutions you were familiar with or use a website that compared rates?

I often search online for the latest rates, then I see if the lender with the mortgage can match or beat, and then check with another bank I do business with. With my latest mortgage, a reader highlighted the WF relationship pricing deal.

Just need to shop around.

Sam I love the case studies. They are helpful in understanding the concepts and the process/details. Keep ‘me coming! My wife and I are long time renters living in CO. We just welcomed our first child into the world on Monday and hope to buy a home here by spring next year. Planning to pay in cash in order to reduce our annual spend. Crazy to think >50% of our $55k/yr spend goes to rent I appreciated u describing in previous articles how u use docusign to make offers and negotiate with sellers. Could u recommend any resources where we could learn more about the negotiation process for buying homes? We are flexible on location due to my remote job, so we are hopeful to snag a great deal but need to learn more about the home buying negotiation process as we check out neighborhoods in the Denver metro area. Thanks and best wishes to u and ur family. Been reading ur blog since 2011 and really grateful u decided to keep at it post the 10-year mark. I hope to create a side hustle when I FIRE in a few years in order to teach my children there’s more opportunities out there than just corporate gigs.

Current Net worth=$1.1m with $800k in brokerage Acct. Hoping to buy home for $400-500k and then transition out of full time work within 3 yrs (age 38). Annual income around $300k and our core non-rent spend is around $25k. Aside from the rent, I feel we live like paupers! But we’re homebodies and enjoy the simple life at home

Congrats!

Sure, I’ve written some posts about negotiating a purchase:

https://www.financialsamurai.com/in-real-estate-money-is-made-on-the-purchase-not-on-the-sale/

https://www.financialsamurai.com/some-things-homebuyers-forget-to-consider-when-purchasing-a-house/

https://www.financialsamurai.com/spray-and-pray-the-cheapest-way-to-invest-in-real-estate/

https://www.financialsamurai.com/no-contingency-financing-offer-a-way-to-offer-all-cash-for-a-property/

There are many more. Check out the search button. Good luck!

We pay 3.75% right now on our primary residence, and we owe about 238,000. We have excellent credit. Do you think it’s realistic to find a rate right now around 2.8%? Any recommendations for the lender with the best rates for conforming refinances?

refinanced back in 2016. 15 year @2.625. Glad I don’t have to do this again

Just finished ours a couple weeks ago, $468K, 2.5%, 15-year, $10,019.25 in total costs (including all Fees and Points) . We started 8/13 and finished 9/24 so not nearly as long or headache inducing.

However, very similar story with inaccurate closing costs.

The short of it–coincidentally I paid my insurance bill one day before I started the refinance, which meant when they began estimating the loan a couple days into the process, the bill still showed unpaid and was included. Est. closing costs were sent a couple times prior to signing with the bill included, each time I told them it was paid, they confirmed and agreed to fix it by signing. Signing day, inaccurate Estimate sheet from title and accurate sheet from Escrow included in docs. Again, I called the Broker and everyone confirmed we were good and to ignore the Title sheet, “Escrow overrides Title,” I was told. We signed.

Within the week, refund check shows up and it is short the insurance payment. I call & email again, Broker agrees to fix it immediately. They confirm, again, the insurance bill had been paid. Escrow fixes the mess, finally, and remainder of refund showed up within 3 days.

Again, not nearly as exhausting as yours sounds, but just proves how critical it really is to read through the closing cost sheet for accuracy.

Yeah, the title & escrow company would rather us pay large overages, than underpay and not successfully close. I guess the borrower would prefer the same thing.

It’s just after a certain amount of overage, a borrower my suspect something is fishy, especially if the overage is obviously wrong to the borrower. You never know whether you will actually get your overage charges mailed back to you.

When neither the mortgage or title officer addressed my question on whether I’ll be credited back and within how many days, despite explaining all the erroneous charges and still not seeing the right math, that’s when I started getting worried. Like, why are you ducking this question?

How much of your $10,019.25 closing costs was actually fees, versus homeowners insurance and prepaid interest you would have had to pay anyway?

$468,000 New Loan

$453,682 Loan Payoff

$7,184 Points on New Loan

$228 Interest on New Loan

$1,126 Interest on Old Loan

$2,914 “Fees”

$2,866 Refund/Loan Paydown

We went through a Broker for our loan and although he was very quick to communicate and respond, he always brushed over everything that it would be okay and fixed down the road…No matter what we brought up, it was always that someone would fix it later. Individual names instead of trust, insurance paid or not, etc.

My goal was to make this is the last refinance we have to do (on this home)…which is why we went with paying the points for the long-term savings as our goal is to convert to a rental if or when we move.

I get most annoyed by the smallest fee….. the credit report. Everyone and their mother can get a report for free these days!

Banks can’t. That’s a 3rd party fee they pass along to you. I’m a lender, and if we could pull the report and score for free we definitely would! It is frustrating though because clients look at “closing costs” like they are all coming from the bank. In reality, most of the closing costs are for title fees, appraisal, accrued property taxes, and other 3rd party fees. Our bank actually doesn’t charge ANY lender fees whatsoever, but I still have to deal with irate clients regularly who want to know what XYZ fee is for. I’m usually like, “um, ask your home insurance agent who quoted you this policy…” and “yeah, title fees are set by the state and I promise I really truly can’t control or negotiate them…” etc.

Thanks for sharing this Sam. I am in Canada so things work a little differently and the banks are less competitive with each other. We decided a few years ago to go the ‘pay off the mortgage early’ route and this Friday we make our last payment (I’m 46 and she is 50). I was feeling smart when it looked like rates were going up but now realize we need to double down on investments to get to freedom. Having the mortgage gone is a nice feeling, but now the race is on the other side of the ledger – right when the markets seem to be frothy ;) I am investing in some bond etf’s to build up some ballast so we will have dry powder when markets drop.

Cheers and thanks again for sharing

Ah, if the banks are less competitive with each other, they would be MORE stringent in the mortgage refinance process b/c they are not hungry for as many clients and can accept only the most credit worthy.

Congrats on paying off your mortgage! Yes, much more capital is needed to generate the same passive income. Tough for retirees!

But good stuff tackling both saving and earning all the same.

Related: Are You Willing To Retire Early To Live Near Abject Poverty?

Interestingly Mortgages work differently here. People usually get a 25 year amortization with a fixed rate – however that rate is far and away guaranteed for only 5 years. Therefore the spread between our variable and 5 year fixed is even less than what you see there. The banks up here really don’t risk much as many of these mortgages are insured by the federal government. Part of the reason why Canadian banks have been great investments.

Sam- I feel your pain. we recently purchased a vacation home in Lake Tahoe, where I put 40% down thru my bank, BofA. 10-1 arm. I have considerable assets invested, and own primary residence, but like you, didn’t see selling triggering capital gains taxes a good move. I worked with 2 or 3 different loan officers thru the 3 month torture ( each one would go on vacation every few weeks). So what happened was each loan officer required another set of the same mountain of information. 3 years tax returns, trust returns, written explanations about everything. I had a mountain of info by the end, and the underwriters kept asking for the same info over and over. Almost seemed like they were trying to make me quit the process. I got to be comical.

In addition, I purchased a commercial building about 6 mos prior with B of A, so they already had all my info in their computers.

Once the loan finally closed I received a courtesy call from the bank’s VP in charge of customer relations. “how was your loan process.” I politely unloaded on him, and have not heard from them since.

next time paying cash, never again.

Chris

Oh man, you just reminded me my loan officer took a week off to go to Hawaii during the last three weeks of the refinance period! He said he could not log into his VPN network, so that delayed our closing by several days.

I felt bad for interacting with him on vacation, but we were almost 4 months in already and 1.5 months past his guidance on when the refi would be done.

Glad you got your mortgage done! I wish we both build massive amounts of capital over the years to never have to refinance again too.

That does sound like a nightmare situation to begin with. A lot of people would not have caught the mortgage lender error and have paid the $9k at closing, none the wiser (although the difference in money would not have been lost, right? It would have gone to pay down the loan faster (I hope).

Although your payments went down, it was because the principal financed was less as your actual interest rate went up (2.5% to 2.625%).

If I didn’t refinance, the payment would have stayed elevated from $3,920 to $3,970 because my rate went from 2.5% to 4.5% (ARM reset after 5 years).

The payment was on the same amortizing schedule, but was based on the original $990,000 loan amount. By refinancing, we made the payments based on the new $700,711 loan amount.

Hi Sam

Long time reader. First time poster. I’m in the mortgage business and was just wondering why you didn’t just roll everything into the loan so you didn’t have to bring in any funds in at closing? Once you sent in those bank statements, the lender will pick that apart and question everything

Easier route would have been to just increase the loan amount and close with bringing in no funds. Once the loan is closed just pay that principal down instantly with the amount you were planning to bring in anyway

Wasn’t offered this choice, but probably could have.

But, I don’t want to increase my loan amount. I want to decrease my loan amount. I use all refinancing opportunities not only to lower my rate, but to also pay some principal too. In fact, I wanted to pay the principal down to $700,000 even, but didn’t want to have them redo everything again. The loan amount was closer to $710,000 when we started (4 payments).

My goal is to march all debt towards zero in a faster than amortization schedule manner. With my primary, I will pay off everything within 15 years, if not 12 years (5/1 ARM + 7/1 ARM), just like I did my SF rental in 2015.

Related: Mortgage Payoff Fees And Procedures To Know

I agree with your thoughts about not putting costs into the loan itself. This seems “scammy” to me. What James is saying: “Please increase your debt load while at the same time pay us increased monthly interest all for the priviledge of allowing us to lend you tens or hundreds of thousands of dollars for which you will pay us. This lets you avoid the inconvenience of coming up with some cash at closing. ”

Ultimately depending in interest rate, one may pay 1.5-2.0 dollars for every dollar of debt so the $5000 closing cost turns into a total cost of $7500-$10000. No thanks.

Hi Sam, I’m amazed you went through that whole process! I would’ve got pissed and just paid the mortgage off. On a side note, I went to Napa Valley for a wedding this weekend. Took 3 hours to drive 75 miles from SFO to St. Helena on a Friday afternoon. Took 3 hours and 15 minutes to get back Monday morning. I finally understand why people spend a million plus to live in the city. Traffic is horrible!! I would spend everything I had to avoid that commute.

Thanks, Bill

I just refinanced to 2.75% 30 year fixed. love VA loan streamline refinancing. At this new interest rate that is less then inlaftion, I think I will have to keep this property as a rental. The lower monthly payments also make it prospectively cash flow positive as a rental too.

Please tell me more about the VA loan and how you qualified and the DP requirements and costs. That is a great rate. Thanks

It’s a VA loan so only for military or veterans (me) and the VA guarantees 25% down so a DP is generally not needed. There is also the VA IRRL (interest rate reduction loan). This is basicallly a super cheap streamline refinance if rates are at least .5% lower then your current rate. This is my second time using it. I went from 4% to 3.35% with USAA for only around 3k in fees. Now I am dropping down to 2.75% with PH Loans but it’ll be more around 5-6k since I am switching lenders and paying 1500$ in points for the low rate. Also, there is no income verification requirement which is nice because I am in grad school.

Very nice! What do you mean the VA guarantees 25% down? They pay for your 25% down payment?

Getting an extra 1.1k a month out of a refinance is good at any income level but I am curious about the extra 80k a year to plan to put towards the principle. Wouldn’t you be better off investing it? Even if you dont want the risk, with your new rate you could put it in a savings account that gets a higher return. You should be able to pay your house off even sooner that way if that’s really what you want to do.

Just curious why you picked paying the extra principle every year with such a low interest rate.

I’m curious what you’d do with our situation:

– Home in the Bay Area (180k left on a 15 year fixed 2.875%, original loan $330k, purchase price 435k, current zestimate 900k)

– 2 rental condos (Sacramento area). No mortgage. zestimate 150k each. Cash flow minus expenses: $20k/yr.

– Cash 100k

– IRA 150k

– Income 180k

– 2 kids in public school (elementary)

– Health care via my wife’s PT Union job. I work in tech.

We’re thinking of getting a mortgage to buy another rental property (or 2, in Sacramento, again). These probably wouldn’t cash flow much initially, but eventually we’d own them free and clear like the other two and be essentially FIRE given our frugal lifestyle. Bubble risk is on for Bay Area adjacent real estate but likewise for stocks… thoughts?

Sacramento is back to GFC peak levels which makes me nervous now. In a crash; the Bay area might retain value while bedroom communities fall. I remember Tracy in 2007.

BTW isn’t it better to pay off your primary and instead have a loan on the rentals? The mortgage interest is a write off now given the TJCA the loan on primary might not be as beneficial.

Depends on how you are holding the rentals. Where I live commercial rates are higher than residential rate, so a 2.8% residential loan would go to 4.5% commercial and pretty much wipe out whatever tax benefit from deducting the interest and that doesn’t even factor in QBIA deductions from rental net income.

Sam, great series of refinance posts. I bought my duplex (live in 1, rent 1) in 2017 and refinanced twice since then (4.875% 30yr fixed -> 3.75% 10/1 ARM -> 3.6% 10/1 ARM) with no-cost closing . I’m currently looking at 7/1 ARMs after the Fed reduced interest rates twice this year. My biggest learning lesson is to develop these personal relationships with bankers and be patient.

Sam

What are your thoughts on recasting considering you are focused on cash flow?

I have done so many times with very positive results. The funny thing is I spoke with the bank manager about this and had to explain it to him. And most everyone I have told about this have never heard about doing this

Also a great idea, provided you don’t have to come up with too much more cash to do so and the fees are reasonable. But I like to take advantage of lower rates. A recast doesn’t change the rate.

For my bank the fees are a one time fee of $150. And it increases my cash flow by hundreds monthly when I do an annual recast.

I was told years ago that without Reamortizing/recasting the loan amount (principle) you will be paying interest on principle you don’t owe, Which gives the bank an interest free loan.

Maybe I’m too risk averse, but ARMs in general seem like playing with fire, because every borrower expects they’ll be able to refinance in their favor when the ARM resets. But the music has to stop sometime and that’s exactly what happened during the housing crisis.

Personally, I got 7 years left on a 2.875% 15 year fixed and I ain’t going nowhere. If I had enough cash to pay it off with $300k leftover I would take it in a heartbeat. Because then I would immediately save all the mortgage interest (the tax deduction is nice but not the same thing) and also my cash flow would go through the roof (because I’m still working) without that payment.

Now, you may be able to pull it all off. Mop up distressed assets during the upcoming recession, keep up your current cash flow at the same time as if it won’t be affected during the same recession, manage all your family expenses, etc., but that seems optimistic.

After 35 years of declining interest rates, it is a possibility that rates could go up. However, I’m in the low rates for life camp. That’s the beauty of the market. There’s something for everyone. People are willing to pay more for peace of mind. Related: 30-Year Fixed Or ARM?

I’m an optimistic fella. I have to be in order to have taken a leap of faith in 2012 and leave full-time work behind.

I love to have options. And I encourage you to accumulate enough cash to have these type of financial options as well.

Congrats on closing! Phew that sounds like one heck of a stressful ordeal you had to go through. Six months is a looong time to have to do so much back and forth. Glad everything worked out in the end! That’s a fantastic rate and a great amount of monthly savings. And wow great catch on the lender error. I bet there are so many people who don’t realize when they are getting overcharged. With so many moving parts and fees the numbers can get confusing. Lame they didn’t even apologize! Glad you can relax now that it’s over and done!

The title officer was responsive, but unkind. Making me feel bad/stupid for explaining some line items was not good. And then her actually getting it WRONG and saying nothing of it was also annoy as well.

Glad to no longer be dealing with her!