Guaranteed returns are always nice. Unfortunately, guaranteed returns are generally very low, especially in this low interest rate environment. Due to low interest rates, investors have been investing in risk assets for greater returns.

The first thing we need to understand is money used to invest in a CD, pay down a mortgage, or pay off student loans should be grouped together in one bucket: the guaranteed returns bucket.

In a different bucket is the money used to invest in the stock market, private companies, and alternatives. This bucket carries risk in return for hopefully greater reward.

First Bucket Of Guaranteed Returns

Within the first bucket of guaranteed returns, we can further differentiate between paying down debt and investing in a CD. Your mortgage and student loans will eventually be paid off based upon an agreed upon lending term.

Even if you lob an extra $5,000 to pay down principal, your amortizing mortgage or student loan monthly payment will not change. The only thing that will change is your percentage mix that goes to paying principal (increases) and interest (decreases).

Given your mortgage and student loan payment amounts do not change, your monthly cash flow also does not change. The only real reason to pay down a loan quicker is due to the dislike of having such loans or the dislike of having loans plus the desire to make a guaranteed return compared to the risk alternative. You've already allocated some money towards riskier investments like the stock market.

The problem with paying down debt is that you increase your risk of insolvency because you reduce your liquidity. The increased risk might just move a hair, but it's still moving towards insolvency if your income isn't secure.

How To Invest In CDs

If you haven't invested in CDs before, rest assured it's very easy. My favorite way to invest in CDs for guaranteed returns with with CIT Bank. As an online-only direct bank, CIT Bank is able to pass on their overhead savings with better rates for consumers.

Simply click on the button below, select a type of CD, answer a few questions, deposit funds electronically, and voila. You can do it all electronically from anywhere you have an internet connection.

CIT Bank offers the most popular types of CDs such as term CDs and no-penalty 11-month CDs. They also have high-yield savings accounts like Savings Connect.

The Game Plan For Guaranteed Returns

Here's the game plan I followed. I built a CD investment ladder for financial security while concurrently paying off $40,000 in graduate school loans in two years and a $464,000 mortgage in 12 years.

1) Secure and bolster your income as much as possible. The most important thing to have is strong cash flow. With strong cash flow, all financial worries tend to dissipate. Sooner or later, our debts are paid off even if we never pay down extra principal.

Bolstering your income means doing a good job at work so you can get pay raises and promotions. Securing your income also means creating multiple income streams. This includes dividend stocks, CDs, teaching, driving, rental property, online income and much more. Once your income streams are strong and diversified, you can make financial decisions from a position of strength.

2) Rank the guaranteed returns from highest to lowest. If you've decided to seek guaranteed returns, then allocating money to pay down the highest debt or investment return is most logical. Give each item a rank of between 1-5. You can also rank your debt amounts from most to least. But ranking the returns is only half the battle.

Next, Consider The Desirability And TimeFrame For Guaranteed Returns

3) Rank the assets by desirability. Now you have a clear picture of what costs or returns the most. The next step is to rank each item by how meaningful the item is to you. For example, my Lake Tahoe property has a returns rank of 5 due to its highest 4.25% interest rate. But, the desirability of holding on to the asset is a 1 because it hasn't been performing well.

At one point, I was very tempted to let the asset go. Meanwhile, I might rank a 2.5% CD as a 2 for returns, but a 5 in terms of desirability for financial security. As a result, I would allocate more capital towards building a CD ladder over paying down my Lake Tahoe property.

And keep in mind that such rankings change with time and market conditions. Now that interest rates have come back up and CDs at the best banks like CIT are paying over 4% again, CDs are a lot more attractive. It's up to each of you to decide what works best for you.

See: The Best Passive Income Investments Ranked

4) Create timeframe goals for each investment. Goals make financial progress much easier to measure. Let's say you take out a $500,000 30-year amortizing mortgage at a 3.625% interest rate, have $30,000 in student loan debt at 3% amortizing over 10 years, and a desire for financial security.

You might want to set a goal to pay down your student loan debt within five years given it agitates you the most, come up with a plan to pay off the mortgage in 20 years, and build a $50,000 CD position in five years. I've found that attacking a smaller debt amount provides a greater sense of progress. Once you come up with your goals, you'll naturally figure out a way to get there.

Recommended Order Of Capital Allocation For Guaranteed Returns

If you have all three, I recommend the following order for paying down or investing:

1) Student loans. Although student loan debt is at a record high, the average student loan is only about $32,000, a fraction of the average purchase mortgage size of $294,000 according to the Mortgage Banker's Association in 2015. Paying down $32,000 in debt is much easier than paying down $294,000.

Further, a student loan cannot be discharged/forgiven during bankruptcy. You can deduct the interest off of student loans up to $2,500, but only if you make under $80,000 as an individual or $160,000 as a couple. Eventually, the student loan moratorium will be over. And it doesn't look like much will be given for free under the Biden presidency.

2) Mortgage. Most mortgages are amortized (paid down) fully within 30 years even if you don't pay extra principal. Until real estate accounts for less than 50% of your net worth, I don't advise paying down extra principal quickly.

Having too much of your net worth in an illiquid asset can spell trouble in a prolonged downturn. Mortgage interest indebtedness is deductible up to a $1M mortgage, and the mortgage interest deduction only starts phasing out after you make roughly $250,000 individually.

Check out the latest mortgage rates with Credible. Mortgage rates are off their pandemic lows. However, mortgage rates are still affordable. If you haven't refinanced in 12 months, I would refinance into an ARM or a 15-year mortgage.

It should go without saying that nobody should ever carry credit card debt beyond the one month grace period. The average credit card debt is an egregious 15%, and often goes up to 30%. If you do have credit card debt, do everything possible to pay it off first and never get into revolving debt again.

CDs Are An Easy Source Of Passive Income

3) CD step stool. Besides getting into the habit of maxing out your 401k, you should also build a CD ladder or CD step stool. The more rungs the better.

Before you build a CD ladder, you should have at least six months of expenses, preferably in a higher yielding online savings account that is never touched. I recommend having 10% – 20% of your net worth in a CD ladder to provide priceless financial security as you strive to achieve your financial goals through risk investments and work.

Click here to open a CD account today with CIT Bank. It's safe, secure, and easier than ever before.

Guaranteed Returns Vs Risk Returns

Some of you might wonder what percentage of your savings should be allocated towards Guaranteed Returns (CD, paying down debt) or Risk Returns (investing in the stock market, private equity, P2P, hedge funds). There's no one size fits all guideline, but here are my suggestions.

Ages 18 – 35: 10% – 30% of savings to Guaranteed Returns, 90% – 70% of savings to Risk Returns. If you're like most 20-something year olds, you've got student loan debt and potentially mortgage debt by the age of 35.

Given you've still got your entire income earning life ahead of you, your chances of not being able to dig yourself out of a financial hole is smaller. As a result, you can stomach more risk to seek higher reward. Losing 50% of your investment as many people did in the 2008-2010 crash is not as big of a deal since your annual savings amount can make up a good portion of your portfolio's losses.

Ages 36 – 50: 30% – 50% of savings to Guaranteed Returns. No longer can you just worry about yourself. You've now got to worry about a potential partner, your parents, your kids, and causes that matter most to you.

Hopefully, you are in the highest earning time of your career where the absolute dollar amount going towards your Risk Returns is significantly larger than when you were younger. Your goal during this time frame is to at least eliminate your student debt and have zero credit card debt. With just an amortizing mortgage to pay off, you can pay down extra principal during times of excess liquidity or poor market environments.

Prioritize Guaranteed Returns From Middle Age Into Your Golden Years

Age 50+: 40% – 70% of savings to Guaranteed Returns. If you still have student loan debt and feel you haven't made a dent in your mortgage by now, then it's time to focus! You want to minimize your debt burden to coincide with a potential decline in income due to a layoff or impending retirement.

Further, you need to have your risk-free assets built up to provide financial security. If you have no debt after turning 50, then you've already figured out how to live within your means and you should be free to allocate your savings to Risk Returns in a responsible manner.

Within the Risk Returns bucket, you can obviously adjust your allocation towards less riskier investments such as government bonds if you so choose. Below is another way to figure out what percentage of savings to allocate towards debt pay down or investing by the interest rate percentage.

The above guidelines work under the assumption that less debt is better than more debt and having a low guaranteed return on a risk-free asset like a CD is good enough once you've achieved a comfortable amount of wealth.

Related: Recommended Net Worth Allocation By Age

Managing Liquidity Is Key

At some point, your Risk Returns bucket will simply be bonus money that is no longer necessary to enjoy your life. Until that time comes I urge you to methodically allocate a portion of your savings towards the Guaranteed Returns bucket. Having too much of a financial safety net is better than having too little.

When I first graduated from college in 1999, I immediately began allocating 30% of my savings towards CDs, and the rest towards my 401K and after-tax investment account to one day buy a property. Work was rough, and the dotcom collapse was a huge wakeup call to hold risk-free assets.

After I bought my first place in 2003, I took out loans for my MBA between 2003-2006. During this time, I reduced my CD contributions to 20% of my savings and invested 80% into the stock market. Two years after I graduated, I paid off my student loans because it felt annoying and bonuses were still good back then. I couldn't deduct any of the student loan interest and the stock market was beginning to turn. The feeling of paying off a significant debt was amazing.

From 2003 – 2013, I paid an extra $3,000 – $20,000 in mortgage principal each year when I felt I had excess liquidity and nowhere better to invest. After paying down an extra $140,000 in principal in 2014 using a mortgage arbitrage strategy, in 2015 I decided to pay off the remaining ~$100,000 balance. Locking in a guaranteed 3.375% return felt fine compared to an uncertain stock market.

I set a plan to attack my $418,000, 4.25% Lake Tahoe mortgage with $15,000 a year in extra principal payments. My goal is to pay the entire mortgage off in 11 years at the age of 50, 10 years earlier than the normal payoff schedule. Fortunately, I beat my goal by 5 years and paid it all off by age 45.

You can never lose if you lock in a gain. Just make sure to be aware of your liquidity at all times. The closer you are to achieving financial freedom, the more you should consider guaranteed returns.

Diversify Your Investments Into Real Estate

Although getting high guaranteed returns is difficult, real estate investing is an investment I like the most. Stocks are very volatile compared to real estate. Therefore, if you want to dampen volatility and build wealth at the same time, invest in real estate.

The combination of rising rents and rising capital values is a very powerful wealth-builder. Inflation should also help boost real estate value as well.

Take a look at my two favorite real estate crowdfunding platforms. Both are free to sign up and explore.

Fundrise: A way for accredited and non-accredited investors to diversify into real estate through private eFunds. Fundrise has been around since 2012 and has consistently generated steady returns, no matter what the stock market is doing. For most people, investing in a diversified eREIT is the easiest way to gain real estate exposure.

CrowdStreet: A way for accredited investors to invest in individual real estate opportunities mostly in 18-hour cities. 18-hour cities are secondary cities with lower valuations, higher rental yields, and potentially higher growth due to job growth and demographic trends. If you have a lot more capital, you can build you own diversified real estate portfolio.

Managing Your Net Worth Carefully

One of the best way to become financially independent and protect yourself is to get a handle on your finances by signing up with Personal Capital. They are a free online platform which aggregates all your financial accounts in one place so you can see where you can optimize your money.

Before Personal Capital, I had to log into eight different systems to track 25+ difference accounts (brokerage, multiple banks, 401K, etc) to manage my finances on an Excel spreadsheet. Now, I can just log into Personal Capital to see how all my accounts are doing, including my net worth. I can also see how much I’m spending and saving every month through their cash flow tool.

A great feature is their Portfolio Fee Analyzer, which runs your investment portfolio(s) through its software in a click of a button to see what you are paying. I found out I was paying $1,700 a year in portfolio fees I had no idea I was hemorrhaging! There is no better financial tool online that has helped me more to achieve financial freedom. It only takes a minute to sign up.

Finally, they recently launched their amazing Retirement Planning Calculator that pulls in your real data and runs a Monte Carlo simulation to give you deep insights into your financial future. Personal Capital is free, and less than one minute to sign up. It's one of the most valuable tools I've found to help achieve financial freedom.

Guaranteed Returns is a FS original post. When in doubt, pay down debt for a guaranteed return.

I was motivated to called my bank after I saw your response and resolved the issue pretty painlessly. Apparently during the application process there was the option to choose whether you are *not* subject to backup tax withholding or if the IRS notified you that you *are* subject to backup tax withholding. So unfortunately, this was an oversight on my part during the application process and I selected that I am subject to backup tax withholding even though I am not and have not been receiving my full interest payments since Jan 2016. However, they were able to retroactively correct this from January 2017 since there is nothing they can do about last year since taxes have been filed already for 2016. Better to learn this lesson now in my early 20’s than later!! Thanks!!

Good to hear! Taking action with ones finances is always a good thing. It’s one of the reasons why I track my finances like a hawk. Nobody is more interested about your money’s well-being than you!

Do you have to pay ‘backup tax withholding’ on your CDs? I just noticed there is a discrepancy between the interest I earn on my CD’s and the amount of interest that actually gets deposited into my CD every month. Should I call my bank or does this just come with having CDs?

Big fan of this blog!!

Very interesting! I’ve never had the bank take out backup withholdings. It’s always gross.

The decision is only for the interest to go back into the CD account or be sent to my checking where it is liquid.

Welcome to my site!

I really get a lot out of your articles, so I want to also help my friend. She is a 65 year old divorcee, and is considering taking on a mortgage of $650,000 at 3.875% at 30 years. She is getting into the game late, according to the chart above she would be paying the mortgage down at more than a 35% debt payday allocation (she is currently invested in the stock market at 50%, 50% money market for down payment). Since she is ahead of the game right now as she has no debt, would you advise thinking ahead and taking on a smaller size mortgage. Is the chart above to change based on her age as well. Thanks again for your great articles.

My situation:

$264k left on $330k Bay Area mortgage. 11.5 yrs left on 15 yr. 2.875% fixed. Bought for $435k. Est value of my little house today: $750k. No, my wife is not willing to move :) and I don’t want to either although it’s certainly tempting.

approx. $80k in traditional IRAs (me & wife. straight index funds) $12k in robo-advisor accounts. My wife has an additional $30k in savings.

2-bdr rental condo in Sacramento. After HOA, property tax, prop mgmt… only about $650/mo. Worth about $100k. We bought it with cash a couple years ago.

Income: $120-150k/yr combined. 41 years old 2 kids. Not looking forward to another 15 working years in my field. Looking for alternatives/flexibility/etc.

No other debts. Suggestions? Beyond the IRA contribution, We’re debating saving for another little rental, paying off the mortgage early, buying more funds, etc.

I think about this a lot. Here’s my thoughts, and how they differ. I have a $480,000 mortgage at 3.5%. After tax deductions for mortgage interest that turns into an effective rate of around 2%. If the Feds long term inflation target is 2%, that turns this into an interest free loan in the long run. As long as I have plenty of liquidity, and strong/safe cash flow, I should defer paying off this debt and invest in other revenue streams. The same thought process should apply to my wife’s medical school loans at 2.65%. Obviously you can take this thought process straight into over leveraging and spending the extra cash flow on an inflated lifestyle. I make a point of avoiding that situation like the plague.

I know that there are emotional reasons for paying off low interest/tax deductable debt, but from a purely financial perspective I think it can have real down sides.

Absolutely agree. Im putting everything else into tax deferred and then taxable investments. If you wanted to inflate your current lifestyle than that could be a good argument for debt pay down above all else. Im more interested in my lifestyle a decade from here.

The emotion removed itself from my equations once I did the math, after that it just didnt make as much sense.

The trick is to watch the lifestyle creep. The article is really good advice for the vast majority of people. You really need to keep your liquidity and avoid over leveraging.

Yeah… but the fed target is 2% that isn’t where it has necessarily been for the recent past (sub 1%). That being said 2-1%~1% which is a super cheap loan because you can likely invest that money elsewhere and get more than 1% after inflation and taxes are counted for a somewhat arbitrage profit.

Josh,

The older and wealthier you get, the more I think you’ll want to pay down the loan.

But, if your effective rate of 3.5% is really only 2%, that means you are making $500,000+ since that means you are paying a 42% effective tax rate. Is that what’s going on? The highest tax bracket earners definitely benefit the most from the mortgage interest deduction.

S

It would come off the marginal rate not the effective, so it could be a lot less (250+) as long as you were also in a high tax state as well. Its really about 2.2, but roughly similar depending on exact inputs.

I made $250,000 last year. Between federal and California income taxes my marginal rate is just over 42%.

You’re right. It’s about the marginal tax rate, not the effective tax rate.

Hopefully your effective ta. Rate is closer to 30%.

So the exactly correct case lol. Also in cali, we have to pay for this place I guess.

How about cash-in refinance? Thanks!

A cash-in refi can definitely bring great returns of the interest rate falls and the cost to do so is reasonable. Definitely an action worth writing another post about to show how the mah works.

Great! Definitely looking forwards to reading your future article about it! coz this year i am not sure where to put my money for investment besides US treasury. I am considering to do a cash-in refi sometime this year. Thanks!

Do you have more information about “After paying down an extra $140,000 in principal in 2014 using a mortgage arbitrage strategy…”

You caught my attention with that line, but I’m not sure what you’re referring to with ‘mortgage arbitrage strategy’. Is it something HELOC based?

Thanks!

Here yah go! https://www.financialsamurai.com/increasing-passive-income-through-leverage/

Thanks!

You say “The problem with paying down debt is that you increase your risk of insolvency because you reduce your liquidity”. Typical Australian loans may be different, but for the ones I looked at you can redraw any extra payments you make in case you need the liquidity. So for the risk free portion we always allocated 100% to paying off the mortgage (best interest rate we could find) knowing that we can get it back at any time. We now have about $300k we can get out any time in the next 20 or so years at a low interest rate designed for first time home buyers.

That’s very interesting. Redraw extra payments penalty free? That’s a great system. And Aussies have some of the largest net worth and inheritances figures in the world.

Mortgage interest isn’t deductible in Australia though right?

Where do you get 2.5% cd? I use ally which has 2% but can’t find higher than 2.2..

Pay off the mortgage! We did so years ago and it set us up for a much better lifestyle. When my job changed – with a deep breath before a new job was found, I was so happy that our castle was ours. There is the +/-‘s of any investment/savings decisions – but also think about the emotions of having your home paid off. We are now less than 2 months from early retirement @ 49 years old – it worked for us!

Great post Sam!

I have been thinking about this a lot since setting the goal to kill our mortgage in 7 years 3 months. This month we officially started year two. The plan calls for a escalation of additional principal payments each year.

I call it the “Mortgage Snowball Strategy” and it looks like the following to pay off our $352,000 mortgage in 7 years 3 months:

Year 1 = $800/month or $9,600/year

Year 2 = $1,600/month or $19,200/year

Year 3 = $2,400/month or $28,800/year

Year 4 = $3,200/month or $38,200/year

Year 5 = $4,000/month or $48,000/year

Year 6 = $4,800/month or $57,600/year

Year 7 = $5,600/month or $67,200/year

Year 8 = $7,120/month for 3 months or $21,360/year

When I developed this plan there were several things I was trying to accomplish:

1 – Obviously goal #1 was to get the mortgage paid off. Specifically my wife and I decided we would like to be mortgage free by 35. This gets us mortgage free 7 months before our 36th birthday.

2 – I wanted absolutely no Austerity. Meaning I did not want it to effect our current lifestyle. The plan is fully dependent on annual increases in our income. I assumed that we can grow our income by at least $10,000 a year or more. Historically we have been able to increase our income by $20,000 or more per year.

You bring up a good point in your post around risks of net worth concentration and liquidity. Besides the increases in income dictating whether we stay on track or not there are two other variables I watch closely:

A) I don’t want our primary residence to make up more than 25% of our net worth. It currently makes up about 18% of our net worth. So, the goal here is to keep investments/savings at a high enough rate to keep this below 25%. Which should not be too hard.

B) We currently prefer to keep a cash cushion of $50,000 in the bank, which includes short term 12-month CD’s. If our balance were to drop below this mark for more than a quarter, it would force a re-evaluation of the additional payments.

With respect to CD’s, we are currently holding <10% of our net worth in 12-month, 3% CD's from Navy Federal Credit Union.

Cheers,

Dom

Thats a lot of cash thrown at something that grows at best the rate of inflation and doesnt change cash flow or options much. Especially given your young age you have to do the opportunity cost calculation of that money being in the market for several decades. Spoiler alert, its massive. Remember, this is simple vs. compound interest, it is never stressed enough how important that is.

Also remember to think of your mortgage at the tax effective apr, not the nominal. It ends up being small overall.

The alternative is to open up a mortgage paydown mirror fund in a taxable investing account and throw it into index funds and maybe some muni bonds (if your tax rate is high enough to benefit). Contribute according to your schedule and at the end of year 8 you could either pay it all off, or do whatever you like with it. As a bonus it increases your liquidity and ability to adapt to unforeseen circumstances.

I did this with my student loans. I had a crazy grand plan to crush them in 3-4 years, but I wouldnt be able to contribute to retirement funds and thus would be paying at my marginal rate (no thanks!) for every extra dollar into it. So instead I did the math, slapped myself and am maxing out tax deferred account and the rest in a taxable. It wouldnt be long before I can make my monthly payments with the cash thrown off from my taxable accounts if I wished, and thats kind of the point.

In the end the net worth change is initially the same, but long term one will have an outsized effect on your life and the other wont.

You’re right Zaphod… except as they like to say past returns do not reflect future ones! Look at last year with the negative ROI on the market! But in the long term I still feel bullish of course but it’s not as simple as you say!

Though my big complain on paying extra on the house is this – say you lose your job after having paid all this… the bank sells the house super cheap because they just needed a smaller portion to cover the balance of their loan and you could take a huge loss that they didn’t really care about. If you owe them a lot they have to be more patient to not lose a lot or any.

I’m more of the mind of investing elsewhere and paying off the entire house when you have enough to avoid that if that’s your goal of being debt free. Then I was able to take advantage of cap gains, mortgage interest deduction, inflation, and more piece of mind that if I ever did default I still have a lot of coin lying around. But I’m a defensive risk management type investor. Though I still do some investments that are riskier for higher returns but it’s all about calculated risk to me.

If you feel you’re going to pay off you house and not lose jobs and you want the psychological part of that knock yourself out. Especially if you’re a horrible saver and will spend the money elsewhere then it’s better spent on principle than a credit card for fun! At 35 and debt free even if you had no other money (which doesn’t sound like the case, but if you did) owning a house outright and likely cars too with decent salary gives you 30 years to build massive amounts of money with very low overhead. Meaning you’re a Saudi’s oil producer with low production costs vs your competition (you require less to live than a competitor that has to pay their living costs still). So I don’t think it’s a bad idea to be debt free. Then when another opportunity arises you still have access to credit because you don’t have a mortgage. Just some thoughts to ponder though.

Very impressive cash flow plan! I will be curious to see if you stick with paying those ever higher payments each month. So long as you get those raises, it should be no problem. The only problem is that life never works out the way we planned. Something always comes up!

Good job highlighting the difference between your personal balance sheet vs your cash flow statement. Everyone understands the balance sheet almost instinctually – this is what I have, this is what I owe. But many only tangentially understand cash flows. There’s the realization that eliminating debt means freeing up cash for investing, but it doesn’t always tie back in to how that impacts the existing cash flows. It’s a subtle distinction, but an important one.

Personally, I bucket all my income into short term and long term expenses and investments, maintaining enough to keep my day to day cash flow uneventful, while letting me invest to build the future cash flow we’ll be living on in retirement.

After reading your post this morning, I decided to bite the bullet and do a refi on my investment property. I had been delaying because of the potential hassle that I gleaned from reading your past posts.

My current rate is 5.375% on a 30 yr fixed. My bank quoted me 4.25% for a 15 yr fixed with an estimated 3.3k in fees. I calculate the break-even point at about 5 years.

My FICO score is 800+, I have no other debt, and an existing relationship with this bank so I am hoping this goes smoothly.

My initial plan was to try to pay the remaining balance as quickly as possible. However, my liquid savings is not where I would like it to be for coming into a bear market. Your post this morning reminded me that I should build that up before paying off the loan.

Just a thought, but if you’re not comfortable with your current liquid savings, then you may want to reconsider doing a refi into a 15 yr from a 30 yr as the higher payment would be a detriment to your cash flow.

If you are looking to increase liquid reserves in as a risk mitigation strategy, then I would also be looking to maximize cash flow, in which case it would make more sense to refi into a 30yr fixed or ARM.

Additionally, there are a number of credit unions out there that offer competitive rates on HELOCs against investment properties, which would be another risk mitigation strategy.

Thought about that, but I got a half a point better rate on the 15 year over the 30 year. The remaining balance isn’t too large, so I plan to pay it off in 10 years, but wouldn’t want to go longer than 15.

If you are looking to pay off in 10, I’d recommend a 5/1 or 7/1 ARM. Even lower rates, plus the flexibility to revert back to a low low payment due to 30 yr.

Also, rates do seem high as indicated below. I just closed on a 30 yr fixed at 4.5%

I looked at posted mortgage rates at some major banks and the 15 yr fixed had a better rate than the 7/1 ARM. It kind of surprised me.

For example – https://www.wellsfargo.com/mortgage/rates/

You should be getting a better rate for a 15yr term give your FICO.

For investment property, and a 15-year fixed, it doesn’t seem that unreasonable to me. We’ve got two loans on investment property, both 5/1 ARMs, at 3.778% and 3.884%. For a 15-year fixed I would expect 4-4.25% to be right in the range of normal.

yeah. 4.25%?!? you should be at 3.25% max.

check out rate30.com. i refi’d with them. they were .25% lower than anyone else.

Are you comparing investment property loans or owner-occupied loans? I’m asking because everywhere I look at investment property loans for a fixed 15 year term, the rates are about 4.25%-4.75%.

Single family owner occupied? Sure, 3.25% easy.

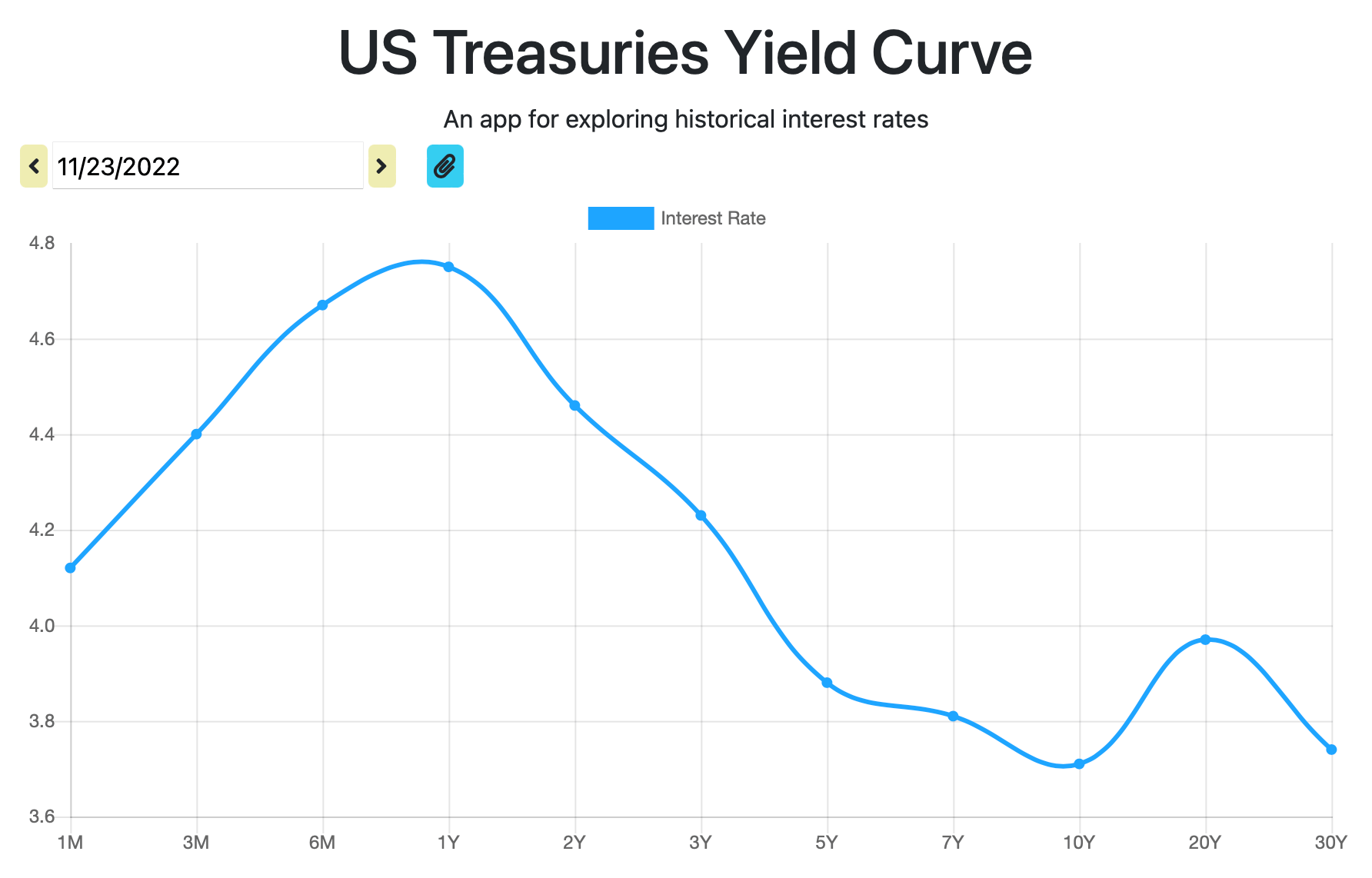

Hi Matt – I would try and pressure your bank to lower their fees to the point where your breakeven point is 2-3 years, or search for an even lower rate than 4.25%. The 10-year yield has moved down 0.35%+ since December 2015’s rate hike.

To give you an example, I have a 5/1 Jumbo ARM at 2.5%, and a 30-year fixed loan for my vacation property from years ago at 4.25%. A 15-year mortgage should be 3.375%-3.75% IMO. Keep checking! Check out LendingTree too. Once you fill in the info, competing banks will contact you with their best rates. Use this info as pressure on your existing bank.

I’m refinancing 4 mortgages for 4 investment properties– one Jumbo ($910) and 3 conforming ($623, $621 and $517). Rate is 3.375 for 15 year fixed for all 4 of them. Jpmorgan. It’s 50-50, Ill end up changing all 4 to 30 year at 3.875% before I close. I go back and forth between forced equity pay down and cash flow.

WOW. Those are phenomenal rates for investment property. I’ll have to check out Chase next time. In the past, they’ve been in the same ballpark as everyone else, but those rates you’re getting are definitely better than any others I’ve seen.

Hi Sam!

Australia and some UK institutions provide what is called a mortgage offset account. This works like a regular savings account, except that the mortgage interest is calculated on the outstanding loan minus the amount in the offset account. The money in this account therefore effectively “earns” interest at the mortgage rate, as the mortgage payment is made up of a larger amount of principle rather than interest.

This would be superior to a CD in terms of liquidity (you can cash out whenever you need, just like a savings account) and also in terms of interest gain, as CD interest would be taxable.

If not for the liquidity, I think I would recommend paying down the mortgage rather than investing in a CD, because tax reduces the CD return.

For example at a 30% effective tax rate:

Mortgage debt = 3.5% before and after tax.

CD = 2.5% Before tax but 0.7*2.5% = 1.75% after tax.

Paying off debt is doubly effective in this case.

But here in the US the mortgage interest is (very often) tax deductible. So the interest rate savings is pre-tax, just like a CD’s return. So its actually a similar comparison to compare the nominal returns on the CD and the mortgage.

Peace of mind for me. I have $60k left on my mortgage (3.5%), and I will take care of it this year. I also do not like it showing up on my Quicken account. I had a CD ladder once five years ago when interest rates were higher.

I am still going back and forth if these HOA fees are worth it. Is there an article somewhere? I am paying $170 a month ($2040 per year) for my primary residence.

$60,000 is such a small amount. Nice. That amount would annoy me enough to just pay it off. That’s what I did with my remaining $100,000 rental mortgage.

The HOA pays for common maintenance. You’ll have to bring your concerns up with the HOA board during their next meeting. The amount also depends on how much your primary residence costs?

Appreciate the feedback, Sam. And yes, indeed, my $60k is bugging the crap out of me, so I want to get rid of it this year. Plus, I set a goal this year that I will payoff my primary residence. This will free up $1500 a month, and I am wondering where I need to invest it (IRA, investment property, or something else). I am already maxing out deferred comp at work for me and my wife ($36k).

“If you do have credit card debt, do everything possible to pay it off first and never get into revolving debt again.”

The messaging behind your comments on credit card debt it spot on. However, there are a couple of edge cases that can be interesting at times.

I presently have about $25K in CC debt – but it’s all at 0% interest. Instead of paying that off, I put the money into a guaranteed return bucket.

Then just shuffle the CC debt onto new 0% offers every 12-15 months. Can still pay off the entire balance at any time, but at least in the interim the capital is making a small return instead (high interest checking, CD, government bonds, etc). In today’s environment, small dollars – but still some extra fun money.

Even at 0% I believe there is a Balance transfer fee. Unless the fee is also 0% in which case can you please share more details?

Isn’t a balance transfer fee something like 2%? I sure hope you are earning 500+ on alternatives in between those transfers…

I wrote about the 0% balance transfer game before. My message is that people can spend their time more wisely creating things that will make them more money than trying to shuffle debt around. It’s smart when you’re younger and don’t have much leeway, but nobody who is worth a good deal of money is playing the 0% balance transfer game. They are busy focused on growing their incoem.

I think you skipped a major point when mentioning amortization. Paying extra principal on a mortgage won’t change your payment amount, BUT it does skip you down the amortization table faster in regard to how much of that monthly payment is going toward interest. For people planning on staying in their home for many years, it’s a powerful compounding effect.

Ok, I will clarify that paying down extra principal helps pay down the mortgage sooner, in part due to a larger percentage of the fixed payment going towards principal.

Another point is that you can free up cash flow immediately (creating lower monthly payments) if you have pre-paid a lot by re-amortizing a fixed term mortgage. Some mortgages let you do this for free, others charge a flat fee (something like $250). It may be harder to do this with an adjustable rate mortgage.

I don’t think reamortizing is well known, it was suprisingly easy and inexpensive when I did it ($250). I know Wells Fargo only allows you to do it one time over the coarse of the mortgage.

Wonderful post. The idea of having two separate buckets really resonates with me. At one point in time I was gung-ho anti student loan debt at all costs. But after I got rid of some of my higher interest loans, I realized that having low interest loans is not all bad, especially since I can get a potentially much better return by investing.

While having student loan debt hanging around is not the most ideal situation, having a plan and knowing when they will be paid off while being able to invest is a pretty good feeling.

Hi Syed,

It’s good to be hung-ho anti debt. That’s what propels us to pay those suckers off. My student loans began to annoy the crap out of me so I just paid the lump sum down. It was like a check list I could cross off, so I could focus my time making money elsewhere.

It’s a tricky balance, no matter what you do. I’m a fan of paying down my mortgage faster rather than investing in CDs with a lesser rate of return than my mortgage interest rate. But as you’ve said, income security and cash flow comes first. I feel like my income is pretty stable. (Every time I say that, though, I feel like I might jinx myself.)

The good thing about paying down the mortgage faster is that after you’ve made some headway, you can get a HELOC to give you additional liquidity in case of emergency. I know what you’re gonna say: if the real estate market tanks again, the bank will freeze your HELOC. That’s certainly possible, depending on how much equity you have in your house by that point. But I think the threat of another massive crash like 2007-08 is very low, and I’d rather have the certainty of knowing that my debt is going away rather than the certainty of losing to interest rate arbitrage by paying more interest on my home loan than I would get back on CDs.

Personally, paying down my mortgage has been a great deal so far. By paying it down faster over the last 7.5 years, I’ve got enough equity to get a hefty HELOC at a good rate. I’m signing docs on it today. That’s going to be my emergency fund after I finish closing escrow on my new investment property.

Are HELOCs at a good rate though? Every time I look, I see HELOC rates at least 1% higher than what you can get for your mortgage rate.

You’re right, HELOCs are usually a bit higher than traditional mortgage rates, which is why you wouldn’t purposely pay down your mortgage to excess and intentionally draw money from the HELOC. But having the HELOC makes me feel less pressured to keep a big cash balance, so I can throw extra payments at my mortgage without worrying about needing cash in the short term. I save the 3% on the extra payments, and if a disaster happens and I need the cash, I have an emergency source to draw from.

To me that makes more sense than storing excess amounts of cash and putting them in CDs, but I can see how your approach might make sense for other people.

I saw adjustables at BAC (looked bcuz of this comment) that started at 2.74 variable. Shockingly low, and unsure how that would really work out since I’ve never done one but was really surprised as it was lower than their mortgage rates.

Sam so maybe you’ve addressed this in previous articles and I’ve forgot but when you save 50%+ of your take home are you also calculating the amount you put into your 401k/Ira? Ie 20% CDs, 20% Brokerage, 20% 401k. Or like 20% CD 40% brokerage and 402 is separate?

I save 50%+ of after tax and after 401k contributions.

The goal is to always max out the 401k and save at least 20% after tax and 401k. Need that liquid money to make other investments.

That’s what I assumed but your diction up top threw me off a bit to make me want clarification! So far I’ve been able to do about 75% of after tax plus I do 16% into my ROTH 401k as an engineer. Amounts are adding up very quickly. :)

you save 80-90% of your income? you must be lucky enough to still live at home… personally i calculate my savings rate considering 401k contributions (since it is definitely a form of savings). but as mentioned you lose liquidity by 401k’s so it’s important to look at the ‘cash savings’

Well when I lived at home I saved north of 95%. Moving out on my own I can only save about 75% since I had to move away to do graduate school and have to pay for costs on my own. When I graduate I will go back to my company, get a raise, go back to living at home and will save 95%+ like I used to. As for the 401k (I put in 6% and the company puts in 10% – so the 6% is taxed and will be taken out tax free at retirement, the 10% is not taxed and I still have to pay taxes on it in retirement is my understanding).

I agree it is a form of savings, I don’t really like it since I can’t actively manage it as easily though and can’t touch it until I’m 59.5 without penalty. But I do pay the tax on it now (ROTH) because I think my tax bracket is as low as it will ever be and only go up (which I will then switch over to a non ROTH for tax shielding purposes to then withdraw at a lower tax bracket).

Yes, I’m an insane saver. I am able to do it because I get little joy out of spending money vs saving and investing it so psychologically it hurts to spend… which gets me out of a lots of taxes (sales tax). But I also make a good amount of money so I’m still living better than most students do.

I feel similar to you wrt spending.

Thoughts of leaving the best as an adult, buying your own place, and living independently?

At what age do you leave your parents?

It won’t let me directly reply to your post Sam, apologies.

As mentioned in the first comment I don’t live at home right now. I live in an apartment now in Austin while I attend UTA. So living on my own isn’t really a hard thing. And I should clarify that living at home is living in my parents studio apartment which is about 100 feet from their residences. So it’s not really the same thing but still pretty close. That being said my parents allow me the freedom to do what I want and always have and don’t hassle me. They’re more like good friends than parents. But I’m also not a flake, I’m a well paid engineer and they like having me around.

As to not paying rent, it’s a fixed cost for them to have that place as they wouldn’t rent it out because it’s so close to where they live. Even now it’s just used for storage until I return. So they pay the same; me there or not. So they don’t mind me getting a financial benefit of me saving more and building my wealth. Now that you have context on the backstory I’ll answer your question.

Having lived on my own, it makes no difference living with them or not to me. So I’ll just stay with them for a few years. I have a company contract until I’m 26 (currently 23) so can save a couple hundred thousand more just living at home so thinking why not. Now I would move out if I had a gf who wanted to move in together so she would have more privacy but if not there is no point. Come 26 I will either move states or stay at the company. If I stay at the company I’ll consider buying a house or just wait for a gf. If I move states I will obviously get my own place again. I know a lot of people would feel bad living at home… but that’s because most living at home are flaky and unsuccessful… I’m already in the top percentiles of income earners and have stashed a solid amount of money, what do I have to be ashamed about? Just my .02 on that though. Also being 23 every year that I don’t live at home is losing 20-30k or so (I recon) that I could have invested and had 40+ years of compounding on which makes it really hard for me to say I should move out.

Only dilemma is that if I had a place I would have the property appreciating in value… but I guess my ROI of 6-10% depending on the investments will have to do. But 3 years doesn’t follow your 5+ years of living somewhere to buy!

I run my life like a business. I am a company with x profits (pay after tax). Do I want to be the CEO who spends lavishly or do I want to give more back to the shareholders (my bank account). I do everything to maximize shareholder wealth (mine), which means I have to do insane amounts of cost cutting to ensure maximum profits. As long as the employee (also me) can sit at the company and not complain under current conditions why shouldn’t I maximize shareholder wealth?

Now, eventually I’ll loosen up and spend more but my goal is to hurry and get my investment income up so that I can save 100% of salary and just play with the investment income for living. I think I can achieve this before 30.

With all my cash I have considered purchasing rental apartments though, as I love RE investing a lot as well (parents do some of it and it seems great with HUGE ROI) but then if I’m moving in 3 years not sure how easy it will be to manage remotely and I don’t want to pay a management company 10-12% of revenue for something I could do myself so easily.

So I will move out at 26, when I get a gf that wants to live together, or whenever I just decide it’s time to go solo I suppose. Making the sacrifice now will ensure I don’t have to make any when I’m older so I think it’s worth it short term!

Sounds like a plan to me! If you haven’t read this post, you should: Would You Give Up Sex, Good Food, And Vacations To Pay Off Your Mortgage In Three Years, as good perspective from the other side of the equation.

Already read it, been reading your site for years. Haven’t missed an article in I don’t know how long. Reading it did make me think of myself and what I would be willing to do though!

To put it in perspective living on my own in a NICE place for college kids I’m able to ALWAYS keep expenses under 1500 a month in Austin. And that’s with me going to bars every weekend, taking girls out, rent, food, and an occasional splurge buying Ferragamo’s (going to wear them 30 years so good deal to me when you amortize it) etc if I see a good sale. And I’m not sure I’ve even ever broke 1400 in a month tbh and average is likely 1200 or so. All while my salary was adjusted downward while I attend graduate school so I had to do extreme measures to keep my savings at a comfortable growth amount. So even living on my own and living it up I spend TOPS 18000 a year and probably sub 15000 (though I eat in a lot and cook as that’s super cheap – just only go out when my friends can which most are on college budgets so saves me heaps there). So I already can have sex, good food, and vacations (I work in a travel group so lots of points on airlines/hotels/rental cars) for 15k a year. Keep in mind I’m phenomenal at finding good deals and cheap prices leveraging connections I’ve made and just searching online too. And when I live at home my expenses never are higher than 200 a week and that’s eating out 15 times a week there and throwing in the bars here or there. But usually a lot lower than that (also I travel A LOT so lots of per diem for free food while I travel – and I travel so much that it burns me out to not travel much in leisure time anyways). The only time my expenses get higher is when I buy a new used car (or another kind of big ticket item). I’m a BMW guy so get a used 3 series for 10-20k cash and hold for 10 years – current one I’ve had 8 years. Maintenance on a 3 series has averaged out to 500 a year over the last 8 years which I think is insanely cheap for any car and I got it for approximately 10k at 15. So 14k (+insurance of sub 1k a year + gas) over 8 years is dirt cheap IMO. So I think you can still ball it up on limited income and save like nobodies business! It’s just when you want the NEW car, with all the upgrades, and then FINANCE it, buy all the little items at stores you don’t really need (that add quick), and go to lots of music concerts etc do you start seeing your income dwindle fast or fees on little things for convenience etc. But mentally I know to live well below my means so I can avoid that.

That being said he did great with the cards he was dealt! I love working more hours personally, less time to spend money! I think he thinks a lot like me but he did so at great sacrifice. Living at home I’m not sacrificing much of anything besides someone will maybe say I live at home… I still go out with the friends and do that stuff. And I could probably save closer to 99% if I wanted to live at home like a hermit and do nothing and never eat out but what’s the point. Eating out is a great enjoyment for me, taking girls out is too. I’ve found an equation that I like and works for me! And I helped my best friend get his savings rate to 67% this year (woot woot – next year will be even higher I bet)! So I love what I’m doing and come 26 I’ll be able to buy whatever house I want cash if I want… so I’ll likely be where he was around then too just following a similar but slightly different road. Both are short term pain for long term gain I suppose, but at the same time it’s hard for me to buy anything that isn’t an investment and isn’t on sale.

Long term I want a partner though, because with 2x the income you can save more than 2x the amount because the costs don’t scale just cause there are two of you so more money to invest! Skipping your 20s to do that and not build your network can be dangerous and leave you with the crazy women, leech women, or divorcees as options. Not saying they all are but more of the good ones are off the market due to relationships and marriage so statistically speaking you have to be careful! But I think if I make a lot and my partner makes a lot we won’t get married, that way we can shield more of our income from Uncle Sam! But then again finding a high earning single woman isn’t always easy as you may or may not be familiar with!

Most people probably wouldn’t go to the extremes I would but I love financial freedom and I just like the challenge of making more money and increasing my Net Worth, it’s just a game. I have more joy playing that game than I ever had doing consumption spending the money… but that’s just my opinion I suppose. How far from Berkeley are you btw, next time I go out there for work (which isn’t too often unfortunately) maybe we can meet up for lunch and tennis. It’ll be fun getting slaughtered I’m sure! Cheers.

This was a very interesting read. I fell like I’ve pretty much got the paydown strategy in place and it’s going well. I know what order I want to tackle them and why. I had not considered a CD ladder though. I’m going to have to go read more about this.

Thanks!

Thank you for this post! Our mortgage is at 4.88%, which is high, but husband lost his job and I don’t think we’d qualify to refinance based upon ratio of mortgage balance to income, so, the best we could do is to use any extra cash to pay it down enough that my income alone would allow refinancing, which hasn’t yet occurred, using re-fi calculators on-line. (No credit card or student loan debt, and maximize 401(k) contribution). Also working on side gigs to earn a little more.

Hi Robin,

No problem. Be careful with this quest to pay it down given your cash flow is less than normal right now. I would suggest not paying it down, but saving that money you would have paid down into a side liquid fund. Once you get enough to pay down the mortgage enough where you can refinance, assess your husband’s job situation, and have some serious conversations with various mortgage bankers that they will indeed refinance at a lower rate.

You don’t want to pay down the mortgage, have less liquid cash, and then find out the banksters didn’t allow you to refinance! Please follow my advice and save that pool of money in a liquid pool first.

Best, Sam

Thank you, Sam, I WILL follow your advice, and very much appreciate you saving me from that deep hole.

Robin, also keep in mind that even though your husband has a reduced level of income, there could very well be equity that would work in your favor towards a refinance even if the income stream is not what it once was before. Equity goes a long way in your potential refinance deal, and it could bridge the gap that your husband’s income used to cover being that you don’t intend on using that equity for anything other than refinancing (many people use this equity for cash out deals that allow them to do some sort of renovation or investment into the house itself)

I would suggest talking about how much weight your equity is actually pulling and whether or not it allows you to refinance right where you stand as opposed to waiting for a change in the principal balance.

Awesome post Sam. I paid off my residential mortgage last year after a bit of a windfall because I love the idea of the smallest monthly expenses possible. I still have 20% in bonds and 5% in cash after everything else is invested in tranches over the course of 2016.

Congrats on paying off your residential mortgage early! Is the feeling of being mortgage free everything you thought it would be and maybe more?