Cash management is important during bad times, but also during good times. Give the increasing volatility in the stock market, cash management is even more important to manage stress.

At any given time, every investor must always decide three things:

1) How to invest their new cash flow

2) How to invest their existing cash

3) How to reposition their existing investments if at all

As long as enough money is coming in to cover your expenses, life is fairly good. As our cash hoard grows, there's also less financial stress because you can more easily cover unanticipated emergencies like a furlough.

Cash Management Recommendation

In general, having 6 – 12 months of living expenses in cash or cash equivalents is good enough for the average person to sleep soundly. When there were bank runs occurring at various regional banks, cash management was even more important!

The FDIC only insures $250,000 per deposit, per insured financial institution. One work around is to add another owner to your financial account. The other solution is to open up money market accounts with multiple top financial institutions.

There might come a point, however, when you will have excess cash. Perhaps you were undisciplined in your monthly dollar cost averaging strategy or maybe you got a bigger windfall than anticipated. Ironically, having too much cash might make you poorer over the long run as cash tends to underperform other risk assets.

Eventually, if you have too much cash, your financial anxiety will be replaced with the fear of missing out on potentially bigger gains in risk assets like stocks and real estate. Given your peers are all getting rich, you will want to follow suit.

If enough greed kicks in, you will end up taking on more risk than you can comfortably withstand, and sometimes bad things will happen. Your financial stress returns once again. Hence, one benefit of following Financial SEER.

Managing Financial Stress Is A Constant

No matter how much money you have or how much you make, you will always have to work on managing your financial stress. After all, the more money you have, the more you have to lose! When you are broke, you've only got upside.

Money is mental. Psychology is why during market sell-offs, there will be headlines about stocks re-testing Great Depression lows. And during bull runs, there will be headlines about how the sky is the limit and you just can't lose. Hence, the importance of cash management.

I didn't do much right financially in 2018 except for continuing to aggressively save. But I did make one move with my existing savings that helped reduce financial stress.

Not only is cash management about stress management, more cash also helps give you more liquid courage to take risks. If you have a lot of cash, you can invest in more assets, quit your job, take a break, relocate across the country, and so much more.

Managing Stress Through Savings

Back in early 2018, I was getting nervous about the stock market. We'd seen an almost 10% pullback in February that jolted me awake. Ever since I left my day job in 2012, I'd been regularly plowing the majority of my cash flow into the stock market and San Francisco real estate market.

After all, my #1 goal is to earn enough passive income so neither my wife or I have to go back to work. With private school expenses, we have a goal of earning at least $300,000 a year in passive income to stay jobless.

With two young kids in San Francisco, we want to generate about $300,000 a year in investment income to live a middle-class lifestyle.

When the correction hit in February 2018, I realized my risk exposure was too high for my comfort. As a result, I slowly started reducing my stock allocation from 70% to 52% as stocks recovered into the summer.

But when you reduce your stock exposure during a rising market, you begin to question your decision because you start getting greedy. You start imagining whether you're missing out on more gains by being too conservative. I was tempted to take on more risk again.

Increasing Savings

But when I got an e-mail from CIT Bank that they had raised their money market rate to 1.55%, I beat back my greed. Just a year earlier, money market rates averaged well below 1%. I still remember only receiving a 0.1% money market rate circa 2015.

1.55% for a money market rate and 2.25% for a 12-month CD rate seemed pretty good. As a result, I decided to lock in a 2.25% guaranteed return for 12 months on July 16, 2018, instead of investing the money in the S&P 500 or the forever tempting FAANG stocks, which I was already heavily overweight, given I live in San Francisco.

As soon as I bought the 12-month CD, I felt a sense of relief. I remember thinking to myself, “Ah hah! Nobody can take away my money now!” I felt my stress melt away as I could now focus on more enjoyable things in life.

Although I'm only earning about ~$190 a month in interest income, it feels wonderful to know my money is secure. Because I generate excess cash flow every month, I constantly have to figure out where to invest the money in order to at least keep up with inflation.

Locking up money in long-term private investments or illiquid investments like real estate enables me to stop worrying so much about how to reinvest my money for years.

Stay Financially Disciplined

As an investor, you must not only come up with some reasonable earnings and valuation forecasts, you must also take action based on your forecasts.

Years ago, my analysis said that 2,800 on the S&P 500 was close to fully valued. We were almost back to the peak seen in January and I told myself if we got past 2,800, I would dial down risk, and that's what I did in July.

The S&P 500 continued to rise until September when it reached 2,929 as the bull market raged on.

Was I fighting the urge to chase the momentum? Of course. But I still had 52% of my public investment portfolio in stocks, so I was still benefitting, although not to the fullest.

Today, the S&P 500 has rocketed above 5,000! But it was above 6,000 until Trump initiated trade wars with the entire world at once! It just goes to show that investing in the S&P 500 for the long-term makes the most sense. Quit day trading.

Manage Risk Exposure

It was also important for me to remain disciplined and look at my overall risk exposure and net worth. I never want to have more than 30% of my net worth in equities. However, I was bumping around that upper limit due to the reinvestment of part of my house sale proceeds in equities.

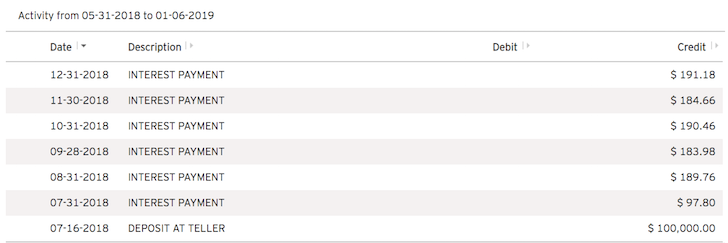

If I had invested $100,000 in the S&P 500 on July 16, 2018, it would have been worth roughly $104,600 by September 30, 2018. But on December 17, 2018, it would have declined in value to just $86,000.

At the end of the year, the $100,000 would have rebounded to $90,600, but still down a hefty 9.4% since July 16, 2018.

Related: How Much Savings You Should Have Accumulated By Age

Returns From Cash Management

Meanwhile, since opening the 12-month CD, it has thus far earned $1,038 in interest for a return of 1.038%. In other words, the difference between this 2.25% CD and the S&P 500 was roughly 10.438%, or $10,438 from July through Dec 31, 2018.

Therefore, the next time you scoff at a money market or CD account rate, don't. Not only can a money market or CD account drastically outperform risk assets, but they also have the added benefit of giving you incredible peace of mind during a downturn.

All I was thinking during the 4Q2018 meltdown was why I didn't put more money into a CD or money market account. If I had invested my entire House Sale Fund, it would have earned $3,750 a month, or $45,000 a year with absolutely zero stress.

During 4Q2018, there were many mornings where I'd naturally awaken by 4am because my mind couldn't rest knowing that another meltdown might possibly be right around the corner. That wasn't very healthy and a sign that I still had too much at risk.

Then, March 2020 happened. Thanks to cash management, I had over $200,000 in cash available to invest. One I wrote my post, How To Predict A Stock Market Bottom Like Nostradamus, I bought $200,000 worth of stock after a 32% correction.

Time To Lock In Another Win

After such a long bull run, my current goal is to re-build my cash hoard. Cash management is more important than ever with recessionary fears on the horizon and an aggressive Fed.

Thankfully, rates are higher today. Money market funds and Treasury bonds are paying over 5%, which is a nice risk-free rate to earn.

Good cash management is about having a good balance in your net worth.

Further, I'm always looking for real estate opportunities, which is why I always need a good amount of cash. I think buying rental properties now is getting more attractive as property prices decline due to higher mortgage rates.

Investing Cash Into Real Estate

With the cash that I do have, I'm also investing in real estate crowdfunding in deals across America. Real estate crowdfunding enables you to surgically investing in individual deals or private eREITs without a huge downpayment or having to take on leverage.

Real estate is a tangible asset that provides utility and a steady stream of income if you own rental properties. Its value will hold more steady than stocks, which is one of the reasons why I like to invest in real estate.

Check out my preferred private real estate platform: Fundrise.

Fundrise enables investors to diversify into real estate through private real estate funds. Fundrise has been around since 2012 and now manages around $3 billion. It predominantly invests in Sunbelt real estate where yields tend to be higher and valuations tend to be lower.

I've personally invested $954,000 in real estate crowdfunding to take advantage of lower valuations in the heartland of America and across the US. My real estate investments account for roughly 50% of my current passive income of ~$300,000. If you don't like investing stress, having a diversified real estate portfolio will help.

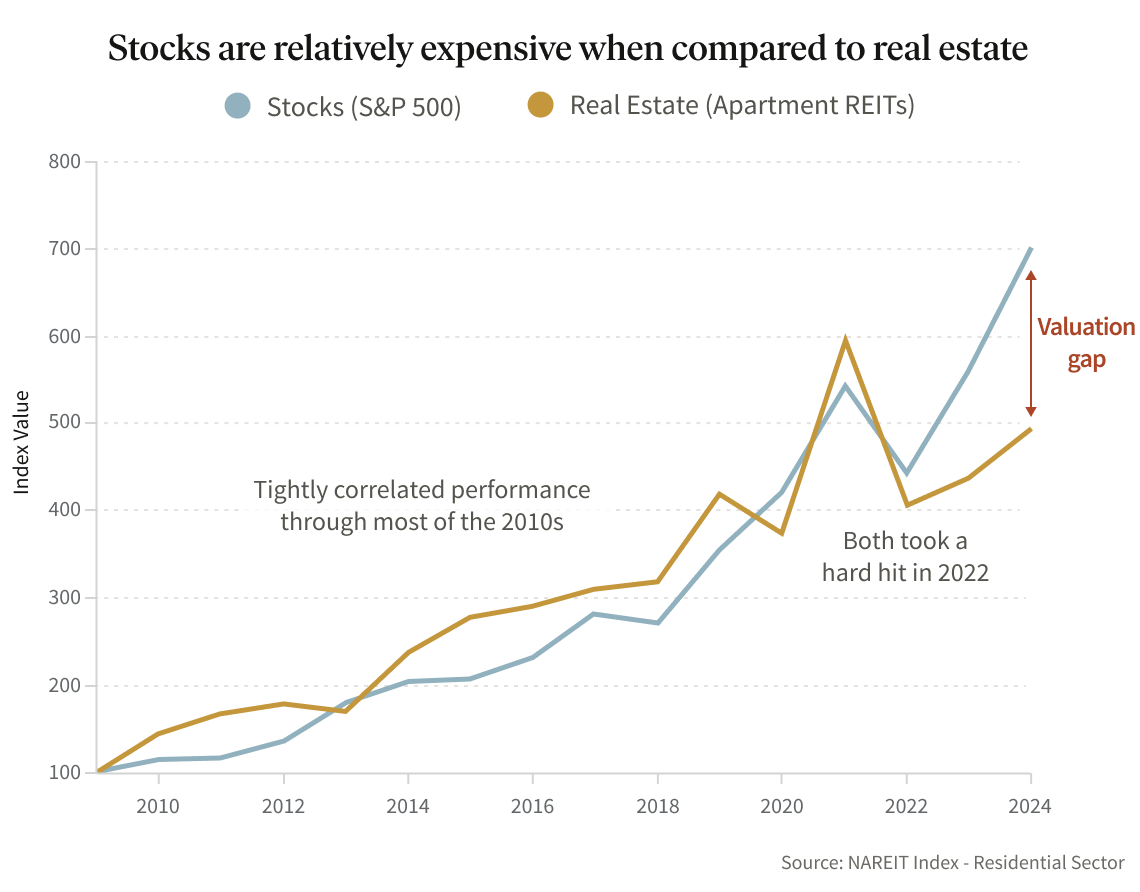

The valuation gap between real estate and stocks is attractive, which is why I continue to invest in residential commerical real estate today. Given the investment minimum is only $10 with Fundrise, it's easy to do.

Invest In Private Growth Companies

In addition, consider investing in private growth companies through a open venture capital fund. Companies are staying private for longer, as a result, more gains are accruing to private company investors. Finding the next Google or Apple before going public can be a life-changing investment.

Check out Fundrise's venture capital product. It invests in the following sectors:

- Artificial Intelligence & Machine Learning

- Modern Data Infrastructure

- Development Operations (DevOps)

- Financial Technology (FinTech)

- Real Estate & Property Technology (PropTech)

Roughly 65% of the Innovation Fund is invested in artificial intelligence, which I'm extremely bullish about. In 20 years, I don't want my kids wondering why I didn't invest in AI or work in AI!

The investment minimum is also only $10. Most venture capital funds have a $250,000+ minimum. In addition, you can see what the venture product is holding before deciding to invest and how much. Traditional venture capital funds require capital commitment first and then hope the general partners will find great investments.

Both Crowdstreet and Fundrise are sponsors of Financial Samurai and Financial Samurai is currently an investor in Fundrise.

Financial Samurai is one of the largest independently-owned personal finance sites that started in 2009. I help people live the lifestyles they want.

Hi Sam,

Really enjoyed the article, thank you. Comments are interesting – we make the assumption that the stock market long-term is a for sure thing. Nothing is for sure. I like your method of looking at what can I earn in a year risk free vs. non-risk free. I think to lock up 6.5% guaranteed was super smart. That’s a decent return for taking limited to no risk.

On the CDs.. I’ve been considering them. 2.45% isn’t bad risk-free especially vs. treasuries as you pointed out, but given you’re in the highest tax bracket, isn’t this pointless? Why invest for a 2.45% return in a savings account? From a tax perspective, you’re earning income from the worst place. It’s like a W2!?!

Sam, did not realize you were only talking about specific funds to buy the house (not sure that’s clear in the post) but now understand your actions if you’re using the funds in the next 24 months. I’m in a different place than you since I’m mid 50’s and no plans for significant cash needs in the next 10 years and will likely work for another decade in a job I enjoy even though I could retire now and live pretty comfortably. Good luck on the new house -sure you’ll hear from many friends on the mainland that haven’t been in touch for years once you move to Hawaii!

Cool. I write in the post in bold that the money is for buying another house towards the end. Maybe it is simply not clear enough.

I have multiple investment accounts for multiple purposes. I’ve always been under the assumption that most people have the same? I’ve written many times about the importance of building an after-tax investment account or two for financial freedom and passive gross income.

Perhaps there are a lot of people who just have a 401(k) or something and that’s it to survive on?

Check out: https://www.financialsamurai.com/new-three-legged-stool-for-retirement/

Don’t die with too much my man!

Sam, I just don’t get the focus on calendar year returns and making adjustments based on what happened between Jan 1 – Dec 31. Isn’t this simply trying to time the market and focusing on short-term returns? If you pull back to 10,000 feet and really think about this time interval in relation to your total investment horizon, it’s just a blip. This just seems opposite to what every true investor sage from Jack Bogle to Warren Buffet warn against so would love to hear more about why you’re choosing to use this time period and how this will be of benefit in the long run. Not criticizing, just perplexed.

Exactly right. You always need a purpose for your money, otherwise what’s the point of saving and investing? To die with too much?

My purpose for my House Fund is to… surprise, surprise, buy a new house within the next 24 months.

What is the purpose of your investments?

Instead of 12 month CD, why would you not just buy a 12 month T-bill?

If it has a higher rate after taxes.

Sam, could you explain why you want your max net worth in equities capped at 30%?

I noticed the pie chart on the high net worth composition article you showed 50-60% of net worth in equities.

Great post Sam

2018 was The year indeed to cash some wins (especially in single stocks and especially in FAANG) and secure them in juicy CD/MM/treasury at almost 2.5%

Even though market can and will rebound, the peace of mind is priceless especially if you are in your 40-50’

Nice one!

I also set my theme to “live the good life” for 2019. Already seems profitable.

Let’s see where the markets will take us – wouldn’t be surprised for 10% in any direction either.

For those considering CDs or high yielding savings accounts, be aware that the IRS considers the income as Ordinary Income, meaning that it is taxed at the rate your AGI is typically taxed at (given that the CDs are in a taxable account).

Also, be aware that while investing in ETFs like SPY and QQQ can be like owning the entire stock market, they are market-cap weighted funds, so a large proportion of a position in those would be concentrated in the giant companies that comprise the S&P and Nasdaq. And sometimes giants blow-up, break-up, or get regulated into ground chuck.

*Raises eyebrow of suspicion at Google and Facebook*

Wow 2.45% is surprisingly high for no lock-up required – I always saw US cash accounts as way lower than our Aussie cash options, but that’s sneaking up to our ING Bonus saver rate of 2.8% here. Didn’t appreciate how quickly the Fed was lifting rates :)

The Reserve Bank rate is only 1.5% and the Fed is at 2.5%…

Foot on the gas for me.

I always respect your thought process. You have a succesful online business to give you confidence to maneuver. My worry is still not hitting my goals far more so then hitting a set back in the next decade.

The great part about investing is your pile of money is never going to be needed all in one year. So if you have the luxury of already being wealthy why not dial back risk. For those with a net worth under 3 million I think they should stay aggressive.

Many of your readers still have over 5-8 decades ahead of them. Invest for the long term and have reserves for the short term.

I took out 2 CDs last year with the hopes of having real estate that makes sense to buy pop up….still nothing yet.

Very cool. Go big or go home! Are used to love those days in my 20s. How old are you?

I still gamble with about $500,000 a year to see if I can hit some homeruns. Because as they say, no bet no win!

That is a solid amount of cash to be betting with!

I am 28. Happy to be where I am net worth is basically your gambling fund.

I have actually found it has become more stressful as you mentioned to deploy cash (bonus) these days.

As you age kids, nicer houses, vacations etc all compete.

I still can’t beleive that working hard and investing the last 6 years has gotten me here.

Anyways thanks as always for the fun motivation!

I will be the gambler in the corner buying small cap value!

Makes so much sense! I opened a CD and savings account at good rates which I feel good about. I’m going with slow and steady this year. I also plan to keep investing each quarter and stay conservative in my allocations too.

Love passive income, hate paying taxes. My goal: 250k passive income from a tax free municipal bond ladder. Currently under construction.

That’s well and good I guess. But that is like 8 million dollars!

By reinvesting the returns the compounding will be magical; I can get a safe 4% tax free return on Munis so 6M should do it. Even at a smaller account size, 4% monthly tax free vs. 2.4% taxed seems preferable in creating stable passive growth.

Hard to get 4% on munis right now, unless you are dipping in quality and going out 30 years (or paying high premiums for high current cash flow – which I don’t disagree with), but 4% YTW is hard with rates where ty are. You should look into some zero coupon minis if you’re trying to “accumulate” on a tax free basis maybe? Worth a look and offers attractive yields if you don’t need the current income.

Great input Phil, thank you.

Hey sam, good article but broken link on “looking to buy a new house”. I must have missed that one so wanted to read up

Honestly, right now I don’t see market going much higher or getting close to the highs it was at… I’m by far a knowledgable investory, but I’m tempted to move all my 401k holdings 90/10 AA into a cash fund for the short-term until the market tanks which it will imo.

I’m 20 yrs from retirement, more likely 25 yrs.

thoughts?

Stop thinking that you know what the market is going to do – trying to time the market is a classic mistake. With 20-25 years until retirement, my guess is your goal is wealth accumulation. Sam’s at the opposite end of the spectrum – he’s focusing on wealth preservation. You should be embracing risk and the accompanying expected return. A recession 20 years away from retirement shouldn’t affect your strategy. Sam’s losing sleep of equity exposure, so a larger cash position is appropriate for his goals.

25 years is an eternity. I agree with Dan.

Take whatever you are up so far this year + a risk free rate and compare to expected stock market gain. Which do you choose?

I’m up about 5.4% this year. So I had 2.45% to get 7.8%. I like this guaranteed return, so that’s good enough for me.

Using CIT here too… 2.45% seems awesome to me given the political climate we are in.

When you say your goal is to have passive income of $250,000, does that include income from Financial Samurai? I would consider that a job given that you spend a significant amount of time doing it. Doesn’t change the math, I’m just curious at how you define “passive.” Thanks.

$250,000 is our passive income goal. Here’s a post on the details. I need to do an update soon, especially now that yields are much higher.

I absolutely agree it takes work responding to you and other commenters.

What’s your passive income goal and how are you coming along?

I live in a LCOL and my kids are grown. My passive income goal is $200,000 per year. I could get there, but I’ve invested in some longer term, illiquid assets that don’t provide income. I’m not anxious to stop working so I’ll let those grow and then reevaluate later.

Thanks for the great Money Market recommendation with CIT- I just opened an account! Way better to sleep at night with money there instead of crazy market. Thanks for all your hard work Sam.

You can report just about whatever stock market return you wish just by picking and choosing the starting and ending dates. That is why I do not put much “stock” in these comparative discussions.

And most often the lowest price is used as a comparison even though most investors tend to “buy high and sell low.” So this is my favorite comparison. Inflation-adjusted, the S&P 500 gained about 800 points from its October 2007 high to yesterday. That is about a 43% return over about 11 years. It is misleading to just divide by 11 but doing that reveals about a 4% annual return.

Given the extremes involved that’s not bad. So if your time horizon is ten years or more, as in many retirement accounts, the market may indeed be the best objective, nonetheless gut-wrenching, choice and short term moves should be ignored if you have a good allocation.

Money outside retirement accounts falls into a different category. You need at least a year’s living expenses in the bank.

If you are the are the rare person who will eventually be paid for not working, well you may need a little less.

There’s actually no debate about the S&P 500 performance in 2018. It was down over 6%. Cash outperformed.

Remember the three things and every investor must do. Cash management is about living a better life

That’s just because to picked 2018. Most people did not invest on January 1, 2018, and dis-invest on December 31 of 2018, so that limited short-term analysis is actually of little use.

Pick different dates to get different returns. September 2017 to September 2018 the S&P 500 is up, same for YTD 2019.

For the individual person, it’s when they bought and sold the stock. Have stock but did not sell it, well you have no actual gains or losses – it’s all talk.

Remember, we’re talking about existing cash flow or existing cash.

Every month or every year is a new period.

Eventually, you should spend your money, otherwise there’s no point.

Huh?

If you were invested in SPY on January 17, 2017, and sold today you would be up about 13% plus dividends.

Even if you invested at the 2007 high you would be up about an estimated 4% a year plus dividends,

They each beat cash hands down. It is hard for cash to rival stocks overall with these low interest rates.

Now if you are telling me you know when to get in and out of the market, when to a have more cash and when to have less, I would say you are going to be wrong most of the time, but good luck.

Personally, everyone else was the most negative is when I got positive, even though my investment horizon limits my exposure somewhat.

I remember hearing the recently departed investment genius Jack Bogle say “its easy to be out, but who is going to tell you when to get in?

In any five year period I have never seen that advice to be wrong. Here is a link to his five bits of investment advice.

https://www.nytimes.com/2019/01/17/business/mutfund/john-bogle-vanguard-investment-advice.html

Here they are in case the link does not work.

1. Stay the course

2. Beware the experts

3. Keep costs down

4. Don’t get emotional [The toughie]

5. Own the entire stock market

Bob,

Your quoted returns don’t count dividend reinvestment which historically is half of your returns.

Who’s misleading who?

Misleading hmmm. I think you need some work on communication skills. And is that true that dividends are half od returns, anyone, Sam?

I mention an estimated return plus dividends. The point is stocks typically outperform cash over most multiyear periods. Yas 2018. I guess we could go back to Voelcker’s day when a 30 year bond as a great long term investment. I don’t see that happening now.

I think, or hope readers know that stocks usually outperform cash over the long run.

However, the topic of this post is about cash and stress management, as everybody should have some cash, that should be optimized.

If you double your money every 14 years I wish you a long life.

Thanks! The money is just there for my family and for target organizations as I had enough when I left work in 2012. But I got really lucky because of the bull market.

How about you? How did you do last year and how are you investing this year? Hope you are enjoying retirement life as well.

And to make your point some folks sound rather stressed!!

It definitely seems like some people are quite argumentative about returns when this post is just talking about cash optimization. It’s kind of weird that people have gotten triggered. Maybe it’s because they did so poorly last year and I have so much anxiety that has carried over to this year?

One guy just told me that I am lucky that’s all. When you lock in a gain, that’s not really luck.

Yeah, not sure. Everybody should just do what they think is right for them. Not sure why every time I write about what I’m going to do or did with my money, some folks get up in arms.

I would question the value of cash assuming you have some equities or other near liquid asset.

Nearly everything can be paid on a 30-day 0% float (Credit card grace period) and that’s enough to cover a short term cash flow issue. If the thesis long term is that equities outperform cash, why have much of anything in cash?

For that matter I do keep a small HELOC (5.25% as of this month) that I can write checks directly against if required too.

Cash at 2.8% just seems awkward in comparison, and if we are playing with HELOC’s anyway one probably gets a better return than that simply doubling up on a mortgage payment?

Admittedly with most people’s mortgage rates probably at the lowest we will see in our lifetime (or near as) there’s wisdom to letting that ride I guess.

For sure. You’ve got to do what’s right for your. Look at your net worth. If you’re happy with it, great. If you’re not, then changes need to be made.

Sorry Bob,

I don’t mean disrespect. Just trying to point out dividend reinvestment skews the results. I’m a stock guy as well.

Thanks, Bill

Thanks for the post. My wife and I are still in the accumulating wealth stage of life. While I didn’t enjoy the tanking of dotcom or the real estate crash, we laughed as our net worth plunged. I’m pretty sure we’ll feel the same way even when it happens again. Of course, if we don’t, well….too late then to do anything about it.

But I love these posts because it’s having me plan ahead 10 to 15 years when I’m pretty sure my viewpoint is going to change considerably. Just gotta get to that big nut still!

I’m continuing to DCA on my 401k. I’ve got more than a decade to even begin thinking about retirement. I’m happy to know that I’m probably contributing at lower prices, but I don’t want to be depressed and log on to look at my account value.

I’d look into the money market route if I was in the preservation stage I suppose, but I’m far from it right now, unlike you.

Quick question – I see people talk about ratios of net-worth in stocks, real estate, liquid assets, etc. When speaking about real estate, how do you measure % of net-worth? Is it the equity you have in the property? I hope this question is clear… I’m not sure how else to word it! :)

Conservative equity value.

https://www.financialsamurai.com/why-its-ok-to-include-your-primary-residenc-in-your-net-worth-calculation/

For free and clear properties, I use conservative current market values less 10 percent selling expenses. For mortgaged properties, I use conservative current market values, less 10 percent selling expenses, and I subtract the current mortgage payoff amounts from the results.

It’s fun to look at Personal Capital’s values, which are based on Zillow values on the asset side less the remaining mortgage principals on the debt side, but that approach is not accurate.

I’d measure shares in total assets rather than net worth.

Sam, thanks for the post. One suggestion:

Even better than the 2.45% MM option is an 11mo no penalty cd offered by the likes of Ally/Marcus.

You give up only 10-15bps in annual yield, and will gain the rate lock for an 11mo period. Liquidate for -0- penalty anytime after the first 7 days. IMO it’s a no brainer given the money market option is a variable rate and there is real potential of cash yields going lower over the short/medium term.

2.25% is also just they’re straight savings account rate–no risk of your buck ‘breaking’ like money markets in ’08!

I like short term treasuries myself. No state income tax on taxable funds. Vanguard treasury-only money market fund is paying 2.33 percent compound yield today. Today’s Treasury bill auction looks like 2.36 percent on the 4 week bills and 2.37 percent on the 8 week bills.

Take a little more risk with Vanguard’s prime money market for 2.49 percent compound yield and pay state taxes if it makes sense.

Several good 1 year CD’s at 2.85 percent. Look at depositaccounts.com for reliable rate information.

I looked into Vanguard’s prime money market account but the lower comparable yield in the Treasury-only money market fund makes more sense if you face a higher state income tax bracket. The loss of ~15 bps is made up for by having a lower tax burden.

2.85% on a CD is crazy to think about. Just 6 months ago, Sam quoted his 1.85% CD rate in the post. 100 bps in that amount of time is wonderful if you’re a saver like me. I doubt we’ll see a similar upward swing in the next 6 months given the market’s hostility to Jerome Powell’s now-dated comments following the last FOMC meeting.

It’s wonderful only if inflation remains low.

I’m keeping taxable savings in short term accounts because I plan to do capital improvements on rentals this year and pay off another rental mortgage that’s above 5 percent. There is a minimal premium for locking cash up for over a year at this point anyway.

I agree, short term Treasuries give comparable or even higher rates than similar term CDs, and with considerable tax benefits, especially in California. Given Sam’s desire to avoid taxes whenever possible, it’s odd he didn’t mention them.

Yeah short treasuries are far more preferable than CD, Money Markets or funds – no fees, highly liquid and no state income tax. Right now on Schwab short treasuries are earning more than CDS for up to 1 year tenors – doesn’t make sense.

You would still look up your money in treasuries if you plan to buy a house within the next 3 to 6 months? Why take the risk for an extra .05%? Seems unnecessary.

Quick question. If someone invests in Vanguard treasury-only money market fund.

1. Can they get the money out in 3-6 months

2. Will we still get interest for the 3-6 invested months

3. Why is there no state tax

4. You still have to pay federal tax right

Inflation for 2018 was 1.9% so the 2.25% only netted you .35% right?

Which is fine for preserving cash as part of your asset allocation…

A +0.35% real rate of return is so much better than a -8.3% real rate of return in the S&P 500 if you want to put it that way.

How did your investments do in 2018? Not very well I can imagine based on your comment :)

I was up only 2%. Or a real rate of return of only 0.1%. But I’m so happy because I outperformed and didn’t lose money.

Down $0 in 2018. Unrealized losses are just that: unrealized. I didn’t have to rebalance this year…the market did it for me. :)

Ask me in 10 years when I start withdrawals if I would have been happier invested in the S&P 500 vs CDs.

Total net worth and cash held steady and being long it means it doesn’t much matter what the market does year to year.

Down is better as I’m still accumulating.

Going to start dropping from 80-20 to a 60-40 allocation over 10 years as I get closer.

I’ll care in 2029 if the markets are cratering but by then I’ll have a more conservative portfolio.

Sorry to hear about the performance. But that’s a good way to look at things so it doesn’t hurt as bad.

10 years is a long time to keep accumulating so I guess that’s fine.

Lol…lifetime performance of new 2018 investments will be better than lifetime performance of new 2017 investments.

I’m happy to be a boglehead and not stressing small market shifts. -8.3%? Yah, really don’t care. Been around a while that that’s a pretty mild drop.

10 years is actually a small amount of time to be accumulating and I just bumped my total time horizon out quite a bit. Should be interesting to see how everything plays out.

If you are worried about the annual performance (down about 4% after 2% dividend) of the S&P 500 then you are doing the whole investing thing wrong.

Put any money you don’t need for 10+ years in 100% stocks and don’t look at it. If you do that every month then you just discounted your entire portfolio all year long.

Need money before 2 years? Money market/CD/Tbills, whatever you want to do.

2-5 years – nice conservative 30/70 mix

5-10 years nice 50/50 mix

I just helped you build and protect your wealth in the most simple painless way possible and as the years move on, just pull what you need down the conveyer belt of safety.

Sam, we’re strongly considering making the same decision with money we’ve set aside for a down payment. We can’t thank you enough for your quick reply a few weeks back.

The market volatility had shaken our nerves but luckily staying the course proved the wiser choice. We’re approaching a decision point where we need to decide how to handle our remaining down payment funds which aren’t safely locked away in a high-interest savings account or Treasury bills.

The stress that comes from managing all the cash I would otherwise have invested has been stressful. I’ve got FOMO on the brain but do feel comfort from seeing the monthly interest deposits or payments hit our accounts.

I’m in a true saver mindset now and it helps with my cash and stress management. Thankfully, yields have crept up to something more respectable for those who wish to keep their assets liquid and in less-risky holdings.