I finally understand why I haven't been able to shake the niggling stress I've been feeling lately. Despite writing less, doing fewer business deals, and exercising more, I still feel this gnawing pressure because I'm responsible for investing my immediate family's money.

When you invest family money, family money always feels more important compared to simply investing your own money. If you make a wrong investment decision with your own money, you may feel bad. However, you'll either work harder to recoup your losses or just internalize the pain and move on.

But if you mess up investing your partner's money, your children's money, or your parents' money, then you feel like a big donkey! Not only will you be disappointed in yourself, but more importantly, you will feel like you have let your family down.

That feeling of shame is why I don't want to manage anybody's money outside of my own. It's also why I don't want to give readers specific investment advice. I'm just sharing what I'm doing with my money. It's up to you to decide what you want to do with yours.

Too Many Financial Accounts To Manage And Questions To Ponder

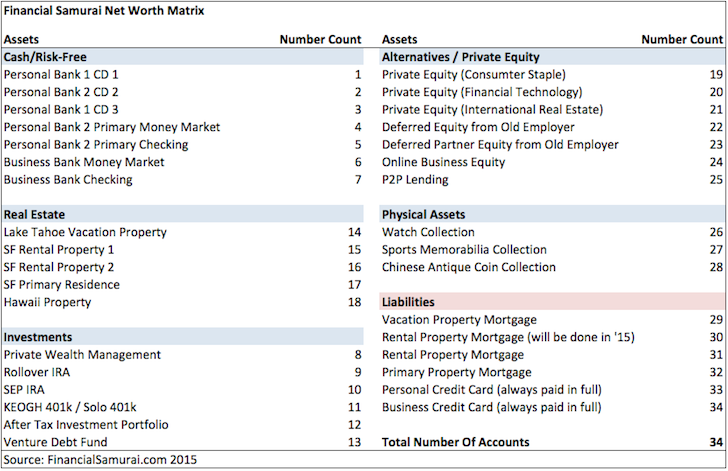

For our family of four, I have to manage and keep track of over 30 accounts. And sometimes, managing them all feels overwhelming.

Take for example the two 529 plans we opened for our children in 2017 and in 2019.

Here are some decisions I've had to ponder over the years:

- To superfund or not to superfund our son's account in 2017? The stock market was looking dicey then, and indeed sold off in 2018.

- If I superfund, should my wife superfund as well? Or should she spread her contributions out due a potential correction or bear market?

- Should we accept contributions from my parents? If so, what is the right amount? Will my parents have enough money left over to feel comfortable in retirement given I don't know exactly how much money they have. They were government employees, hence, did not make large incomes.

- Should I invest the 529 contributions in a target date index fund or a target date actively managed fund by our provider? The answer is clearly a target date index fund due to lower fees and the difficulty of outperforming an index long-term. However, only years later did I realize we had to make a choice.

- Is it OK to start contributing again to my son's 529 plan in July 2022 since it's been five years? Or do I have to wait until 2023, the following calendar year?

- How much more should we contribute to our daughter's 529 plan so that her balance will end up roughly equal to our son's 529 plan balance when she turns 18? I ended up writing the 529 plan amounts by age to provide every parent a guide.

- What is the penalty if we contribute too much and how do we fix it?

Luckily I run a personal finance site to answer these questions and get reader feedback! Otherwise, I might go mad with all these considerations!

Many Financial Accounts to Manage

Here's a snapshot I found of my various financial accounts from 2015. I'm afraid our finances have only gotten more complicated with the birth of our children.

Due to uncertainty in the banking space, having multiple banking relationships now is more important than ever to protect your assets.

The Financial Contribution Snafu

My mom has always been generous with her money. Since 2017, she has regularly contributed the maximum gift tax amount to fund both children's 529 plans. This is despite her never making more than $50,000 a year in her life and despite her not coming remotely close to the estate tax threshold.

At the beginning of 2023, she wrote me two checks and asked me to deposit them. When you receive money from a family member, it might feel great. But to me, it adds an extra level of responsibility. I don't want to let her down.

The one thing I do have is enough money to not rely on my parents for help. As a result, I always initially decline the offer. However, I also want to honor my parents' wish to contribute. After a while of declining or ignoring her request, she will start to disapprove of my actions.

Deciding How To Invest The Funds

With one of the two new $17,000 checks, I had to decide when was the right time to deposit the check into my daughter's 529 plan. I wasn't worried about the other check for my son's 529 plan because I won't deposit it. His 529 plan has enough and I don't want to accept so much money from my mom. My mom finally agreed!

Despite my mother regularly reminding me to deposit her check, I patiently waited for two month until the S&P 500 had corrected down to 3,950 from a high of 4,195 before depositing. Psychologically, even if the S&P 500 headed still lower, it felt better to deposit below 4,000.

Upon depositing the check through my Fidelity mobile app, I immediately e-mailed my mom so she could transfer funds from her savings account to her checking account. Her savings account pays a much higher interest rate.

She wrote back, “Thanks for letting me know about depositing her 529 check this week.”

It Wasn't Meant To Be

After depositing the check, the S&P 500 began to rebound. I felt great! In just four days, the $17,000 check was in the money by 3%. That's $510! Whoo hoo! What a great Family Money Chief Investment Officer (CIO) I am.

Then I got an e-mail from Fidelity saying the check BOUNCED! The $17,000 in funds was debited from our daughter's 529 plan account and all the gains were lost. How sad.

When I told my mom the news and asked her what had happened, she said she wasn't notified I was going to deposit the check.

When I forwarded her e-mail acknowledging my notification, she said “Ah, that was the time I spent hours trying to open the kids' dancing video you sent using a different app.” She had been distracted.

Lesson learned. When sending important information, keep the message as simple as possible! And good thing I didn't cash the check due to the bank run at various regional banks!

Try Again, Maybe?

My mom wants to write another check, but I told her to hold off. I still have her bounced check.

Now that she has transferred enough funds into her checking account, maybe I can try to redeposit it. But if so, I will have have to wait several days to see if it gets rejected again.

If it bounces, do I ask my mom to write another check? The answer is NO.

Forcing destiny is not the way. I did my best to wait for the right time to invest. I gave her a heads up. Yet the check still bounced. It was not meant to be.

Besides, what if I deposit her check and the S&P 500 starts to go down again? Then I'd feel like the stock market gods were laughing at me. Forget it! It's best my mom spends her money as she sees fit.

I have now successfully been able to decline both her checks without guilt. Right on!

Although my daughter's 529 plan will be invested for the next 15 years, it still irks me to have missed the rebound. The entire process reminds me that day trading is a waste of time and money. I experience too many emotions when investing in public equities.

Investing Family Money Can Be Stressful

The larger your family and the more you want to take care of them financially, the more stressful it is. The more you care about your parents, the more you will worry about their well-being as well. This is your Provider’s Clock ticking

Bear markets amplify the Family Money CIO's anxiety due to the magnification of disappointment and shame they might feel for losing other people's money. At some point, the losses could be so great that no amount of hard work to earn active income is enough to replace the losses.

There's something to be said about keeping your finances as simple as possible. There's also a benefit to not always having excess cash to invest.

Imagine just spending all your money every time it comes in and never investing for the future. How freeing! You'll never feel the pain of losing money because you're always immediately enjoying it.

The way things are going now, I sometimes feel like investing family money is a full-time job. As someone who wants to re-retire and live a more relaxing life, I'm somewhat stuck.

Fortunately or unfortunately, I've got too much money exposed to risk assets to not pay close attention. One wrong decision could cost our family in one year, five years of living expenses.

Luckily, it’s generally been a bull market, so having most of our net worth in risk assets has turned out well. If you have too much cash for too long, ironically, you might end up for long-term. Cash management is also a big part about managing your family finances because you want to feel secure, but at the same time, you want to build your wealth.

Alternatives To Managing Your Family's Money By Yourself

Investing in private funds has been my main solution for stress relief. It's nice to have someone else manage my money. In addition, if you don't want to deal with surprise capital calls, then invest more in open-ended venture capital funds instead of closed ones.

Once I've committed a certain amount of capital to each private fund, there's no turning back. As the capital calls come due, I happily pay them. It's also nice to not see the fund's daily value.

If managing your family's money is causing you too much stress, here are some alternative solutions to consider. Each solution should alleviate some amount of stress.

- Hire a financial advisor just like you would hire a property manager. Here are many strong reasons to higher a financial advisor. The more kids, parents, and responsibilities you have, the more a financial advisor can help relieve your mental load and stress.

- Farm out your public stock and bond investment portfolio to a digital wealth advisor like Empower, Betterment, Vanguard, etc.

- Buy High yield CDs

- Buy Treasury bonds

- Invest in structured notes with downside protection

- Invest in private real estate funds that diversify your existing real estate portfolio

- Utilize financial tools from Mint, Empower, Boldin, etc.

Be Kind To The Family's Money Manager

The next time you find your partner or spouse more stressed than normal and you can't tell why, maybe it's because they're busy investing the family's money.

Maybe they screwed up a trade or are second-guessing one of their rebalancing decisions. Or perhaps they're doing their best to make up for investment losses they haven't told you about. Heck, there might even be a bank run that threatens to doom the global economy!

When the family's money manager is in capital preservation mode and it's a bear market, they will likely be going through some mental upheaval. So try to be understanding and cut them some slack.

Asking them to take on more work beyond their day job and family money investing responsibility might cause a fight. It's just human nature to feel worse when you're losing.

Don't take what your family's money manager is doing for granted. Instead, be as supportive as possible. After all, they are investing for everyone's future.

Final Epiphany About Managing Family Money

In October 2023, I ended up paying for a new house with all cash. To do so, I had to sell a lot of stocks. The result is I feel LESS stressful about investing family money because I have less of it!

Our visible net worth doesn't go up or down as much, which provides stress relief. In addition, my entire family gets to enjoy our wealth by living in a nicer home.

However, I do have a new stress, which is figuring out whether to sell our old home or rent it out. Having a large asset not generating any income was stressful as we were living paycheck to paycheck for 3-6 months. Thankfully, I was able to find tenants for our previous home in February 2024.

Now I'm grinding back to financial independence because I want to have all my investment income cover our desired living expenses again. There is a good stress involved now that I have more purpose for earning money. Over 16 months after purchasing the house, I've successfully built back up my liquidity to over two years of living expenses.

Now, I plan on selling our old house to simplify life and free up even more liquidity.

Free Wealth Management

Empower is the best free wealth management platform for investors. You can x-ray your portfolio for excessive fees and get a snapshot of your asset allocation by portfolio. Empower's free tools also let you easily track your net worth and plan for your retirement.

When there is so much uncertainty in the world, you absolutely must stay on top of your finances. Understand where your risk exposure is and stay on top of your cash flow. Empower's free wealth management tools will help you bring calm to the chaos.

I've been using Empower since 2012 and it has helped me growth my net worth tremendously since retiring. It is the best free wealth management platform today.

Order My New Book: Millionaire Milestones

If you’re ready to build more wealth than 90% of the population, grab a copy of my new book, Millionaire Milestones: Simple Steps to Seven Figures. With over 30 years of experience working in, studying, and writing about finance, I’ve distilled everything I know into this practical guide to help you achieve financial success.

Here’s the truth: life gets better when you have money. Financial security gives you the freedom to live on your terms and the peace of mind that your children and loved ones are taken care of.

Millionaire Milestones is your roadmap to building the wealth you need to live the life you’ve always dreamed of. Order your copy today and take the first step toward the financial future you deserve!

Subscribe To Financial Samurai

Listen and subscribe to The Financial Samurai podcast on Apple or Spotify. I interview experts in their respective fields and discuss some of the most interesting topics on this site. Your shares, ratings, and reviews are appreciated.

To expedite your journey to financial freedom, join over 60,000 others and subscribe to the free Financial Samurai newsletter. Financial Samurai is among the largest independently-owned personal finance websites, established in 2009. Everything is written based on firsthand experience and expertise because money is too important to be left up to the inexperienced.

48 years old with 49(+?) accounts here…..it’s more if I break out individual pieces of equipment (skid steer, tractor, trucks, etc… but I lump “Equipment” & autos under one subdivided “asset account”).

How I manage the risk & stress….here is a BIG CLUE: NEVER have I ever, or will I ever, exceed FDIC, SPIC, or NCUA insurance limits… Do you think they put those little signs on the front door of every bank in the country and next to every teller window because they are joking??? Well….apparently they might actually have been joking…(total BS BTW), but you’ve got to be nuts…..it’s called ICS/CDARs, UST direct, Money Markets, do it yourself, etc… You need multiple banks, brokers, and credit unions, and you have to keep an eye on all of them, all of the time. I once opened 3 new FDIC accounts (jointly with my spouse) just to receive the proceeds from the sale of my old office building in 2018, I was informed by the title company “agents” that I was “paranoid and wasting money on extra wire fees”, I told them where to stick their “expertise”, and that I was more than happy to spend $45 on two extra wire fees to FDIC protect an extra $1MM….idiots.

I used to ask people what the heck these huge corporations all did to manage their FDIC insurance risks? I always got blank stares in response…now I know…they don’t, oh yea, I’m the idiot. I don’t know exactly what the compensation package of a Silicon Valley Tech Company Treasurer is, but apparently I am more qualified than a significant percentage of them…..call me, I can be made available for the right amount, on a work from home scenario, of course….

If it was not for free/automated bill pay software from banks, automatic credit card debits from vendors, and CD’s, UST’s, and Agency bonds all being available digitally, it would be impossible for me to manage the ridiculous financial environment I have created for myself. Let’s just say I am not sitting on a yacht in the Caribbean, and I have never flown on a private jet in my life, because once you build your fancy little world, you get to spend the rest of your life maintaining it, or it will just fall apart. Technology makes it possible/easier, but you still have to pay dang close attention.

Anyway, check out new issue 3yr Agencies @6.00% folks…(there is a reason all these banks are getting smoked marked to market on the 1.50% paper they bought just a couple of years ago….) Hold them to maturity or don’t even buy them in the first place….not financial advice, not your advisor, for entertainment purposes only…..

Stay frosty out there.

Sam – like your audience, many of our users are their family’s CIO/Banker/Financial Expert, do you think your audience would be interested in having the ability to not just manage the investments and answer questions, but actually create a financial plan for family members?

Like your family our family also sometimes invests alongside one another.

Managing my son’s accounts is somewhat stressful. He only has 6 years left before college so the timeline is getting close. His 529 took a hit during the downturn and we don’t know when it’ll come back. 6 years will be over before we know it. Maybe he can go to a community college as you recommended in the other post. Or go to Canada…

Dear Sam, over 30 accounts. Wow, no wonder you are stressed. In your post you mentioned Fidelity ‘s mobile app. Have you ever done a post on how you handle account security and privacy? Might be useful to readers. Ever feel uneasy listing every account at personal capital or some other wealth aggregation site? Ever feel uneasy setting up ACH between different accounts? Does using Venmo make you concerned? Ever wish you just had everything offline on a master excel sheet at home on a cold storage desktop? Do you use an authenticator app or a physical key like a yuba key? Cheers.

Eric

Funny enough, I feel no stress using finance technology. Perhaps it’s because I’ve an adopter since the late 1990s. I also had $2,000 of my ATM money returned to me after being held hostage in China.

Do you manage your family’s finances? If so, what is your plan?

Sam, loved the book and the podcasts as well. Just got onto the newsletter, great stuff all around! I was wondering with the recent Fed comments if you have a new target for the S&P 500 to hit in order to start buying it again?

Great to hear! If you don’t mind leaving a book review on Amazon, and the Apple podcast, much appreciated.

I’m still nibbling at 3,900. And will just buy more if the S&P 500 goes down further.

For now, it’s all I can eat Treasury bonds yielding 5%+. I feel like it’s a blessing and a wonderful gift to all of us.

Sam, I hear you 100% on this one!

I’m frugal by nature, so I never wanted to pay anyone to manage our $$ or do our taxes. That changed about a year ago and I hired a professional Wealth Advisor and a CPA.

I work at sizable tech company and things are complicated with DCP, Mega back-door Roth, HSAs, ESPP, rollover iras, legacy Roths, a recent inheritance, and the list goes on. 2 years ago, I was laid off from my last company and received a large severance which paid out roughly 60% of my current year salary and 40% of my next years salary in the current calendar year. Combine that with some ill-timed stock sales, and I had to write a $100K check to Uncle Sam on tax day due to bad execution. This was my tipping point.

It has removed SO much stress from my shoulders. I have a solid investment strategy, all of my old accounts are optimized and cleaned up, I get helpful reminders at key points in time, and have pros that are available for questions whenever I need them.

When I divide the fees paid by my hourly wage, it comes out to roughly 100 hours of my time (post-tax earnings). I used to spend easily that much time managing our money late and night and on weekends, stressing out and missing quality family time.

I now sleep much easier knowing that things are being done correctly and have an extra 100+ hours of my time back. Win win if you ask me!

Another great article Sam. Your hard work is so appreciated.

I LOVE managing some of our family money. Someone trustworthy has to do it! I feel it’s part of my contribution to my family and I’m very organized with it. Years ago, I opened up 2- 529s for each of my 3 daughters. I figured by the time they’re 18, they’d have plenty. Plus I think it’s great to show your daughter that women can manage money very well I might add!

“ Plus I think it’s great to show your daughter that women can manage money very well I might add!”

Absolutely! I’m pumped to teach my daughter about personal finance and money management as well. Alas, she’s only three :p

Managing family money is definitely stressful. I originally had my parents money invested in high quality dividend funds – about 40 different ones – then 2020 hit and dividend stocks, like most others, got hammered, and I went to ~40% cash for a while for them and then did a few speculative bits, with large cash and kept most of the div for a while. Now I have 10% in REITs, 40% in short and medium term bonds, and 50% in index funds. I’ve narrowly beat the market for them over the last 5 years but just too much stress. I’m glad I’m able to get them 5% in bonds now finally and going direct in individual bonds vs bond funds. They haven’t been difficult to deal with at all on this but I just feel a lot of responsibility. At least now I feel financially secure enough even if I ended up zeroing them out from investments, I could make them whole again.

I salute you for the stress of helping the family out

Outperforming over 5 years is not easy! Well done.

“ At least now I feel financially secure enough even if I ended up zeroing them out from investments, I could make them whole again.”

Good to know. That’s a good mental trick to have.

Sam, Kudo’s to you for love and care you attend to your family and the financial care you provide to your family. I too am in charge of the family investments. At the early stages, I too let my emotions take over which caused a negative financial decision later, such as selling investments during a downturn, only to see the investment turn around for a good profit later. We learn from experience and are better for it. Sam, keep persevering and keep up the good work that you provide to your family and the Financial Samurai family!

Thank you Eric. The same to you!

I tried managing my mother’s money for years and spent endless hours creating her multiple customized budgets. I genuinely wanted to help. Did she appreciate it or like my help? Debatable.

Perhaps she appreciated it to some degree, but it resulted in tearing our relationship apart. I didn’t give up at first. I let some time pass, and I tried a few more times over the course of a few years. And each time, it just resulted in a ridiculous amount of stress, endless excuses on her part, her starting fights with me, and a negative impact on my health and probably on hers as well. So I finally enough of this and stepped away from it all.

The only thing I still help her with is filing her taxes. She was paying someone over $300 for the most basic type of tax return and complained about it. And the process always stressed her out. It still stresses her out today, but at least I file them for her “for free” so it saves her money. It also gives me a small amount of insight into her financial situation without being too time consuming.

Managing family money is not easy at all. Even if your family is supportive and appreciates your help, it’s still stressful.

You’re doing a lot for your family Sam especially with that many accounts, phew! I appreciate your suggestions on alternatives to doing it all yourself as well. I have been buying a lot of treasuries this year and even some CDs again. It’s amazing how rate hikes can make those investment vehicles so much more attractive again.

As the saying goes… you can only lead a horse to water. It’s great you’ve helped your mom pay down debt and come up with a plan. So long as there aren’t any scammers out there to take advantage, she’ll be OK.

The scammers preying in the elderly are the worst.

Sam, it is a lot of stress to manage the family’s money and respect to you for your management.

My husband and I each manage our own investments and split up paying the bills, largely because both of us are interested in finances and because it takes some of the stress out if we are both involved. What works for us is lots of communication and some guidelines, such as, discussing any investments (which we make in $5,000 minimum tranches) and letting each of us know when each of us spends more than $1,000.

I was a young widow, and that experience made me realize that I am capable of financial management. I’d encourage anyone to begin. By no means am I an expert, I am always learning.

Sam, I am so grateful for all your content. It’s so incredibly relatable. I am the one managing our family’s finances (my husbands amazing but he’s happy to tell me to “have at it” ;-) . It’s not always an easy job but I have become much more reserved as I’ve gotten older having watched so many bear markets (beginning with the dot com bubble/burst as I was working my first job on Wall Street).

I now have two teenage boys who will be going to college in a few years (I’m approaching 50) and for me, capital preservation is now front and center. It’s important that I can put my head on the pillow every night and fall asleep knowing that I’m not going to loose my family’s money. If that means that I forsake the potential stock market gains, even in index funds, then so be it.

Right now, we’re steering the ship, slow and steady and for me that means CD’s and money market funds, and just a whole bunch of boring but safe investment. I was just sharing with a friend yesterday of the Capital One 5% 11 month CD or the Schwab or Vanguard Money Market funds that are now paying over 4.5%. These are certainly respectable safe (sleep well) places to park your money. Yes, it may loose a bit to inflation, but so be it. I value my sleep way too much.

Hi Karen!

“ It’s important that I can put my head on the pillow every night and fall asleep knowing that I’m not going to loose my family’s money.”

So important to rest easy and feel good about our investments. Got to love the 5% yielding risk-free investments as well.

Enjoy the remaining years the kids are at home with you!

Sam

Synchrony also has a 5% CD for 14 months right now. Just bought some for my mother and M-I-L.

Sam I give you a lot of credit for putting yourself out there with your opinions. People can always pick apart what you say, do, or write about. Investing money is always hard. You buy something and it goes up and you wished you had bought more. When it goes down you wished you didn’t buy any. During the big run up in stocks from 2009 to 2020 I would feel sick that I was missing out on stock market gains. I was mostly invested in cds.

One day driving home from work I was complaining to my wife about not making money in the stock market. She said look at that homeless guy standing on the corner with a sign asking for money, do you think he made any money in the stock market today. I got the point.

Your wife is a wise woman. Thank you for sharing this story. To show and feel gratitude regularly is what makes us feel rich.

Thanks for the reminder. I feel grateful to have reader perspectives such as yours.

Do you manage your family’s finances? Yes

If so, do you ever get stressed doing so? When we didn’t have enough money to pay the bills, I did. Now that we are financially comfortable, I don’t.

Do you ever feel like managing your family’s money is a full-time job? No

What are some strategies for reducing stress when managing your family’s finances? I check our accounts once a month. Not only is my time valuable, but obsessing over my account numbers is more likely to lead me to make mistakes or lose sleep. So I think a better approach is hands-off and eyes-off the balance. When I have money to deposit, I put it in without trying to time the market. Since my time horizons are long, I think more time in the market is always better than trying to wait for the perfect moment. I also don’t stress about the optimal funds. I make my best decision at the time of a deposit and then walk away. I revisit my allocations once a year. Could I be richer with a more active approach? Maybe, but I am happier this way.

You’ve obtained master investing status in being able to remove your emotions from investing.

Sadly, I have not been able to, which is why I’ve assets allocated my net worth the way it currently is.

I sometimes feel too much responsibility to take care of my family and optimize their finances, probably because I’m worried about how competitive and cruel the world is and can be.

Perhaps when my kids turn 18, I will feel relief that it’s now up to them to invest and manage their finances.

I don’t know if it has much to do with my kids’ ages (still have two in elementary/middle school), but I think it’s more a reflection of my worldview.

At risk of sounding like a holy roller, I have a very strong belief in God so I trust that no matter what happens, he’ll help us get by. We’ve been through some rough storms in the past so that’s not just a theoretical belief for me.

Plus, I always keep in mind that everything in this world is temporary. I don’t worry so much about losing 16% of my portfolio last year because we still have enough money to pay the bills and someday, when I die, I’ll be losing 100%. Sure, it will be nice to leave my kids a financial cushion, but I don’t think that’s necessary for them to have a happy life.

I like the attitude, everything is temporary!

It’s one of the reasons why I’m doing my best to spend, give, and enjoy.

Ive been managing my mother’s retirement money for over a decade. Fortunately I just split her money between a single Vanguard fund, Wellington, and HYSA and its worked out great for her. But now her sister died last month and Im going to have to make decisions on investing the inheritance shes just been notified she’ll receive. That has taken me down a whole other rat hole researching inheriting 401k etc. tax implications , legal docs showing up my mom has to sign. List goes on. I guess its a good problem to have but it still adds stress , not just financial but my siblings butting in with their opinions and questions.

Ah yes, it gets complicated when an inheritance is involved. You remind to remind others to start a Death File and share it so heirs can easily access your funds.

Sam, with all the resources and knowledge that you and your readers have, wouldn’t it be better for us to invest the potential 529 money in higher interest paying assets?

Sure. Open to suggestions beyond Treasury bonds yielding a juicy 5%+. In my mind, I always think, “Why not do both,” or “Why not do that as well.”

Related post: Ranking The Best Passive Income Streams

It’s hard to want to out more $ in index funds within 529s since both of mine Utah and NC have spiraled down 15-20% with the rest of the market, and no end in site. My oldest is 4 years away from college. Bummed I can’t convert to a CD within the 529 to preserve value? Any thoughts? Keep in index funds????