This post will look in depth at the average net worth by age for the upper middle class. The upper middle class, aka the mass affluent, is loosely defined as individuals with a net worth or investable assets between $500,000 to $2 million. Investable assets means money outside of your primary residence, which is considered “trapped” and unproductive.

The upper middle class is also sometimes referred to as the aspirational class or HENRYs. HENRY stands for High Earners Not Rich Yet. Eventually, with the right savings and investing habits, HENRYs will build large amounts of wealth. They just need to be patient.

Some also define upper middle class as those who are college educated with incomes in the top 15%. A top 15% income is roughly $140,000 or greater for households or $80,000 or greater for individuals in 2025. For reference, the median household income is now about $80,000.

The upper middle class is an aspirational class that many aspire to achieve. With enough hard work, determination, and a long enough life, many of us can achieve upper middle class status. To folks, having status is even more important than money.

The upper middle class didn’t inherit their money. They mostly earned it through hard work. On the other hand, getting rich with a net worth of above $10 million often takes a tremendous amount of luck.

The upper middle class invests in real estate

If you want to boost your wealth beyond the middle class, invest in real estate. The combination of property price appreciation and rental income growth is a powerful wealth creator. Real estate enabled me to retire at 34 due to a portfolio of rental properties that generate over $120,000 a year. You can invest 100% passively in real estate through Fundrise, with an investment minimum of only $10. I’ve personally invested over $500,000 in Fundrise so far. I've met and talked to the CEO multiple times over the years.

The Middle Class And Upper Middle Class Are Different

The middle class is different from the upper middle class. Middle class is defined as those earning between 67% and 200% of the U.S. median household income. The Pew Research Center defines middle-class households as those .1 That’s between $42,330 and $126,358, using the U.S. Census Bureau’s 2020 median income of all households. The income is at least 10% higher in 2025.

We can also define middle class in terms of net worth. According to the U.S. Census data, the average net worth for U.S. households in 2022 was about $1.06 million. The median net worth is about $192,900 according to the latest Consumer Finance Survey. In other words, wealth is concentrated at the top.

We all aspire to be upper middle class or rich. However, statistically, it's not possible. Therefore, it's worth discovering other ways we can feel rich without actually being rich.

The Average Net Worth By Age

To calculate the average net worth for the upper middle class, let's first look at the average net worth of all Americans. This data comes from the US Federal Reserve.

- The average net worth for Americans younger than 35: $73,500

- The average net worth for Americans between 35 – 44: $299,200

- The average net worth for Americans between 45 – 54: $542,700

- The average net worth for Americans between 55 – 64: $843,800

- The average net worth for Americans between 65 – 74: $690,900

- The average net worth for Americans 75 or more: $528,100

- The average net worth figures are quite impressive, and are likely 20% higher in 2025.

The middle class is a fine class. However, let us aspire to get into the upper middle class in our lifetime. After all, we'd all much rather achieve financial freedom sooner, rather than later.

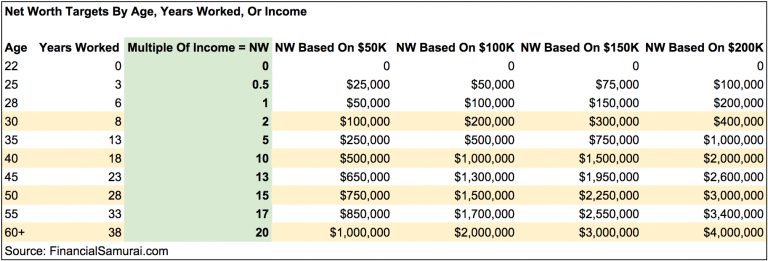

Based on the average net worth figures above, the upper middle class net worth by age can simply be 50 percent or greater.

Key takeaways from average net worth by age data:

1) Volatile wealth. There's a huge 37% decline in the average American's net worth for the same period (55-64 to 75+), which may signify that the average American isn't as adept in making their money last into retirement. They are perhaps spending down their principal instead of investing their net worth in stable, income producing assets.

2) The average American starting out is struggling. For the first 35 years, the average American is struggling to make ends meet. They're probably in school, paying off debt, and saving for a rainy day. There's probably a lot of angst about never being able to get financially ahead in such a competitive and expensive world.

3) The average American does well later in life. The average net worth by age in America is actually quite healthy, contrary to popular belief that most Americans don't save enough for retirement. Clearly, extremely wealthy individuals will skew the averages higher. But, the biggest surprise is the $843,800 average net worth figure for the typical American ages 55-64. That's almost like saying everybody who is between the age of 55-64 is a millionaire!

The More Money You Have, The Better

This data should stand out as much as the incredible study which says that 100% of Americans who make more than $500,000 a year are happy. But the media doesn't want to report on positive financial findings because poverty and suffering garners more traffic and advertising dollars.

For the average American, their financial lives get so much better later on in life. Perhaps this is why older people are more relaxed, less insecure, and almost all agree with my own average net worth and 401k charts.

Given inflation is elevated, more people are feeling financial constraint as their incomes don't keep up. Many households live in expensive cities with children. As a result, even multiple six-figure incomes may not feel like enough to feel secure. In their minds, only generational wealth will be able to alleviate the stress and anxiety.

Median Net Worth By Age

I can hear a cacophony of complaints about how absurd the data is by the US Federal Reserve regarding the average net worth by age. Don't worry. I've already got a headache listening.

Averages tend to skew the numbers higher due to a concentration of very wealthy individuals. Therefore, let's take a look at the median and average net worth for Americans according to the Federal Reserve. If you truly want to be upper middle class, you need to have more than the average person.

Median net worth by age provides for potentially a more realistic picture of the “average” American. The sweet spot for net worth amount continues to be ages 55 – 64, right before the traditional retirement age of 65. Although, new research in 2024 says the traditional retirement age can be lowered to 55. Saving 10 years off your working life is huge!

The curve of the median net worth chart, if we were to graph it, looks the same as the average net worth chart. By the time the median American reaches 75+, s/he has spent down 35% of principal.

Social Security Is Important For The Median Person

Let's look on the bright side of things. If you still have $163,100 in median net worth by age 75+, you're probably going to turn out just fine, especially if you have long-term care insurance. Protect your family.

If we add on pensions or Social Security, is the retirement crisis really so bad? None of us have to live in expensive cities such as San Francisco, New York, Honolulu or Los Angeles during our non-working years either. We can hop on a bus to Iowa, Indiana, South Dakota, or Louisiana to allow our net worth to last longer.

For those of you who are really bearish about the financial health of the average American, or who feel upset because your net worth isn't in-line with the upper middle class net worth figures, here's a chart to justify your concerns. The chart below shows that the median US household has gone nowhere in the past 50 years!

Remember, when it comes to data, we can pretty much believe whatever we want to make ourselves feel better. We see what we want to see, in order to justify our actions.

Average Net Worth For The Upper Middle Class

Now that we've analyzed the data for all Americans with averages and medians, let's look at the average net worth for the upper middle class.

The above average person isn't drawing down capital to survive due to their creation of multiple income streams, smart asset allocation, discipline to consistently live within one's means, and the desire to leave money for loved ones and charities who are in dire need of funding. The Financial Samurai ideology is to leave the world better off than when we first entered.

Finally, the financially savvy person understands the estate tax (death tax) doesn't kick in until assets are over $13.99 million for persons dying in 2025. That's pretty huge.

Therefore, every single person might as well shoot for accumulating up to $13.919 million per person to help other people. But the reality is, anything above $10 million is a top 1% net worth and rich, not upper middle class. After a few million dollars in net worth is considered closer to upper middle class.

Anything earned beyond such an amount should be spent with great enthusiasm while alive! You don't want to die with millions. If you do, that means you wasted a lot of time and energy while younger.

Be Careful Having Too Much House

One of the problems with the average American is that the value of their house dominates their net worth. The upper middle class (top 20% of Americans) have a net worth where their primary residence is worth less than 30% of their overall net worth.

The upper middle class follow my primary residence as a percentage of net worth guide. A primary home worth more than 30% of net worth is too concentrated.

Conversely, notice how a house takes up more than 60% of the average American's net worth. Therefore, the average net worth for the upper middle class should have a very diversified net worth.

How To Join The Upper Middle Class

If you want to join the upper middle class per your age group, I recommend the following:

1) Max out your 401k and/or IRA as soon as possible. Try and save an equal or greater amount in after-tax investments as well.

2) Think about the proper asset allocation in relation to personal risk. Your assets should be deployed in a way that aims to beat the risk-free rate of return by at least 2-3X. Stay diversified and never confuse brains with a bull market!

3) Voraciously read as much as possible about wealth management, investing, retirement, taxes, and other issues. Subscribe to the Financial Samurai newsletter and the Financial Samurai podcast on Apple or Spotify for free. Don't be afraid to seek professional financial help too.

4) Move to a part of the country where there is opportunity. Give yourself a chance to get financially lucky by coming to areas where there is robust employment and brain share. It used to take two months to cross the country. Now it only takes five hours by plane.

5) Buy a home that you can afford and own it for as long as possible. You'll wake up 20 years from now and thank yourself for having something to show for all your monthly payments. Forced savings through principal payments may sound rudimentary, but most people don't have enough discipline to save on a regular basis.

6) Read personal finance books such as my instant Wall Street Journal bestseller, Buy This, Not That: How To Spend Your Way To Wealth And Freedom. It's jam packed with information and strategies to help you build more wealth compared to the average person. The upper middle class are voracious readers.

More Upper Middle Class Wealth-Building Strategies

Here are more recommendations if you want to join the mass affluent or upper middle class.

7) Build as large of a taxable investment portfolio as possible. Once you've maxed out your 401(k), 403(b), IRA and other tax-advantaged accounts, you must build a tappable taxable investment portfolio. After all, it is your taxable investment portfolio that will generate the passive investment income necessary for you to live free or retire earlier.

8) Don't be afraid to seek professional financial help if you're lost. Put it this way. The more lost you are, the more bang for your buck you get hiring someone to give you advice or manage your money.

9) Make sure you are properly insured: health, life, auto, house, and umbrella policy. Any number of bad things can happen that can easily wipe away your net worth.

10) Work and invest for as long as possible. “Time in the market is more important than timing the market,” as the saying goes. Half the battle is just surviving through all the ups and downs, which is why consistent dollar cost averaging and refining of work skills is important.

11) Once you've properly diversified your wealth, things start getting a little messy. Track your finances through Excel, or a free financial tool by Empower in order to optimize your finances and make sure there aren't any leakages. It's hard to improve what you don't measure.

12) Think positively. If you want to join the upper middle class, believe you deserve to be wealthy. Don't let the government or naysayers keep you down. Use constant failures as learning points.

Build Upper Class Wealth Through Real Estate & Venture Capital

To achieve an upper middle class net worth, I highly recommend investing in real estate in addition to stocks. If you look at the average net worth by age for the upper middle class, real estate is a core component to the net worth composition.

Real estate is a tangible asset that provides utility and a steady stream of income if you own rental properties. Unlike the stock market's volatility, real estate tends to be more stable and often delivers higher income yields. Over time, thanks to rent appreciation, property value growth, and mortgage paydown, real estate can help you build significant wealth.

To invest in private real estate passively, check out Fundrise, my preferred real estate platform. Fundrise has been around since 2012 and now manages over $3.5 billion for over 380,000 investors. For most people, investing in a diversified real estate fund is the simplest way to get exposure.

Investing In Private Growth Companies As Well

For those interested in long-term innovation, Fundrise Venture also provides access to private AI companies like OpenAI, Anthropic, Anduril, and Databricks. AI is reshaping productivity and employment at a massive scale, and I want to ensure my family’s portfolio has sufficient exposure to this transformation.

With a minimum investment of just $10, it’s easy to dollar-cost average into Fundrise, as I’ve done for years. As I grow older and wealthier, I no longer have the patience to deal with maintenance or tenant issues. Further, I want to invest in private AI companies so my children don't ask me 20 years from now why I didn't near the beginning.

Real Estate Enabled Me To Retire Early At Age 34

Due to my real estate investments since 2003, I've been able to handily achieve a net worth far above the average net worth by age for the upper middle class. Today, real estate income accounts for about 50% of my current $370,000 a year in passive and semi-passive income.

The key to building great wealth is through aggressive saving and savvy investments. Real estate is a proven wealth-builder long term as it forces you to pay down debt and own for the long-term.

Free Financial Analysis Offer From Empower

If you have over $100,000 in investable assets—whether in savings, taxable accounts, 401(k)s, or IRAs—you can get a free financial check-up from an Empower financial professional by signing up here. It’s a no-obligation way to have a seasoned expert, who builds and analyzes portfolios for a living, review your finances.

A fresh set of eyes could uncover hidden fees, inefficient allocations, or opportunities to optimize—giving you greater clarity and confidence in your financial plan.

I’ve been using Empower’s free financial tools and speaking with their financial professionals since 2012. From 2013 to 2015, I also consulted part-time at their offices when they were still called Personal Capital. As both a longtime user and affiliate partner, I’m genuinely pleased with the value they’ve consistently delivered over the years.

The statement is provided to you by Financial Samurai (“Promoter”) who has entered into a written referral agreement with Empower Advisory Group, LLC (“EAG”). Click here to learn more.

About Financial Samurai

FinancialSamurai.com was started in 2009. It is one of the most trusted personal finance sites today with over 500,000organic pageviews a month. Financial Samurai has been featured in top publications such as the LA Times, The Chicago Tribune, and Bloomberg.

Join 70,000+ others and sign up for my free weekly newsletter here. The Average Net Worth By Age for The Upper Middle Class is a FS original post.

Are pensions considered investable assets for these net worth calculations? If not they should. Retired military, police and teachers have a lot more wealth than it looks on the surface.

A pension is a valuable asset. Here’s how to calculate the value of your pension.

Interesting article. Does your net worth include homes? I see most places 5.8 m is 1% and last year was 5.4m. I think what might push it up is the high concentration. At the top .10%.

Fortune stared the above and so did wiki. Why is yours so high?

Depends on the source. Check it out: https://www.financialsamurai.com/obtaining-a-top-1-net-worth-easier-than-ever/

Love your articles! I am 45, have $450k equity in house, $525k pre tax savings, $150 post tax savings, $400k value in equity in my business I hope to sell by the time I am 50. We save $42k per year towards future retirement and save $25 in cash we keep in brokerage saving account we aren’t 5.25% intrastate in. My question is can we partially retire at 50? My wife and I plan to earn a living but at a reduced income. We won’t need to pull money from savings but plan to let the $1.4m in investment grown between 50 and 67 when we plan to take distributions. At a conservative growth rate we should have at least $3m by the time we reach 67. Is this feast?

A conservative growth rate is about 6%. Some financial planners use this figure when they work with their clients. 2022 was a year both stocks and bond did poorly. Otherwise, a split of 65% stocks and 35% bonds should do well in a long run. You should definitely put your pre-tax savings in this. Also you could try to move some of the pre-tax savings into Roth and pre-pay the taxes, but it makes no sense to overdo it. While a full retirement @50 is too risky, a partial retirement may work, but it depends on how much work you are willing to do. Potential medical costs could ruin you finance if you don’t plan it well. So you should at least make enough to cover the costs your health insurance + some money for any potential major fix-up costs for your residence. Equity in your primary home should not be counted unless you would relocate. Also the equity in your biz could fluctuate greatly. It all depends on how much a buyer is willing to pay.

What do you think about investment in vacation homes? I bought one in 1999 for $490K and today it is paid off and $3.2Mworth

Congrats! Where is it located?

In general, vacation homes are a bad investment. Underutilization and first properties to decline during a downturn.

I’d love to hear more details about your home. Thx

As an under 35 man who fits in the average networth, you should also mention crypto as a way to diversify. I’ve made quite a bit of my money off it and I’d recommend others put a small 1-5% of their money into it as a speculative asset.

As younger retirees (50’s) we are very pleased and grateful for our financial position of several million, but, most importantly, we are pleased that we, and our kids lived the lives we wanted to live along the way, with homes on the Southern CA Coast, as well as via other lifestyle choices we made when we were young. We knew what we wanted and didn’t want at a fairly young age.

Everyone has different dreams, so I can’t say enough about how important it is to make good financial decisions at an early age, with a sustainable long-term plan, so you can live the life you really want to live as early as possible.

I’m 60, been a high school teacher for 35 years, almost always worked a second job too. I have a net worth of 8-million and I plan on working 4-5 more years because I love my job. So I’ll probably be worth more when I retire in a few years. I’m single, love working and helping others. I deliberately and methodically saved in my Roth, 403b, and pension accounts. I’ve saved and bought a couple of so-so homes and paid them off — nothin fancy.

It just didn’t seem that hard to become upper-middle class or rich for that matter. Just get educated (doesn’t even need to be a great university degree/major) and goto work for 35 years +, save tax deferred (don’t even need to make great returns on your invested savings,) try to stay healthy and eat well. Buy a little real estate, nothing fancy. Don’t tell people you are a millionaire, dress in Walmart clothes, drive an old car, mow your own lawn and paint your own house. Success starts with a 50-60 hour work week, for a few decades. It worked for me.

Love it! The power of consistency and time. Having that low operating cost is also great.

Any fun plans on how to spend the $8+ million?

land is the basis for all wealth

I agree to a point. Too bad there is so much property tax to the point where after paying a certain amount, it’s unbearable.

Would love to hear how a 60 year old HS teacher amassed 8 mil in net worth. Without an inheritance, that’s a nearly impossible number. Borderline not believable.

What is equally important to accumulation of assets is the fact of how one spends down one’s nest egg. Many, if not more assets are lost in the spending (sourcing of income, taxes) as in the build-up to retirement!

“There’s a huge 37% decline in the average American’s net worth for the same period (55-64 to 75+), which may signify that the average American isn’t as adept in making their money last into retirement.”

I don’t think this signifies anything about their adeptness. Not everyone’s goal is to leave a huge inheritance after they die. Maybe that’s the “Financial Samurai Way”, but not everyone has to have the same goals. Not everyone has kids (or if they do, then perhaps leaving some inheritance may be a nice-to-have but not a priority), and most people feel good enough about leaving what they do have left to charity without stressing that it’s not 100% of the principal they retired with.

In fact, within the FIRE movement it’s much more common for people to actually desire to draw down principal rather than keep their principal perfectly intact by the time they die. It would be nice if my investments do better than I expected so I can leave a large amount to charity, but I’m not going to go out of my way and work several more years just to ensure I never draw down principal. If I outlive my money and am able to leave at least some for charity when I die, I consider that a win. If I never draw down any principal in retirement, I would actually consider that a personal failure in planning too conservatively and working way longer than I needed to.

Also, I agree with some of the comments the first chart should be redone using the median. You have a section below where you talk about the median, but you never made the chart or showed the numbers. Drawing conclusions about how ok Americans in general are doing based on averages rather than medians is pretty meaningless.

Yep, see the book, “Die with Zero” for a good explanation (and solid defense) of spending down your money before you die.

The only problem with the book is the author is worth over $150 million. So it’s much easier to tell people to spend all the money when he himself will likely not be able to.

I just turned 27 and am building my second house on a lake. I have over $130,000 in real property paid off except $9,000, about $480,000 in my businesses liquidity and $15,000+ in tools I also have precious metal investments. I am going to start renting my second house out and eventually buy large apartment complexes. I’m doing well but I will do better just getting started.

Congrats! Keep on prudently going!

Upper middle class is is lifestyle. Umc people usually have college degrees, high incomes (low-mid 6 figures), and a great deal of autonomy in their work. It has nothing to do with being responsible or saving in a 401k. It depends mostly on your intelligence and the type of career you’re in. Working a blue collar job and saving money for 30 years doesn’t make you upper middle class. It just makes you a middle or working class person with money. It’s not the same thing.

“It depends mostly on your intelligence and the type of career your in.”

That’s the dumbest comment I’ve heard on here…

There’s plenty of blue collar workers that have high paying jobs, and who also have education. Yet they choose to work outside the confines of an office and house/community they cannot afford.

Your describing what’s called being a snob and wannabe elite Nothing cool or classy about either. In fact, I’m m glad you made that comment, because it’s a reflection of those with your mentality living in a delusion.

Your sense of superiority is amusing.

I do believe there is a difference between having a high income and having a lot of assets. I do believe you need to save and invest a high-income to become wealthy or possibly rich — especially if one starts with little to nothing.Earning a lot of money is one thing, but keeping and growing that money via savings and investment is another — one has to save and invest for retirement.

I know people who have nice homes and cars who don’t save and they are only a few paychecks away from insolvency. Upper middle class is everything you said in your introductory sentences, but it is so much more — saving, investing to grow one’s wealth. The old adage, “It’s not how much you earn, it’s how much you keep, grow and invest,” really is true when striving to move up the American class system.

“But, the biggest surprise is the $843,800 average net worth figure for the typical American ages 55-64. That’s almost like saying everybody who is between the age of 55-64 is a millionaire!”

It’s not though. The median is likely incredibly far below $843,800, because we know distributions of things like income, net worth, etc., are very positively skewed. That is, you could have one person with a net worth of $50MM and 49 people with a net worth of $0 and still end up with an average net worth of $1MM. I wouldn’t be surprised if it’s only 10-20% of people in that age bracket that have a net worth over $1MM.

K-Man, you’re correct. Why would anyone use the average (the “mean”)? Every other website uses the median or at least shows both the mean and median. The way this is shown is completely inaccurate.

Curious, why strive to be median when you can strive to be average?

Don’t be average but the median is a better reference point where you are. Percentiles would be better still.v

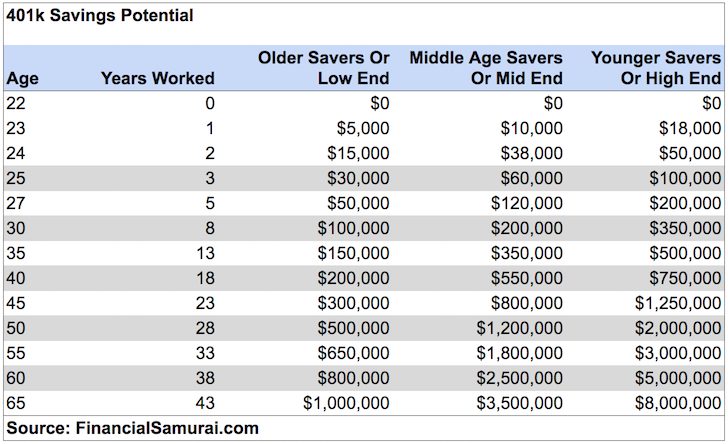

How do arrive at $596,500 for pretax savings at age 45 from the 401k table above (i.e., how mid end savings of $800,000 got converted to $596,500 for age 45)?

And, do you have similar data for couples where one spouse is a homemaker?

My IRA and 401 (tax deferred) accounts are about $2,000,000 with an additional money in taxable accounts. Actually, the tax deferred accounts (while this is their listed value) are worth less, as I owe taxes to the IRS as I withdraw the required minimum distribution. How do I account for this when computing net worth?

I went back and was reading your original charts. Each of your charts starts out with the “average person” or “above average person” or the “average American”.

How do you factor in married couples. In the above average category what is the case? Is it double the number we see or is it one half of the number we see.

Good question.

Check this out: https://www.financialsamurai.com/the-average-net-worth-for-the-above-average-married-couple/

I think these numbers are high for above average in the 30’s but low in the 50’s. My wife and I are 31-34 and our combined net worth is $550k. I’d be surprised to see many our age have a net worth that is much higher without inherited wealth. We have no debt (cars, mortgage, student loans) and are now saving $200k a year. I’ve done some projections and it’s crazy what we will end up with later in life. I think everyone’s real problem is the fact that they need to lease new cars, take expensive vacations and don’t enjoy saving. There is nothing better than watching your net worth increase every paycheck. Work hard, don’t have kids outside of marriage, and don’t get divorced. In my opinion these are the keys to success.

Hi Chad,

There’s more of us than you think. My wife and I (27-30 have) have a combined net worth of about 900K and we are both teachers. We started with nothing but I’ve heavily invested in real estate. I’m not sure that the early numbers are that far off.

Wow! That’s great!

I’d love to profile your story if you are willing to share. Please send me an email. I do want to ride profile about teachers.

Email sent!

So, I am nearly 70, single, and have an income of about $60K, but a net worth of about $2.5 million (thanks to compound interest).

Am I upper middle class or lower upper class in terms of net worth?

(Not that it really matters. I have far, far more than I need to live on and my goal is to give almost all of it away before I die, leaving enough for Long Term Care should I happen to need it and enough for the funeral. Still, it would be of curiosity to know.)

Hi John my name is Cheryl I found your comment very interesting on the site I wanna know how to do compound interest I’m very interested because I would love to have a good nest egg by the time I reach retirement can you please help me in the situation so I can make the right steps thanks

Thank you for the article and data. It would be nice to see the top 1% remove from the data to take out the extremes. But in the end the way I look at my work, earnings and savings is that I really only compete with myself. What do I need/want for my family and self. If you focus on what the neighbor has you become very jealous society. Have a market where individuals can succeed to their own desires and levels.

Good article, although it may be a bit technical for those just getting started.

It all boils down to hope: yes, you can get there! Just about everyone can become “mass affluent.” If you live like you’re never going to have two dimes to rub together, that’s where you’ll end up. Live like you can become well-off, and you’ll go that direction instead.

This isn’t just opinion; I’m doing it.

It would be good to develop a chart of net worth for people who don’t live in the expensive cities (nearly anything along the CA coast and some parts of the east coast. The upper middle / above average tend to live in big cities, earn more, have higher valued houses, and also face more expenses. Wouldn’t that skew even the median? You suggest that retirees move to North Dakota (weather is an issue). It can noted that for those no faint in heart, there are a number of semi-abandoned small towns in Kansas. Colorado looks great in a few spots, but I am digressing. In other words, regionally adjusted comparison – like the PPP (purchase power parity) used to make cross-country comparisons of per capita GDP – would be helpful.

You’re free to adjust the charts down to whatever makes you feel happy. But then, that’s kind of like moving the goal post to make scoring easier.

The federal tax code doesn’t tax less for those who live in SF where the median house costs $1.5M to give them a break. They’re argument is, who cares if your job is there, move if you want to save money on housing. It’s a free country.

I often find it’s programmers, lawyers, doctors, engineers, and other “professional” people of means who make these websites and financial blogs (which themselves often earn quite a bit for the writers.). about 50% of the working population makes less than 30k gross before taxes. I agree that living within ones means and investing is smart, even though we are likely looking at a nasty nasty bubble bursting coming up, it will no doubt recover long term, should the ecology of the planet not shit the bed.

However, one needs to have means first, and that is decidedly uncommon, the data makes that plainly clear. No how matter how much anyone of means, who’s often found said means by luck (yes the data suggests that as well), says that it’s all about gumption, grit, hard work, and go get’em bootstrap pulling, is selling you a myth. Why Because finding high paying work that allows for this kind of savings requires exactly that, luck. Studies show the poor tend to stay poor, and the affluent tend to stay affluent. Exceptions are just that, and using them to constantly suggest people can do better is misleading.

As you note, median is much more accurate….by quite a bit.

“It may also be surprising to learn how much of a person’s net worth is tied up in his or her home. If you exclude home equity from the net worth calculation, then the median net worth drops significantly across all age groups. For example, the median net worth for a person age 70 to 74 years drops to $31,823 from $181,078 when home equity is excluded.”

The costs of food and housing and education and health care and transportation and child care and taxes have been well-defined by organizations such as the Economic Policy Institute, which calculated that a U.S. family of three would require an average of about $48,000 a year to meet basic needs; and by the Working Poor Families Project, which estimates the income required for basic needs for a family of four at about $45,000. The median household income is $51,000.

The Official Poverty Threshold Should Be Much Higher

According to the Congressional Research Service (CRS), “The poverty line reflects a measure of economic need based on living standards that prevailed in the mid-1950s…It is not adjusted to reflect changes in needs associated with improved standards of living that have occurred over the decades since the measure was first developed. If the same basic methodology developed in the early 1960s was applied today, the poverty thresholds would be over three times higher than the current thresholds.”

The original poverty measures were (and still are) based largely on the food costs of the 1950s. But while food costs have doubled since 1978, housing has more than tripled, medical expenses are six times higher, and college tuition is eleven times higher. The Bureau of Labor Statistics and the Census Bureau have calculated that food, housing, health care, child care, transportation, taxes, and other household expenditures consume nearly the entire median household income.

CRS provides some balance, noting that the threshold should also be impacted by safety net programs: “For purposes of officially counting the poor, noncash benefits (such as the value of Medicare and Medicaid, public housing, or employer provided health care) and ‘near cash’ benefits (e.g., food stamps..) are not counted as income.”

But many American families near the median are not able to take advantage of safety net programs. Almost all, on the other hand, face the housing, health care, child care, and transportation expenses that point toward a higher threshold of poverty.

Very strange stuff. I have a net worth of over 2 million. How come I don’t feel upper middle class? I drive a 10 year old car, live in a 2000 square foot house and wonder if my cash flow will last for a possible 30 years????????

It’s probably because you’re comparing yourself to people who have more. But if you come up with a plan, and do an income and expense analysis, you’re probably going to be fine.

But $3 million is the new $1 million. That’s all thanks to inflation. So perhaps when you came at one more million dollars you’ll feel good.

See: https://www.financialsamurai.com/are-you-a-real-millionaire-3-million-new-1-million/

I believe part of what skews this too is the fact that people 55-64 are more likely to have their parents die, and thus, potentially inherit larger sums of money than they would have earned otherwise.

I came to US since I was 18. Study and work, open 2 failed restaurant but I was pretty aggressive investor. My net worth around $2.8M that real estate(no loan), 401K and cash. I still feel poor, live normal life, golf once awhile, shop for bargain, never fly business class, eat at home most the time.

lunacy

upper class 40%

upper midlle class 10%

middle class 10%

working class 5%

homeless 35% (like the upper class, homeless in urban areas on sidewalks and parks, upper class on their estates, have in common: impromptu: doing the bugaloo, charleston, one man waltz, , mazurka, etc gesticulating wildly towards the sky, soliloquy, giving speeches and believing you are the King of Spain, receive radio waves from extraterrestrial civilizations, etc

It’s a nice article. For upper middle income folks, the table says it is “average” rather than “median.” It would be interesting to see if the median is much different from the average.

Thank you for writing this article. I read it a few years back when I just started working after graduating college, and I was 22. I hardly had anything in my savings, my Roth was sitting at about $4000, and I had never even heard of a 401K.

My starting wage at my new job was rather low (for an Econ Bachelors at U of Mich) and I was very discouraged that I would be unable to match these numbers. My savings rate potential was low and I had to move to a new location and live alone (paying all my bills from the start). However, after a few months of living paycheck to paycheck, I saw my assets start to stabilize and grow. I took your advice to max out my Roth and pre-tax 401K match, then proceeded to hoard any money I didn’t spend into an online savings account – so maybe a 1% return every year pre-tax.

Looking back, I realized that these age ranges are good touchstones for where you should aim to be. Now that I am 25 years old, I am actually within the $70,000 asset range. Still paying off a $12,000 car loan, but I learned that is considered equalized if I just sold the car for full value (also took your advice to read up on investing/asset management). Now I have quite a bit of liquid cash to put into a Betterment account and wait out the fluctuations of the market.

Thank you again for helping someone just starting out after graduation!

WELL DONE Diana! And good job for not looking at these figures as impossibilities, but as achievable targets to keep you on a great financial path!

Give yourself 10 years of disciplined savings and investing, and you will be absolutely AMAZED by how much you will accumulate by age 35. With such wealth, you will have more options to do what you wish. We all burn out eventually and want to do something new. Please share the message!

Check out: Investment Strategies For Retirement Based On Modern Portfolio Theory

Best,

Sam