Liquid courage is sometimes needed to talk to a person you fancy. The more alcohol you drink, the more your inhibitions tend to go away.

In the finance world, liquid courage is also what's needed to make risky investments or investments during risky times. The more cash you have, the more liquid you are and the more guts you have to put money behind your beliefs.

Even though holding a lot of cash can be a drag on performance, you just never know when investment opportunities may arise. As a result, I believe it's prudent to always have roughly 5% of your investable capital in cash.

The Courage To Invest Starts With Having Lots Of Cash

Since I left work in 2012, I've considered myself a relatively conservative investor for my age (34 to 44). Without a steady paycheck, my cash flow is unpredictable. Further, my wife doesn't have a job either and I also have two young children to feed.

When it comes to measuring my risk tolerance using the SEER methodology, I'm unwilling to give up more than six months of my life to cover potential bear market losses. Whereas some of my friends my age are willing to give up two years or more of their lives to make up for any losses.

Given my situation, my public investment portfolios are diversified. I own a lot of equity-linked structured notes in one portfolio because I wanted to hedge against downside risk. In another portfolio, I have almost half the portfolio in individual municipal bonds.

Further, I'm more interested in investing in real estate because it is a tangible asset that is less volatile and tends to produce more income.

While you won't find me going on margin buying equities, I have no problem leveraging up to buy real estate. A seemingly paradox, but one that is grounded in my belief real estate is less risky than stocks.

Despite my belief in being a conservative investor, maybe I'm mistaken. The other day, I was discussing the investing landscape with a friend who made me reconsider my risk tolerance. With 100% of my rollover IRA in equities, and 70% of the equities in individual tech companies, perhaps my investment risk profile is more risky than I though.

If you talk through your investment moves with a family member, you may realize you are much more aggressive as well. If so, changes may need to be made in order to not lose an unexpected amount of money in the future.

Examples of some of the riskier investments I have made since early 2020:

- Bought ~$250,000 worth of the S&P 500 in March and April 2020 – How To Predict A Stock Market Bottom Like Nostradamus

- Borrowed seven figures to buy a house in the summer of 2020 – Real Estate Buying Opportunities During COVID-19

- Bought ~$25,000 cryptocurrency and HUT (ethereum miner) in June 2021 – How I'd Invest $100,000 Today

- Buying $40,000 worth of LTH, a health and fitness stock in October 2021 as a laggard reopening trade for 2022

- Bought $100,000 worth of S&P 500 and $50,000 in the NASDAQ in January 2022 after the market correction

- Bought a true forever home in 2023 with mortgage rates at 17-year highs because I could pay cash and get a great deal.

- Invested $143,000 in Fundrise's venture capital product in 2024 because of its exposure to private AI companies. I wish I invested more as Fundrise Venture went up 43.5% in 2025.

Having Cash Gives Me The Confidence To Invest And Hold On

All these investments required courage, especially buying the house on leverage right after lockdowns. I'll discuss my house-buying process in a future post as it was a real knee-knocker.

I'm not sure a truly conservative investor would have made these investments. Rather, perhaps a conservative investor would have just kept raising cash or bought bonds instead.

The only way I could have made these investments is if I had some cash left over AFTER making each investment decision. Liquid courage was paramount in taking these investment risks. The leftover cash would serve as my buffer in case the investments went sour. In other words, having cash gave me the confidence to take risks.

It's worth recognizing that in a bull market, everything tends to go up. Therefore, making the above investments wasn't anything special. What's important is having the liquid courage to put capital to work during downturns.

It is the mobilization of capital and the appropriate asset allocation of capital that makes up the most important part of your returns over time. If you can recognize long-term investment trends and invest accordingly, you will likely do very well.

Researching and buying individual investments is fine. Just make sure you mainly focus on your overall asset allocation.

The Ideal Amount Of Cash An Investor Should Hold

The answer to the ideal amount of cash an investor should hold is subjective. We all have different risk tolerances, objectives, obligations, and cash flow. But let's try to figure out an appropriate level anyway.

Every day, as stock, real estate, and other risk asset prices go up, you might feel bad about missing out. However, this bad feeling only starts occurring when you hold a certain amount of too much cash. After all, your existing investments are going up.

On the flip side, every time there is a major correction, you may feel bad not being able to invest if you don't have enough cash. Therefore, the key is to figure out the ideal cash amount where you feel neutral.

Below is a fantastic chart that shows the stock market losses and how often they occur by percentage declines.

Figuring Out How Much To Cash To Hold Based On The Following

- Stocks tend to increase in value each year by 10% on average

- The average daily movement of the S&P 500 is between +0.7% and -0.7%

- Corrections of 10% or more tend to occur every 1.8 years

- Bear markets of 20% or more tend to happen every 4-5 years

- Real estate tends to increase in value each year

- Real estate tends to go through cycles every 7-10 years

- REITs has been one of the top performing asset classes over the past 20 years

- It's very hard to time the market, which is why dollar-cost averaging is recommended

- New cash is always being added to your investment portfolio

- The longer a bull market extends beyond the average duration (4.8 years), the more cash you should have

- Differentiate between cash in your investment portfolio and cash used to pay for life's emergencies

Bear Markets Are A Part Of Investing

Over the past 72 years, there have been 13 bear markets. Each bear market lasting an average of 13 months, with declines averaging 25.8% before markets recovered. In contrast, the 14 bull markets since 1949 lasted an average of 49 months. They gained an average of 131.8% according to Putnam Investments.

Given these facts and assumptions, it would be wise to always have a majority of your capital invested and a minority of your capital held in cash. A minority of your capital in cash can range from 1% – 49%. At the same time, you never want to fall into a stressful liquidity crunch where you are forced to sell assets.

Personally, I believe the right percentage of capital held in cash should generally hover around 5%. It can go up to 10% in an extended bull market. Again, this is different from the cash you hold to pay for life's emergencies.

If you accumulate too much cash you could actually end up poorer over the long-term. The reasons why include cash underperformance, the difficulty of investing a lot of cash, and the propensity to spend cash on things that don't generate returns.

Ideal Cash Amount: 5% Of Investable Assets

Let's say you have a $1 million portfolio. 5% equals $50,000 in cash. Does that sound appropriate? It depends on your portfolio composition and investment outlook. You also need to calculate how much new cash you are contributing to your investment portfolio each month.

If your “cash replacement rate” is 100% each month (contributing $50,000 each month), then perhaps having 5% in cash is unnecessary. You can have more than 95% of your capital invested. However, you probably shouldn't be 100% invested since you never know when another opportunity will arise.

Let's say the portfolio is 100% invested in the S&P 500 and the S&P 500 goes up 10%. The return would be $100,000. Now let's say 95% of the portfolio was invested in the S&P 500 with the same 10% increase. The return would only be only be $95,000.

However, let's say the S&P 500 corrects by 10% in month six and still closes out the year +10%. If you were able to use 100% of your 5% cash to buy when the S&P 500 was down 10%, your $50,000 in cash would have returned ~22%. The total return would be ~$110,000 or $10,000 greater than if you had invested 100% in the S&P 500.

Of course, this scenario means you need to perfectly time your cash investment. And as we all know, retail investors have poor investment timing.

Adjust Your Cash Up And Down Depending On The Environment

Therefore, if you believe the bull market has a lot of room to run, you want your portfolio to always be as close to 100% invested as possible. Having no cash can also save you from making bad investments. For example, Wall Street is forecasting the S&P 500 to finish 2025 up another 8% or so. Therefore, you may want to be overweight equities again.

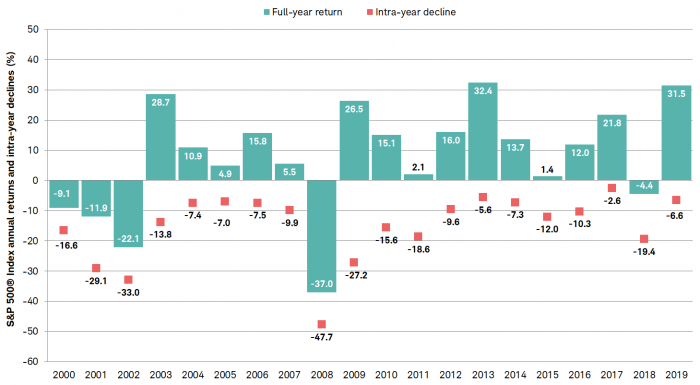

The below chart shows the intra-year decline in the S&P 500 from 2000 – 2019. Having cash to buy the dips or use as a buffer is helpful.

Ideal Cash Amount: The Case For 10% Of Investable Assets

Given we're about eight years past the average duration of a bull market, increasing your portfolio's cash to 10% may be prudent. Does having $100,000 of your $1 million portfolio in cash sound unreasonable? Given where valuations are today, I don't think so.

Everybody is expecting at least another 10%+ correction at some point. Therefore, if it happens, saving $10,000 in losses by keeping $100,000 in cash should be comforting.

If you were to invest the entire $100,000 during the correction, then your portfolio would get an extra boost from such an investment if the S&P 500 eventually recovers.

However, if the S&P 500 goes up another 10% while you're holding 10% of your portfolio in cash, then buying during the correction and seeing a rebound back to 0% would be close to a wash.

Below is a chart from Putnam Investments that shows the historical duration and performances of bull markets and bear markets. What jumps out immediately is that our current bull market still has a lot of upside if it were to replicate the bull market of the 1990s.

Cash Buys You Time To Wait: Investing In Artificial Intelligence

You're certainly welcome to raise a lot more cash in your portfolio if you think a bear market is coming. In one 2020 CNBC survey, it found the average investor held roughly 23% of their portfolio in cash and cash equivalents.

The reality is, nobody knows when the next correction will happen. At the same time, we know there are always investment opportunities every day.

For example, I'm currently on the way to investing $500,000 in artificial intelligence companies. We are at the beginning of the AI revolution, and I don't want my kids asking me in 20 years why I didn't invest in artificial intelligence today.

Sure, valuations are lofty, but the investment in AI is accelerating according to the latest results from AI firms Nvidia and Databracks. I'm willing to invest 10% of my investable capital in AI because I have a lot of cash.

The easiest way for anybody to invest in private AI companies is through the Fundrise's venture capital product. It is an open-ended product with only a $10 minimum and much lower fees than traditional venture capital funds.

When it comes to measuring investment risk, calculate your potential loss and compare it to your remaining cash. If your remaining cash is 5X or more your potential loss, you will likely have the confidence to invest.

More Cash Gives You More Courage To Do A Lot Of Things

Besides cash giving you more courage to invest in risk assets, having more cash also gives you more courage to make a change in your occupation, start a family, be more giving, and so much more.

Feeling financially secure is wonderful. And if you find yourself waiting too long for a correction, then you can always use the cash to pay down debt if any.

In conclusion, I say it's worthwhile to aim for the following goals:

- Regularly earn high-enough investment returns to regularly pay for your desired living expenses

- Earn enough passive income to pay for your desired living expenses

- Have 5% – 10% of your investable capital in cash so you always have the ability to take advantage of investment opportunities that occur every year

- Have at least six months worth of living expenses in cash or cash equivalents so you never have to sell down your investments at inopportune times

Achieve all four financial goals and I dare say you will have achieved the ultimate level of financial freedom. No longer will you worry much about your day-to-day financial needs. People won't stress you out as much either.

Having a lot of cash is an integral part of your financial well-being. Embrace your cash to the fullest!

Invest In Private Growth Companies

Today, my liquid courage propels me to invest in private AI companies through private funds. Companies are staying private for longer, as a result, more gains are accruing to private company investors. Finding the next Google or Apple before going public can be a life-changing investment.

Check out Fundrise venture. It lets you invests in:

- Artificial Intelligence & Machine Learning

- Modern Data Infrastructure

- Development Operations (DevOps)

- Financial Technology (FinTech)

- Real Estate & Property Technology (PropTech)

A sizable amount of the venture product is invested in artificial intelligence, which I'm extremely bullish about. In 20 years, I certainly don't want my kids wondering why I didn't invest in AI or work in AI!

The investment minimum is also only $10. Most venture capital funds have a $250,000+ minimum. I plan to invest $500,000 into private growth funds that invest in artificial intelligence over the next three years. Fundrise is a long-time sponsor of Financial Samurai.

Conversation With The CEO Of Fundrise On AI

Here's a conversation I had with Ben Miller, CEO of Fundrise. We talk about AI, private growth funds, and the future of venture capital. You can sign up for my podcast on Apple or Spotify.

Readers, how much liquid courage does cash provide you? How much cash do you think one should have at any moment? Are there examples where having cash gave you the confidence to invest in something you otherwise wouldn't?

Note: the other way to gain investing courage is to just hire a financial advisor or digital wealth advisor to manage your money. Once you farm out your investment responsibilities or at least a portion of it, you also transfer a lot of the emotion when it comes to investing. Liquid Courage is a Financial Samurai original post.

I agree with you that each persons ideal level of cash will be different. For me, I am good with 6 months in cash and investing the rest. I recently threw in $10k at the market highs during the beginning of the month because I have no need for the money anytime soon. I tend to dollar cost average and invest lump sums as they arrive, since a 30% run up just to wait for a 10-20% correction makes little sense. However, sometimes, I will get in just after the run up.

Many new clients I talked to as an advisor at my previous financial firm had been in all or excess cash for 5-10 years, waiting for the inevitable drop, missing out on the gains in the interim. While if used as a safety buffer, cash can make sense, holding large amounts, especially in inflationary periods, is harmful.

I keep about a year’s living expenses in cash. I don’t consider it touchable except for dire emergencies. The vast majority of my money is tied up in real estate. The main reason I don’t keep much of my investable assets in cash is just doesn’t make me anything. But I will admit that during those in between investment times that I do hold significant amounts of cash, the feeling of having unlimited options is almost euphoric.

I HEAR you about liquid courage coming from cash! That definitely played into our decision to sell our condo instead of renting it out. We were clearly at a top in the market (maybe not the very top but prices had appreciated in our complex 30% from 2020!). Selling would give us a six-figure stash that we could use as a down payment for a bigger rental, to buy a smaller rental for cash, to invest in the market or just to hold and give us more courage to take chances with our consulting business. The options from a cash stash are very freeing.

My liquid courage comes from the belief that I can always find a way to make money. Our stock investments are treated as liquid cash. Haven’t had to tap into it yet. It would be very unlikely for me to be laid off from the career I’ve had for 19 years and if that did happen, my husband and I have contacts to get work to make ends meet. We’ve both done so many different hustles by now that there’s no way we would ever go hungry and will always have a place to live since the house is paid off.

Hi Financial Samurai

All excellent points, holding cash has so many advantages. It enables us to take risks and also to be patient which is extremely important, in particular for buy and hold investors.

Cheers

Hi Sam-

Been thinking about this a lot lately with

30% market return in 2019

20% in 2020 and now 2021. I believe there’s very limited upside over the next 1-2 years.

I’m 32 and my wife and I have $2.5M NW and $2.3M is in equities. I read your blog all the time and know diversification is so important but always just think if I’m willing to hold stocks for 20+ years; I’ll be fine. Lately though, I’m getting uncomfortable with this allocation. I also may buy a house in 2023 which would likely require a $300-$500k down payment so thinking about gearing up for that. I feel so incredibly privileged but it consumes me thinking about this. My NW was $1M about 2 years ago so I’m just getting comfortable with this.

I have always been a bit conservative in my cash position due to occasional larger expenditures/purchases for rental property portion of my portfolio. Has anyone used or researched the margin lending aspect available through Interactive Brokers as an alternative to a large cash position? While the rates are currently low, they are variable, so it doesn’t leave you with the same level of comfort that cash may. But, my current assumption is that it could be used in similar fashion to a HELOC for short-term expenses. Additionally, depending on your risk tolerance, it could potentially give you liquidity to buy into a market dip (kind of doubling down), or maybe used for a rate arbitrage either for dividend stocks or Fundrise investments. Just curious if I’m missing some obvious risks or roadblocks to looking for a bit more cash position efficiency.

Very interesting article… When I started my career, I always felt the need to have a healthy amount of cash… I am now in my mid-30s with nearly 4M in equities and a small portion in private real estate deals and crypto… I have less than $5K in cash at the moment as I am saving about 25K a month after taxes that I use for expenses and to continue DCA into risk assets… Unless I had a much more bearish view on the market, I don’t see the need to hold that much cash. If something comes up unexpected, my entire portfolio is essentially liquid.

Sounds good to me. Do you recall how much you had invested in the stock market during the global financial crisis?

I would say so long as you’re making six figures a year, and can keep your job during a downturn, going all in is fine in your mid 30s.

How do calculate “investable assets” if someone has a large chunk in real estate? For example, someone has $5M in real assets and $3M in liabilities, plus let’s say, $2M in index funds. Based on your rule, would you advise them to hold $350k in cash, or only $100k?

$2 million real estate equity + $2M in index funds = $4million X 5% = $200K in cash.

If you are extremely leveraged, wouldn’t you want a big pile of cash to help you sleep? I’m just thinking if you ONLY have $5M in real estate and $5M in mortgage, you wouldn’t want to keep $0*5% = $0 !!!

Sorry to harp on this, but you advocate for real estate investment all the time on your blog, and just want to know how you’d plan accordingly.

Oh, no worries about harping at all. Are you feeling overly exposed to risk assets? If you are stressed, then feel free to raise more cash! I’m not you and you’re not me. It’s important to focus on what you’re comfortable with.

The last bullet point in my assumptions is:

* Differentiate between cash in your investment portfolio and cash used to pay for life’s emergencies

I hope you do not have $0 equity with $5 million in real estate exposure. How much cash do you think you’d need? I’d love to learn more about your story.

Thanks

I’m a lot closer to the original hypothetical I outlined, but if there were some catastrophe like 2008, then maybe the latter hypothetical isn’t so crazy.

If a bubble is bursting, you don’t want your cash reserves to be a percent of your equity so that they are also declining! I’m just thinking your formula could use a retweak, that’s all.

FWIW our cash reserves are about 2% of total assets and 4.5% of net worth.

Sure. So what do you recommend and how much cash do you have?

For most people, cash is always being replenished.

I have no recommendations…I’m completely winging it. That’s why I come here!

Come to think of it, I guess my advice for people with stock AND real estate is to keep 4-6 months of expenses in cash for all properties, and then do the 5% for your liquid assets like stocks and bonds.

It’s fascinating to read the anxiety some people have from their comments.

It looks like most people are just looking for approval for a decision they already decided.

Sam, in the past week, I was thinking about BABA as well! Do you plan to hold for a few years?

At current levels, I see 20% downside and 80% upside over the next three years.

In three years, we can look back to this post about liquid courage and laugh at my poor investment decision. Or, we can dissect this case study and recognize that investing money takes guts.

I’m willing to take this risk because I have a lot more cash behind. If Chinese tech stocks do go down another 20%, I will likely double my position to $100,000.

I dream of a day where I can have a lot of cash sitting in my wallet and I can just do something very risky that has a 1% chance of 100x returns with a 99% chance of losing everything and not care if I do end up losing that investment.

It is taking a very long time and I don’t think I will ever get there but having cash is a good means to get there.

You can always invest 1% of your portfolio into a potential multi-bagger unicorn. Like you said. You never know.

Here’s what happened when I invested $3,000 in one stock back in 2000.

https://www.financialsamurai.com/fortune-hunting-money-making-opportunities-in-stock-market/

Sitting at roughly 8%, but some of it is in bond funds. I guess it all depends on your investment style, goals and objectives.

Just curious, where’d you get the “If your remaining cash is 5X or more your potential loss, you will likely have the confidence to invest”? I do a similar calculation for high risk investments.

It’s the level I’ve noticed where my liquid courage is high enough to make riskier investments. I have kept track of various levels over the past couple of decades.

About 8 years ago, I settled on portfolio allocaiton that includes 20% in cash. I realize most of you will think i’m nuts for keeping that much cash (and in fact I never mention this to friends or family ). When my other investments fall “out of band”, I re-balance using that cash. Makes it much easier (mentally) for me to “buy low” and to sleep at night. Sam has a much stronger stomach/ability for changing allocations based on reading the market than i do. In the past when I’ve tried that I invetiably end up buying high and selling low leading to predictably subpar returns. As a somewhat recent example, allocation strategy caused me to buy VBR (small cap fund) about a year ago. I never would’ve done that if left to my own predictions.

If you’ve got a system that works, stick with the system I say.

The biggest battle is getting the appropriate amount of capital invested.

I bought S&P 500 and Dow Jones IA structured notes with my entire severance payment back in June 2012 because I was bullish on the market, but I was afraid of losing any money since I left my day job.

Although I had to give up some of the dividends for the 20% downside Protection, it gave me enough courage to invest it all.

Related: https://www.financialsamurai.com/understanding-structured-derivative-products-cdsnote-as-an-investment/

I love your contrarian bet on Chinese stocks. I don’t want to be on the other side of the Chinese government so I’m not willing to risk my money but I definitely see the potential if your correct.

Time will tell if things work out with Chinese tech here. And if it doesn’t, I will only have myself to blame!

I love the markets in this way. There’s always two sides of the trade where one believes and one doesn’t believe.

I just like to put my money where my mouth is. Otherwise, there’s really no point jibber jabbering about investments.

We don’t keep much cash around at all. Currently, we only have about 2% of our net worth in liquid cash. And that’s because Mrs. RB40 plans to take a long unpaid LOA next year.

Normally, I keep my liquid courage in bond funds. I can sell those and move to stock when the market is down.

Is cash better than bond funds?

I suppose it depends whether you believe interest rates will rise. If they do, those bond funds will take a hit unless they’re a specifically short term fund

Excited your wife is finally taking a year off!

Cash is different from bonds in the sense that you don’t have to think about bond risk or tax implications as much.

Hmm, I think I currently have closer to ~9% liquid currently. With today’s crypto crash and everything’s that going on, this article’s got me panicking a bit.

I’ve actually been toying with the idea last year and this year to have around ~20% liquid. Was wondering if there was a derivation to where the 5% figure came from, and if it’s different depending on net worth?

For example, maybe save the ceiling of 10%, or 6 months of expenses (i.e. if 10% isn’t enough to cover 6 months of expenses, should save a bit more)?

Great article, as always.

One point on the Bull vs Bear market chart (which is very interesting):

Doesn’t it make a big difference whether you include the 5-month, 16% “Bear Market” in 2012? If you just ran the Bull Market from 2009 to 2021, that would be bigger than the 1990s run:

(1.94) x (0.86) x (4.02) = 6.70 –> +570%, i.e., bigger and longer than the Internet Bubble

Still, your main point, which is that bull market runs are hard to predict is well taken. But it’s worth noting that the chart would look less sanguine if this blip were computed in a different way.

Yes, it would make the overall results different for sure. I was thinking the same thing.

But it is what it is. If the chart took out the -15% drop in 1990, the 1990s bull market would look even bigger as well.

Like mini earthquakes to help relieve the pressure and prevent a big one. Resetting a little is good.

Yes, good point re: the 1990s. The Bull Market / Bear Market paradigms are important, but also hard to track.

In any case, I like the main notion of the article, which is to stay mostly invested but keep some cash for further investments.

Over the years, I’ve found that when things are uncertain (i.e., I have a view on the markets, but I’m not 100% sure), it’s best to do a mixed strategy. Invest some and keep some in reserves. Or sell some and keep some of the investment. The partial strategy is good for psychology and lets you make a move without going all in.

I like how you’ve articulated and quantified that notion here in the article. Onward!

Cash is truly king. I fell victim to lack of on hand cash not all that long ago…

I was saving to buy a new house so I had to keep my money focused on that. I was also approached with a very limited time opportunity, which required some quick decisions. The long story short was that I had less than 2 hours to decide to make a bet on a specific company and purchase some restricted shares and warrants. There was a relatively reasonable buy in, but the cash had to be moved quick – cash needed to be in for closing that day. I had to look at my funds and with the ultimate goal of buying a house, I had to make a choice. Focus on the house, or make a gamble on the success of this opportunity. In the end I decided that the house was more important so I decided to not touch the housing funds. Instead I tapped into the little side emergency fund that I was holding.

The good news is the investment paid off, and I made a huge profit of a couple million. I also bought a house with the housing fund a couple months later, win-win. The other news is, a friend of mine decided to make a different move and use his housing fund instead. His investment paid off significantly better. He made over $100M on the deal, and is now living abroad on easy street. He also decided he no longer needs a full time house, and is just renting different places around the world as he travels. He is also buying a series of rental properties to utilize when in the states.

While I’m very happy with the returns on my investment, I can’t help to think If I only was carrying more cash on hand…

I suppose at some point everyone feels that way, when looking back with a woulda/coulda/shoulda mentality. One thing for sure, I’m focusing on carrying more “liquid courage” going forward. You never know when you will get the next phone call, and cash will need to be deployed quickly.

I would think 5% in cash seems about right, and will likely be my target going forward.

Nice to see you in the crypto game finally. Hut8 stock has also been crushing it.

If by “crushing it,” you mean setting up the suckers to get flattened in this obvious pump and dump, then it is indeed soon to crush the suckers.

Only recently I realized the classic 70/30 split was wrong, and the appropriate asset allocation is very close to what you said above: keep 2 years worth of living expenses in cash, the rest in stocks. If your spouse is a dentist, then you can even reduce the 2 years to 6 months, and never pay down the mortgage. This is especially true for people who want to stay invested for 20-30 years before they retire.

This realization came during the 2020 COVID downturn a hedge fund return 4000% and the fund manager boasted that their clients are well protected. I realized their clients are protected only if they need the cash at that moment. If they don’t need the cash at that moment, they’d do just as well by not selling. (unless you cash out the 4000% gain and buy the market at the bottom, but I doubt anyone who had the courage or timing)

Agreed, my husband has a very secure government job and hence freed me to be able to go all in on the correction back in early 2020 with equities. Having a dependable spouse with income and benefits is an important factor to consider when weighing asset allocation and risk exposure. I was also working but my company didn’t make it through COVID and therefore without him, I would’ve kept a much higher cash buffer for our family.

What are your thoughts on holding precious metals in place if cash to beat out inflation and retain purchasing power?

I don’t think Sam ventures into alternative assets besides real estate. I don’t see safety in cash when $3.5 trillion of a spending bill is about to be passed, on top of already hot inflation. The 1970s are my guide for how fast inflation can get away from people. Personally I think real assets are underrated now, but you have to ensure they’re liquid enough if you are using them as savings

Correct. Im not a fan of precious metals except for in the watches I own. I’d rather own real estate, which inflates with inflation and generates higher rents with inflation.

Sitting at 16% of Networth in cash. Given my current expenses, I’ve got 3 solid years of cash if needed. If I cut back expenses, the cash would probably last 5 or more years if needed. Some feel this is too much on the sideline, but for me, I sleep well at night knowing that if it all came down to hell in a handbag I’d be able to weather it.

I like that term “liquid courage” better than the usual term “dry powder”. Sometimes when things are all falling, it can be tough to rotate from one investment into another even when it makes sense to do so. Having the cash already set aside helps clear that mental hurdle.

I peg the amount of cash I hold to the amount of time I can live off the cash (and other ultra-conservative investments), not a percentage of my portfolio. So if my essential expenses are say $80k/yr., I would target something like $80k in cash during normal times and $240k+ during periods when I feel markets are overpriced (like now). That said, I don’t let my cash stash exceed 10% of my portfolio since I plan to stay aggressively invested. I try not to “buy the dip” (time the market) and would prefer to strictly adhere to dollor cost averaging but I will admit, my actual buy behavior sometimes speaks otherwise.

Sounds like a plan. And so long as you have a plan for what to do, that’s the most important thing.

Couldn’t agree more! I’ve been sitting on 10% cash and at times a tad more, since my accidental retirement. To me it just made more sense to hold a lot of cash that I could deploy easily over bonds.

Everyone bashes cash – especially with our short term inflation. But cash gives you flexibility.

Cash is king. Cash is freedom. I love my F-you cash money!

Hah, good! Sounds like you really love your cash. It does feel great to have so much security.