This post will look in depth at the average net worth by age for the upper middle class. The upper middle class, aka the mass affluent, is loosely defined as individuals with a net worth or investable assets between $500,000 to $2 million.

The upper middle class is also sometimes referred to as the aspirational class or HENRYs. HENRY stands for High Earners Not Rich Yet. Eventually, with the right savings and investing habits, HENRYs will build large amounts of wealth. They just need to be patient.

Some also define upper middle class as those who are college educated with incomes in the top 15%. A top 15% income is roughly $100,000 or greater for households or $65,000 or greater for individuals in 2023.

The upper middle class is an aspirational class that many aspire to achieve. With enough hard work, determination, and a long enough life, many of us can achieve upper middle class status. To folks, having status is even more important than money.

The upper middle class didn’t inherit their money. They mostly earned it through hard work. On the other hand, getting rich with a net worth of above $10 million often takes a tremendous amount of luck.

The Middle Class And Upper Middle Class Are Different

The middle class is different from the upper middle class. The middle class is defined as those earning between 67% and 200% of the U.S. median household income. The Pew Research Center defines middle-class households as those .1 That’s between $42,330 and $126,358, using the U.S. Census Bureau’s 2020 median income of all households.

We can also define middle class in terms of net worth. According to the U.S. Census data, the average net worth for U.S. households in 2022 is about $300,000. The median net worth is about $110,000 in 2024. In other words, wealth is concentrated at the top.

We all aspire to be upper middle class or rich. However, statistically, it's not possible. Therefore, it's worth discovering other ways we can feel rich without actually being rich.

The Average Net Worth By Age

To calculate the average net worth for the upper middle class, let's first look at the average net worth of all Americans. This data comes from the US Federal Reserve.

- The average net worth for Americans younger than 35: $73,500

- The average net worth for Americans between 35 – 44: $299,200

- The average net worth for Americans between 45 – 54: $542,700

- The average net worth for Americans between 55 – 64: $843,800

- The average net worth for Americans between 65 – 74: $690,900

- The average net worth for Americans 75 or more: $528,100

- The average net worth figures are quite impressive.

The middle class is a fine class. However, let us aspire to get into the upper middle class in our lifetime. After all, we'd all much rather achieve financial freedom sooner, rather than later.

Based on the average net worth figures above, the upper middle class net worth by age can simply be 50 percent or greater.

Key takeaways from average net worth by age data:

1) Volatile wealth. There's a huge 37% decline in the average American's net worth for the same period (55-64 to 75+), which may signify that the average American isn't as adept in making their money last into retirement. They are perhaps spending down their principal instead of investing their net worth in stable, income producing assets.

2) The average American starting out is struggling. For the first 35 years, the average American is struggling to make ends meet. They're probably in school, paying off debt, and saving for a rainy day. There's probably a lot of angst about never being able to get financially ahead in such a competitive and expensive world.

3) The average American does well later in life. The average net worth by age in America is actually quite healthy, contrary to popular belief that most Americans don't save enough for retirement. Clearly, extremely wealthy individuals will skew the averages higher. But, the biggest surprise is the $843,800 average net worth figure for the typical American ages 55-64. That's almost like saying everybody who is between the age of 55-64 is a millionaire!

The More Money You Have, The Better

This data should stand out as much as the incredible study which says that 100% of Americans who make more than $500,000 a year are happy. But the media doesn't want to report on positive financial findings because poverty and suffering garners more traffic and advertising dollars.

For the average American, their financial lives get so much better later on in life. Perhaps this is why older people are more relaxed, less insecure, and almost all agree with my own average net worth and 401k charts.

Given inflation is elevated, more people are feeling financial constraint as their incomes don't keep up. Many households live in expensive cities with children. As a result, even multiple six-figure incomes may not feel like enough to feel secure. In their minds, only generational wealth will be able to alleviate the stress and anxiety.

Median Net Worth By Age

I can hear a cacophony of complaints about how absurd the data is by the US Federal Reserve regarding the average net worth by age. Don't worry. I've already got a headache listening.

Averages tend to skew the numbers higher due to a concentration of very wealthy individuals. Therefore, let's take a look at the median and average net worth for Americans according to the Federal Reserve. If you truly want to be upper middle class, you need to have more than the average person.

Median net worth by age provides for potentially a more realistic picture of the “average” American. The sweet spot for net worth amount continues to be ages 55 – 64, right before the traditional retirement age of 65.

The curve of the median net worth chart, if we were to graph it, looks the same as the average net worth chart. By the time the median American reaches 75+, s/he has spent down 35% of principal.

Let's look on the bright side of things. If you still have $163,100 in median net worth by age 75+, you're probably going to turn out just fine, especially if you have long-term care insurance. Protect your family.

If we add on pensions or Social Security, is the retirement crisis really so bad? None of us have to live in expensive cities such as San Francisco, New York, Honolulu or Los Angeles during our non-working years either. We can hop on a bus to Iowa, Indiana, South Dakota, or Louisiana to allow our net worth to last longer.

For those of you who are really bearish about the financial health of the average American, or who feel upset because your net worth isn't in-line with the upper middle class net worth figures, here's a chart to justify your concerns. The chart below shows that the median US household has gone nowhere in the past 50 years!

Remember, when it comes to data, we can pretty much believe whatever we want to make ourselves feel better. We see what we want to see, in order to justify our actions.

Average Net Worth For The Upper Middle Class

Now that we've analyzed the data for all Americans with averages and medians, let's look at the average net worth for the upper middle class.

The above average person isn't drawing down capital to survive due to their creation of multiple income streams, smart asset allocation, discipline to consistently live within one's means, and the desire to leave money for loved ones and charities who are in dire need of funding. The Financial Samurai ideology is to leave the world better off than when we first entered.

Finally, the financially savvy person understands the estate tax (death tax) doesn't kick in until assets are over $12,060,000 for persons dying in 2022. In 2023, the estate tax threshold jumps to $12,920,000! That's pretty huge.

Therefore, every single person might as well shoot for accumulating up to $12,060,000 to help other people. But the reality is, anything above $10 million is a top 1% net worth and rich, not upper middle class. After a few million dollars in net worth is considered closer to upper middle class.

Anything earned beyond such an amount should be spent with great enthusiasm while alive!

Be Careful Having Too Much House

One of the problems with the average American is that the value of their house dominates their net worth. The upper middle class (top 20% of Americans) have a net worth where their primary residence is worth less than 30% of their overall net worth.

The upper middle class follow my primary residence as a percentage of net worth guide. A primary home worth more than 30% of net worth is too concentrated.

Conversely, notice how a house takes up more than 60% of the average American's net worth. Therefore, the average net worth for the upper middle class should have a very diversified net worth.

How To Join The Upper Middle Class

If you want to join the upper middle class per your age group, I recommend the following:

1) Max out your 401k and/or IRA as soon as possible. Try and save an equal or greater amount in after-tax investments as well.

2) Think about the proper asset allocation in relation to personal risk. Your assets should be deployed in a way that aims to beat the risk-free rate of return by at least 2-3X. Stay diversified and never confuse brains with a bull market!

3) Voraciously read as much as possible about wealth management, investing, retirement, taxes, and other issues. Subscribe to the Financial Samurai newsletter and the Financial Samurai podcast on Apple or Spotify for free. Don't be afraid to seek professional financial help too.

4) Move to a part of the country where there is opportunity. Give yourself a chance to get financially lucky by coming to areas where there is robust employment and brain share. It used to take two months to cross the country. Now it only takes five hours by plane.

5) Buy a home that you can afford and own it for as long as possible. You'll wake up 20 years from now and thank yourself for having something to show for all your monthly payments. Forced savings through principal payments may sound rudimentary, but most people don't have enough discipline to save on a regular basis.

6) Read personal finance books such as my instant Wall Street Journal bestseller, Buy This, Not That: How To Spend Your Way To Wealth And Freedom. It's jam packed with information and strategies to help you build more wealth compared to the average person. The upper middle class are voracious readers.

More Upper Middle Class Wealth-Building Strategies

Here are more recommendations if you want to join the mass affluent or upper middle class.

7) Build as large of a taxable investment portfolio as possible. Once you've maxed out your 401(k), 403(b), IRA and other tax-advantaged accounts, you must build a tappable taxable investment portfolio. After all, it is your taxable investment portfolio that will generate the passive investment income necessary for you to live free or retire earlier.

8) Don't be afraid to seek professional financial help if you're lost. Put it this way. The more lost you are, the more bang for your buck you get hiring someone to give you advice or manage your money.

9) Make sure you are properly insured: health, life, auto, house, and umbrella policy. Any number of bad things can happen that can easily wipe away your net worth.

10) Work and invest for as long as possible. “Time in the market is more important than timing the market,” as the saying goes. Half the battle is just surviving through all the ups and downs, which is why consistent dollar cost averaging and refining of work skills is important.

11) Once you've properly diversified your wealth, things start getting a little messy. Track your finances through Excel, or a free financial tool by Empower in order to optimize your finances and make sure there aren't any leakages. It's hard to improve what you don't measure.

12) Think positively. If you want to join the upper middle class, believe you deserve to be wealthy. Don't let the government or naysayers keep you down. Use constant failures as learning points.

Build Upper Class Wealth Through Real Estate

To achieve an upper middle class net worth, I highly recommend investing in real estate in addition to stocks. If you look at the average net worth by age for the upper middle class, real estate is a core component to the net worth composition.

Real estate is a tangible asset that provides utility and a steady stream of income if you own rental properties. While stocks gyrate in a highly volatile way, real estate values are more steady and provide higher income yields.

My two favorite ways to invest in real estate are through:

Fundrise: A way for accredited and non-accredited investors to diversify into real estate through private eREITs. Fundrise has been around since 2012 and now manages over $3.3 billion for over 500,000 investors. For most people, investing in a diversified real estate fund is the easiest way to go.

CrowdStreet: A way for accredited investors to invest in individual real estate opportunities mostly in 18-hour cities. 18-hour cities are secondary cities with lower valuations and higher rental yields. Growth tends to be higher due to job growth and demographic trends. You can build your own select real estate fund with CrowdStreet. You just have to do more due diligence on the sponsors and projects.

Both platforms are affiliate partners of Financial Samurai and Financial Samurai is currently an investor in a Fundrise fund.

I've personally invested $954,000 in real estate crowdfunding across 18 projects to take advantage of lower valuations in the heartland of America. The upper middle class are big investors in real estate to benefit from rent increases and property price increases.

Due to my real estate investments since 2003, I've been able to handily achieve a net worth far above the average net worth by age for the upper middle class. The key to building great wealth is through aggressive saving and savvy investments. Real estate is a proven wealth-builder long term.

FinancialSamurai.com was started in 2009. It is one of the most trusted personal finance sites today with over 1 million organic pageviews a month. Financial Samurai has been featured in top publications such as the LA Times, The Chicago Tribune, and Bloomberg.

Join 60,000+ others and sign up for my free weekly newsletter here. The Average Net Worth By Age for The Upper Middle Class is a FS original post.

Love your articles! I am 45, have $450k equity in house, $525k pre tax savings, $150 post tax savings, $400k value in equity in my business I hope to sell by the time I am 50. We save $42k per year towards future retirement and save $25 in cash we keep in brokerage saving account we aren’t 5.25% intrastate in. My question is can we partially retire at 50? My wife and I plan to earn a living but at a reduced income. We won’t need to pull money from savings but plan to let the $1.4m in investment grown between 50 and 67 when we plan to take distributions. At a conservative growth rate we should have at least $3m by the time we reach 67. Is this feast?

A conservative growth rate is about 6%. Some financial planners use this figure when they work with their clients. 2022 was a year both stocks and bond did poorly. Otherwise, a split of 65% stocks and 35% bonds should do well in a long run. You should definitely put your pre-tax savings in this. Also you could try to move some of the pre-tax savings into Roth and pre-pay the taxes, but it makes no sense to overdo it. While a full retirement @50 is too risky, a partial retirement may work, but it depends on how much work you are willing to do. Potential medical costs could ruin you finance if you don’t plan it well. So you should at least make enough to cover the costs your health insurance + some money for any potential major fix-up costs for your residence. Equity in your primary home should not be counted unless you would relocate. Also the equity in your biz could fluctuate greatly. It all depends on how much a buyer is willing to pay.

What do you think about investment in vacation homes? I bought one in 1999 for $490K and today it is paid off and $3.2Mworth

Congrats! Where is it located?

In general, vacation homes are a bad investment. Underutilization and first properties to decline during a downturn.

I’d love to hear more details about your home. Thx

As an under 35 man who fits in the average networth, you should also mention crypto as a way to diversify. I’ve made quite a bit of my money off it and I’d recommend others put a small 1-5% of their money into it as a speculative asset.

As younger retirees (50’s) we are very pleased and grateful for our financial position of several million, but, most importantly, we are pleased that we, and our kids lived the lives we wanted to live along the way, with homes on the Southern CA Coast, as well as via other lifestyle choices we made when we were young. We knew what we wanted and didn’t want at a fairly young age.

Everyone has different dreams, so I can’t say enough about how important it is to make good financial decisions at an early age, with a sustainable long-term plan, so you can live the life you really want to live as early as possible.

I’m 60, been a high school teacher for 35 years, almost always worked a second job too. I have a net worth of 8-million and I plan on working 4-5 more years because I love my job. So I’ll probably be worth more when I retire in a few years. I’m single, love working and helping others. I deliberately and methodically saved in my Roth, 403b, and pension accounts. I’ve saved and bought a couple of so-so homes and paid them off — nothin fancy.

It just didn’t seem that hard to become upper-middle class or rich for that matter. Just get educated (doesn’t even need to be a great university degree/major) and goto work for 35 years +, save tax deferred (don’t even need to make great returns on your invested savings,) try to stay healthy and eat well. Buy a little real estate, nothing fancy. Don’t tell people you are a millionaire, dress in Walmart clothes, drive an old car, mow your own lawn and paint your own house. Success starts with a 50-60 hour work week, for a few decades. It worked for me.

Love it! The power of consistency and time. Having that low operating cost is also great.

Any fun plans on how to spend the $8+ million?

land is the basis for all wealth

I agree to a point. Too bad there is so much property tax to the point where after paying a certain amount, it’s unbearable.

What is equally important to accumulation of assets is the fact of how one spends down one’s nest egg. Many, if not more assets are lost in the spending (sourcing of income, taxes) as in the build-up to retirement!

“There’s a huge 37% decline in the average American’s net worth for the same period (55-64 to 75+), which may signify that the average American isn’t as adept in making their money last into retirement.”

I don’t think this signifies anything about their adeptness. Not everyone’s goal is to leave a huge inheritance after they die. Maybe that’s the “Financial Samurai Way”, but not everyone has to have the same goals. Not everyone has kids (or if they do, then perhaps leaving some inheritance may be a nice-to-have but not a priority), and most people feel good enough about leaving what they do have left to charity without stressing that it’s not 100% of the principal they retired with.

In fact, within the FIRE movement it’s much more common for people to actually desire to draw down principal rather than keep their principal perfectly intact by the time they die. It would be nice if my investments do better than I expected so I can leave a large amount to charity, but I’m not going to go out of my way and work several more years just to ensure I never draw down principal. If I outlive my money and am able to leave at least some for charity when I die, I consider that a win. If I never draw down any principal in retirement, I would actually consider that a personal failure in planning too conservatively and working way longer than I needed to.

Also, I agree with some of the comments the first chart should be redone using the median. You have a section below where you talk about the median, but you never made the chart or showed the numbers. Drawing conclusions about how ok Americans in general are doing based on averages rather than medians is pretty meaningless.

Yep, see the book, “Die with Zero” for a good explanation (and solid defense) of spending down your money before you die.

The only problem with the book is the author is worth over $150 million. So it’s much easier to tell people to spend all the money when he himself will likely not be able to.

I just turned 27 and am building my second house on a lake. I have over $130,000 in real property paid off except $9,000, about $480,000 in my businesses liquidity and $15,000+ in tools I also have precious metal investments. I am going to start renting my second house out and eventually buy large apartment complexes. I’m doing well but I will do better just getting started.

Congrats! Keep on prudently going!

Upper middle class is is lifestyle. Umc people usually have college degrees, high incomes (low-mid 6 figures), and a great deal of autonomy in their work. It has nothing to do with being responsible or saving in a 401k. It depends mostly on your intelligence and the type of career you’re in. Working a blue collar job and saving money for 30 years doesn’t make you upper middle class. It just makes you a middle or working class person with money. It’s not the same thing.

“It depends mostly on your intelligence and the type of career your in.”

That’s the dumbest comment I’ve heard on here…

There’s plenty of blue collar workers that have high paying jobs, and who also have education. Yet they choose to work outside the confines of an office and house/community they cannot afford.

Your describing what’s called being a snob and wannabe elite Nothing cool or classy about either. In fact, I’m m glad you made that comment, because it’s a reflection of those with your mentality living in a delusion.

Your sense of superiority is amusing.

I do believe there is a difference between having a high income and having a lot of assets. I do believe you need to save and invest a high-income to become wealthy or possibly rich — especially if one starts with little to nothing.Earning a lot of money is one thing, but keeping and growing that money via savings and investment is another — one has to save and invest for retirement.

I know people who have nice homes and cars who don’t save and they are only a few paychecks away from insolvency. Upper middle class is everything you said in your introductory sentences, but it is so much more — saving, investing to grow one’s wealth. The old adage, “It’s not how much you earn, it’s how much you keep, grow and invest,” really is true when striving to move up the American class system.

“But, the biggest surprise is the $843,800 average net worth figure for the typical American ages 55-64. That’s almost like saying everybody who is between the age of 55-64 is a millionaire!”

It’s not though. The median is likely incredibly far below $843,800, because we know distributions of things like income, net worth, etc., are very positively skewed. That is, you could have one person with a net worth of $50MM and 49 people with a net worth of $0 and still end up with an average net worth of $1MM. I wouldn’t be surprised if it’s only 10-20% of people in that age bracket that have a net worth over $1MM.

K-Man, you’re correct. Why would anyone use the average (the “mean”)? Every other website uses the median or at least shows both the mean and median. The way this is shown is completely inaccurate.

Curious, why strive to be median when you can strive to be average?

Don’t be average but the median is a better reference point where you are. Percentiles would be better still.v

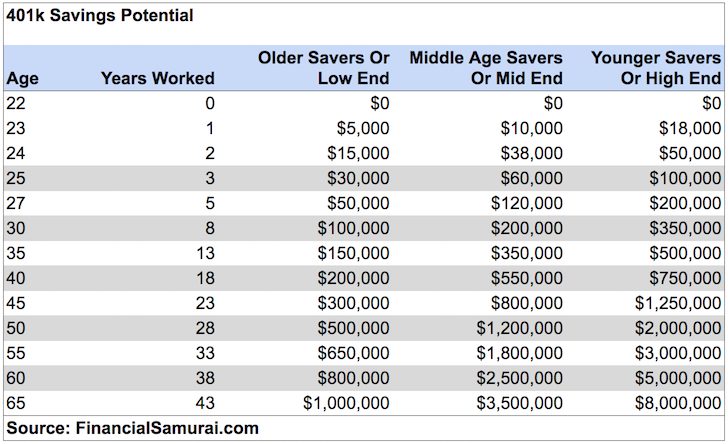

How do arrive at $596,500 for pretax savings at age 45 from the 401k table above (i.e., how mid end savings of $800,000 got converted to $596,500 for age 45)?

And, do you have similar data for couples where one spouse is a homemaker?

My IRA and 401 (tax deferred) accounts are about $2,000,000 with an additional money in taxable accounts. Actually, the tax deferred accounts (while this is their listed value) are worth less, as I owe taxes to the IRS as I withdraw the required minimum distribution. How do I account for this when computing net worth?

I went back and was reading your original charts. Each of your charts starts out with the “average person” or “above average person” or the “average American”.

How do you factor in married couples. In the above average category what is the case? Is it double the number we see or is it one half of the number we see.

Good question.

Check this out: https://www.financialsamurai.com/the-average-net-worth-for-the-above-average-married-couple/

I think these numbers are high for above average in the 30’s but low in the 50’s. My wife and I are 31-34 and our combined net worth is $550k. I’d be surprised to see many our age have a net worth that is much higher without inherited wealth. We have no debt (cars, mortgage, student loans) and are now saving $200k a year. I’ve done some projections and it’s crazy what we will end up with later in life. I think everyone’s real problem is the fact that they need to lease new cars, take expensive vacations and don’t enjoy saving. There is nothing better than watching your net worth increase every paycheck. Work hard, don’t have kids outside of marriage, and don’t get divorced. In my opinion these are the keys to success.

Hi Chad,

There’s more of us than you think. My wife and I (27-30 have) have a combined net worth of about 900K and we are both teachers. We started with nothing but I’ve heavily invested in real estate. I’m not sure that the early numbers are that far off.

Wow! That’s great!

I’d love to profile your story if you are willing to share. Please send me an email. I do want to ride profile about teachers.

Email sent!

So, I am nearly 70, single, and have an income of about $60K, but a net worth of about $2.5 million (thanks to compound interest).

Am I upper middle class or lower upper class in terms of net worth?

(Not that it really matters. I have far, far more than I need to live on and my goal is to give almost all of it away before I die, leaving enough for Long Term Care should I happen to need it and enough for the funeral. Still, it would be of curiosity to know.)

Hi John my name is Cheryl I found your comment very interesting on the site I wanna know how to do compound interest I’m very interested because I would love to have a good nest egg by the time I reach retirement can you please help me in the situation so I can make the right steps thanks

Thank you for the article and data. It would be nice to see the top 1% remove from the data to take out the extremes. But in the end the way I look at my work, earnings and savings is that I really only compete with myself. What do I need/want for my family and self. If you focus on what the neighbor has you become very jealous society. Have a market where individuals can succeed to their own desires and levels.

Good article, although it may be a bit technical for those just getting started.

It all boils down to hope: yes, you can get there! Just about everyone can become “mass affluent.” If you live like you’re never going to have two dimes to rub together, that’s where you’ll end up. Live like you can become well-off, and you’ll go that direction instead.

This isn’t just opinion; I’m doing it.

It would be good to develop a chart of net worth for people who don’t live in the expensive cities (nearly anything along the CA coast and some parts of the east coast. The upper middle / above average tend to live in big cities, earn more, have higher valued houses, and also face more expenses. Wouldn’t that skew even the median? You suggest that retirees move to North Dakota (weather is an issue). It can noted that for those no faint in heart, there are a number of semi-abandoned small towns in Kansas. Colorado looks great in a few spots, but I am digressing. In other words, regionally adjusted comparison – like the PPP (purchase power parity) used to make cross-country comparisons of per capita GDP – would be helpful.

You’re free to adjust the charts down to whatever makes you feel happy. But then, that’s kind of like moving the goal post to make scoring easier.

The federal tax code doesn’t tax less for those who live in SF where the median house costs $1.5M to give them a break. They’re argument is, who cares if your job is there, move if you want to save money on housing. It’s a free country.

I often find it’s programmers, lawyers, doctors, engineers, and other “professional” people of means who make these websites and financial blogs (which themselves often earn quite a bit for the writers.). about 50% of the working population makes less than 30k gross before taxes. I agree that living within ones means and investing is smart, even though we are likely looking at a nasty nasty bubble bursting coming up, it will no doubt recover long term, should the ecology of the planet not shit the bed.

However, one needs to have means first, and that is decidedly uncommon, the data makes that plainly clear. No how matter how much anyone of means, who’s often found said means by luck (yes the data suggests that as well), says that it’s all about gumption, grit, hard work, and go get’em bootstrap pulling, is selling you a myth. Why Because finding high paying work that allows for this kind of savings requires exactly that, luck. Studies show the poor tend to stay poor, and the affluent tend to stay affluent. Exceptions are just that, and using them to constantly suggest people can do better is misleading.

As you note, median is much more accurate….by quite a bit.

“It may also be surprising to learn how much of a person’s net worth is tied up in his or her home. If you exclude home equity from the net worth calculation, then the median net worth drops significantly across all age groups. For example, the median net worth for a person age 70 to 74 years drops to $31,823 from $181,078 when home equity is excluded.”

The costs of food and housing and education and health care and transportation and child care and taxes have been well-defined by organizations such as the Economic Policy Institute, which calculated that a U.S. family of three would require an average of about $48,000 a year to meet basic needs; and by the Working Poor Families Project, which estimates the income required for basic needs for a family of four at about $45,000. The median household income is $51,000.

The Official Poverty Threshold Should Be Much Higher

According to the Congressional Research Service (CRS), “The poverty line reflects a measure of economic need based on living standards that prevailed in the mid-1950s…It is not adjusted to reflect changes in needs associated with improved standards of living that have occurred over the decades since the measure was first developed. If the same basic methodology developed in the early 1960s was applied today, the poverty thresholds would be over three times higher than the current thresholds.”

The original poverty measures were (and still are) based largely on the food costs of the 1950s. But while food costs have doubled since 1978, housing has more than tripled, medical expenses are six times higher, and college tuition is eleven times higher. The Bureau of Labor Statistics and the Census Bureau have calculated that food, housing, health care, child care, transportation, taxes, and other household expenditures consume nearly the entire median household income.

CRS provides some balance, noting that the threshold should also be impacted by safety net programs: “For purposes of officially counting the poor, noncash benefits (such as the value of Medicare and Medicaid, public housing, or employer provided health care) and ‘near cash’ benefits (e.g., food stamps..) are not counted as income.”

But many American families near the median are not able to take advantage of safety net programs. Almost all, on the other hand, face the housing, health care, child care, and transportation expenses that point toward a higher threshold of poverty.

Very strange stuff. I have a net worth of over 2 million. How come I don’t feel upper middle class? I drive a 10 year old car, live in a 2000 square foot house and wonder if my cash flow will last for a possible 30 years????????

It’s probably because you’re comparing yourself to people who have more. But if you come up with a plan, and do an income and expense analysis, you’re probably going to be fine.

But $3 million is the new $1 million. That’s all thanks to inflation. So perhaps when you came at one more million dollars you’ll feel good.

See: https://www.financialsamurai.com/are-you-a-real-millionaire-3-million-new-1-million/

I believe part of what skews this too is the fact that people 55-64 are more likely to have their parents die, and thus, potentially inherit larger sums of money than they would have earned otherwise.

I came to US since I was 18. Study and work, open 2 failed restaurant but I was pretty aggressive investor. My net worth around $2.8M that real estate(no loan), 401K and cash. I still feel poor, live normal life, golf once awhile, shop for bargain, never fly business class, eat at home most the time.

lunacy

upper class 40%

upper midlle class 10%

middle class 10%

working class 5%

homeless 35% (like the upper class, homeless in urban areas on sidewalks and parks, upper class on their estates, have in common: impromptu: doing the bugaloo, charleston, one man waltz, , mazurka, etc gesticulating wildly towards the sky, soliloquy, giving speeches and believing you are the King of Spain, receive radio waves from extraterrestrial civilizations, etc

It’s a nice article. For upper middle income folks, the table says it is “average” rather than “median.” It would be interesting to see if the median is much different from the average.

Thank you for writing this article. I read it a few years back when I just started working after graduating college, and I was 22. I hardly had anything in my savings, my Roth was sitting at about $4000, and I had never even heard of a 401K.

My starting wage at my new job was rather low (for an Econ Bachelors at U of Mich) and I was very discouraged that I would be unable to match these numbers. My savings rate potential was low and I had to move to a new location and live alone (paying all my bills from the start). However, after a few months of living paycheck to paycheck, I saw my assets start to stabilize and grow. I took your advice to max out my Roth and pre-tax 401K match, then proceeded to hoard any money I didn’t spend into an online savings account – so maybe a 1% return every year pre-tax.

Looking back, I realized that these age ranges are good touchstones for where you should aim to be. Now that I am 25 years old, I am actually within the $70,000 asset range. Still paying off a $12,000 car loan, but I learned that is considered equalized if I just sold the car for full value (also took your advice to read up on investing/asset management). Now I have quite a bit of liquid cash to put into a Betterment account and wait out the fluctuations of the market.

Thank you again for helping someone just starting out after graduation!

WELL DONE Diana! And good job for not looking at these figures as impossibilities, but as achievable targets to keep you on a great financial path!

Give yourself 10 years of disciplined savings and investing, and you will be absolutely AMAZED by how much you will accumulate by age 35. With such wealth, you will have more options to do what you wish. We all burn out eventually and want to do something new. Please share the message!

Check out: Investment Strategies For Retirement Based On Modern Portfolio Theory

Best,

Sam

I just googled “net worth by age” and came across this article, WOW!

This is incredible, love the 10 steps on how to get to the upper-middle class. I’m proud to say I am doing all but one of them and plan to add umbrella insurance this quarter to protect myself.

Also love the last one, a positive attitude & believing you deserve to be wealthy is so true!

Wonderful Google works! :) The abundance mentality is super important. I’ve shot myself in the foot too many times to count.

https://www.financialsamurai.com/abundance-mindset-to-grow-wealth/

In my opinion, Anyone with confidence and ethical determination can build a net worth above the average person. Even as a single parent to 3 kids…in my case I was a single father. I grew up poor, crying single mother, stress. I searched out mentors and successful leadership. Worked through 4years of University. Confidence building years. Then entered the real estate field. Through real estate I purchased my first 4 plex at 32 years old (Bay Area 1992). Lived in the 4-plex, raised three kids until they were 9, 10, and 12. then used the equity after ten years to purchase 160 acres with creeks and forests to raise them better in a house that needed work. Once the home was comfortable, I used the cash flow (from 4-plex) to buy a small commercial building and found a good tenant after years of remodel and elbow grease. The next building was another single tenant commercial property just 6 years later. Kids now grown and back to full time work in real estate sales for 3 years of total committed hard work I purchased another 4-plex and then an amazing (but dated) house for rental and then another house. At 56 years old, my Net worth is 3.25M and my annual cash flow is $105,000 not including $200,000 per year in real estate commissions. Children raised and retirement in sight for travel.

In the “household wealth is flat” chart, I can’t help but wonder if part of it is like a reverse of the “enough is enough” mentality mentioned in another comment regarding retirees. Whenever something is defined as a “household” metric, I wonder about the other factors in households, mainly being people living alone or with other people. Maybe wealth seems flat per household because as people are more affluent, they tend to live alone longer, since there is less financial need/incentive to “shack up” to save on living costs. For example, a two-person household with a combined net worth of $60k looks like more than a single-person “household” of $45k, but the lower household figure is a 50% per-person increase.

But I guess that goes along with your “you can do whatever you want with data to get the picture you want” point made with the graph. :)

Excellent article. A few points:

1) The net worth should include non income producing assets (such as the primary residence and cars should be excluded) only. A person’s primary residence and car loans should simply be tracked separately as liabilities, which is precisely what they are until paid off in full. Once said off in full, all that means is that the person has a place to live and a vehicle to drive around.

2) The net worth does not account for pensions for those who happen to work for the government. Neither does it account for the social security contributions (a pension for all of us) made by working people. Net worth enthusiasts for example would deride a person earning $100k+ but with very little net worth and extol those who earn $50K with a high net worth. I agree, but the missing part of the equation is that the person earning large incomes through their lives have by default large SS contributions and thus large SS payouts. Thus, net worth can horribly underrepresent a person’s true worth.

3) Net worth calculations should also be adjusted upon specific family situations. For example a double income couple with 2 professional degrees and white color jobs without any kids will by default be almost rich in this country if they are not “money stupid”. Many double income earners can manage 1 kid (barely), but with 2 kids, demands start rising up. Not only 1 spouse sometimes takes off/reduces work, you also have to feed/cloth/raise 2 human beings and possibly send them to college. This can significantly alter the net worth picture. Also, the timing of when kids are born is paramount. Kids born at a young age ca derail professional development. Kids born when the couple has already ascended the corporate ladder doesn’t make a big dent.

4) Obviously, location impacts the net worth in a big way. Living in SF, NYC, DC, LA etc. should require your net worth maybe 2X – 3X compared to living in the rest of the US.

In short, I find that a blanket “net worth” chart – while helpful – does not add contextual information desirable for my specific case. The question “how I am doing” remains unanswered.

A few simple suggestions are as follows:

– Consider your income at age 40. Call it X. I like this income because it can somewhat describe a “median income” you would have earned your life.

– Consider the number of years you would have worked. Call it Y.

– You should save at least 15% of your income through your life (employer match included) in a tax-shielded retirement instrument (401K, IRA). Taking X as the baseline, your own contributions to this retirement instrument should be 0.15 * X * Y. I like to see Y as 25. This leaves a person a few years of enjoyment without work and not too few as to having missed peak earning years. Thus, your own contributions to this fund should be about 4X. If X was $100K, this means over the working years, you should have put $400K in this fund. Let the market take care of the rest of the investment gains.

– The primary residence should be paid by age 45.

– At least 1 secondary rental real estate should be owned. Preferably 2. That’s a nice cashflow on the side. These should be owned outright by 55-60 and all the rent should go to your own enjoyment.

– Make sure you send your kids to the college. How you do it – it really depends. I did not invest in a 529. I lived very frugally for 3 years of my life when I was unmarried and earning relatively high. I saved close to 80% of my take home income and invested it. That investment is enough to finance college education for 2 kids in state schools and even more.

If these things fall in place, life will be good. I would not look at a single net worth number and look at the larger picture instead.

Best,

Don’t forget that SS isn’t a savings or investment account. It is simply paying for current retirees. It could change or go away at any time, so any inferred future promise from current contributions isn’t actually an asset to add to net worth. In accounting speak, it isn’t a true receivable because there is no obligation (I’m a CPA). ;)

Pingback: Solving Financial Insecurity To Live More Freely | Financial Samurai

I think this is a great post and exactly what I was looking for–benchmarking myself to an appropriate category/goal. I’m a young professional and certainly seeking to stay in the upper middle class. However, I have one minor question and disagreement regarding post-tax (non-retirement) vs. tax-deferred (pre-tax/retirement accounts).

Why do you think the allocation toward pre-tax accounts should be that much larger than post-tax while you are young–say, under 35?

My thought is while I am young, to contribute to retirement accounts up to the company match, and then keeping the rest of my net worth in taxable dollars.

Reasons are:

1) not at the top tax bracket yet, thus less expensive to have taxable dollars;

2) before 35, generally significant expenses such as house purchase, engagement ring, wedding, etc.;

3) keep liquidity for potential opportunities–“cash is king”;

4) use after-tax dollars to buy RE and rent it out for another stream of passive income, which is generally not taxable due to depreciation–could be a retirement vehicle in itself.

Looking forward to your response.

Pingback: Scraping By On Five Hundred Thousand A Year | Financial Samurai

Pingback: The Top 1% Net Worth Amounts By Age | Financial Samurai

If we were to count or “appraise” the value of various pension plans around the country as a partt of an individuals net worth, many recipients of pensions, whether public or private sector would be considered multi-millionaires.

I would highly agree. A public pension is worth millions. The question is how broke the private citizen will be after they are taxed to death to fund those pensions.

How do you explain the middle class wealth collapsing when most of their wealth is tied to real estate? In you other article you state real estate builds wealth the best. Maybe there are some costs that aren’t being shown in your real estate wealth article (property taxes / insurance / maintenance).

Jim,

Excellent question! We’re right now still in the national RE recovery mode, unlike in certain cities where values have far exceeded the previous peak now.

Due to selling off property near the bottom, taking out HELOCs, not paying down extra principal, and still recovering, property may not have helped as much as it should. But, it has if you compare the median net worth of a homeowner to a renter. It’s literally 30-40x higher.

To Go long property, you have to own more than just one, otherwise you’re neutral.

I am at early to mid 30s and married with networth $3.5mm including 2 cash paid condos in NYC, 500k in retirement account, 500k cash, and 700k in shares. my goal is to reach 5mio then retire. hopefully i can do it in 5yrs.

I think I’m on the right track here. Have a primary condo with about 60k in equity in it. Also 3 other rental properties which generate some nice income, with combined 100k in equity or so. MM fund with about 100k, and IRA and stocks with 150k. 400k net worth or so, and I’m not quite yet 36. I could work and make more money, but I would rather chill out and take 3 months a year off, and do what I like to do. This site is very helpful!

While contrarian from most comments above, I actually think most of you may be understating the potential effects that outliers have on the average values. As a simple example:

If I take a weighted average of $100K (weighted at 99.99%) and $10B (weighted at 0.01%) the average comes out to about $1.1M average net worth. Obviously, this is an extreme example, but the major outliers can cause pretty big swings on this type of data. Just a thought…

Pingback: Social Security Will Make Us All Millionaires In Retirement | Financial Samurai

These posts are very motivational and it changed my life and attitude towards money. I wish you would have been a blogger back in the dot com days! :) I discovered your blog in 2011 and it was rude awakening for me. Like many other Indian immigrants, we were good at saving money but not savvy at managing it. While we had around 250k in cash sitting in the bank, we had zero assets. We had less than 30k contributed in our 401k invested in some treasury bond fund! We started maximum contribution to our 401k in 2011 (250k now, have a lot of catching up to do!). Bought our primary house and 2 investment condos in the next couple of years. Added money via back door roth (I know you are not a big roth IRA fan, which is about the only thing I disagree with you on). Invested in the stock market, 529’s for the boys etc. I joined PC after you mentioned it in your blog and as of today our net worth is $1.4 M. And if I add the property that I own in India, I am at around 1.65. I am 41 and my wife is 39. Even though I am working in tech in the bay area, I am also working on getting my mortgage broker licence as a part time gig. I am hoping I will have some additional income coming from there. I have now set a goal of $10 M net worth in the next 15 years. By then my youngest one would be through college. While we might be able to to retire a lot earlier we both love our jobs and will not mind doing it for another 15 years or so.

If you had any doubts if your blog made any difference to peoples lives, you have at least one family for which it did… Thank you, Sam!

Wonderful to hear Sunil! Sounds like you’ve really supercharged your wealth since 2011, and I’m glad Financial Samurai was the rude awakening to help you mobilize your income and wealth!

I was going to write a post about what people have to show for all the income and hard work. It’s interesting to see how some people who earn modest amounts of income can end up with so much, and some people with very large incomes can end up with so little.

Sounds like a interesting story. The initial 250k was somehow quadrupled in 4 years. I get the 401k max out part. Are you talking 1.4 mil in assets or net worth?

Bay Area housing math. Interested in hearing more details about this one :)

$1.465 Net worth! Here is the math:

2011: 150k down on primary home for 730k which is now worth $1.15M. Loan balance of 540k = 610K equity

2012: Condo 1: 60k down on 240k condo which is now worth 430k. Loan balance of 175k= 255k equity

2012: Condo 2: 80k down on 370k condo which now worth 470k. Loan balance of 280k= 190k Equity

250k in 401k+ 30k in roth + 50k in 529 + 80k stocks and cash. Total $1.465

Pretty crazy huh?! We have modest salaries by bay area standards ($100k each), but we don’t want to go after the start up lottery or higher salary. Been there, done that… just not worth the stress!

Thanks for the followup post. Awesome, stuff!! Their could be a housing bubble out there (opinion). Be safe.

Hmm…never (ever) thought of myself as mass affluent/upper middle class. For clarification purposes do you propose including the equity of a home??

If so I’m at ~ $1.09M net worth at 54.5 yrs old. Single male at this time.

Maybe living in Seattle WA where Microsoft, Amazon, Boeing, Nordstrom, etc. are located and it tends to make someone “less affluent” since our COL is a bit higher. Entry level homes are $450K in SEA.

I’m 22 going on 23 and coming up on my 1 year anniversary at my job. My current NW as calculated by PC is right around $40k. I am a ways off from the $349k number, but I’m more than halfway to the $73k Federal Reserve average and getting by based on the FS chart. Not bad, I think, but now I’m aiming for that $349k number. Good to see these numbers laid out. Thanks for this post.

Good thing the age range for $349,000 is up to 35. You’ve got 13 years to get there. With you $40k now, I’ve got little doubt you won’t surpass that figure!

I don’t know too many under 25 year olds who spend time reading personal finance blogs. Everybody should, but life gets in the way.

Sam,

Your chart is spot on…the wife just turned 40 and I am 44, and according to your chart our net worth should be $1.574M. As of yesterday, we are sitting at a net worth of of $1.613M. Props to you….

Stephen

Stephen, perhaps more appropriate is saying props to you!

Cheers

I didn’t read through all of the comments, but I was wondering if the wealth numbers by age could be broken down into quintiles and/or then further into the top 10%, top 1%, and top .1% for each age bracket (a bit more informative than just using average and mean, though mean is, I feel, more telling). I know that would be lots of graphs, but you make them look so pretty ;)

Thanks for the great article!

I think you’ll enjoy these two posts:

How Much Do The Top 1% Make By Percentages?

Top One Percent Income Earners By State

Some nice graphs for readers.

Excellent post. It’s truly motivating to see these numbers. I would take a small exception to your statement that “None of us have to live in expensive cities such as San Francisco, New York, Honolulu or Los Angeles during our non-working years either. We can hop on a bus to Iowa, Indiana, South Dakota, or Louisiana to allow our net worth to last longer.”. While that is true for most Americans, same-sex couples who are married can’t move to those states, or at least not if they wish to keep their legal marriages and all the legal benefits that provides.

Gotcha. I’ve always looked at marriage as a penalty due to the marriage tax.

I know that inheriting a partner’s Social Security benefits if they die is one benefit. Could you list some other benefits of legal marriages? Thanks

Related: At What Income Level Does The Marriage Penalty Tax Kick In?

This is great data. Thanks for compiling everything. The “Average Net Worth of an Above Average Person” (great title, by the way) is very motivating. That’s a lot of money for young folks!

So what net worth would classify you as rich?

Depends on age and cost of living. For expensive cities, probably anywhere between $5 – $10 million. Rich to me, means not having to work, while having your money generate enough income to live a comfortable life. Maybe I should write a post about this and do a survey.

If you have $5 million liquid, you should be able to generate about $110,000 risk-free a year.

Yes please write a post about it if you can. I would be interested to hear more on your perspective.

Accoridng to Felix Dennis

“According to my tables of wealth, “rich” starts at a total asset value of $30 million- $80 million (also known as “the lesser rich”).”

So I guess you definition of rich is essentially more about comfortable life than affording all the luxuries

Would you agree with him otherwise? He is a multi-millionaire after all.

Probably not very pertinent or useful to listen to a multi-billionaire’s definition of rich.

Share with us what your definition of rich is.

My definition is wealth is pretty much the same as his:

“Rich enough to retire, or to work eighteen hours a day, or drink yourself

into oblivion every night—if that’s what you want. Rich enough to smile sweetly or sneer at bank managers, depending on what you had for breakfast that morning; to turn your relatives green with poorly concealed jealousy while they creep around with their hands out; rich enough to buy a massive yacht (I don’t advise it, though) and sail away into the sunset like

the Owl and the Pussycat for years on

end. Rich enough to live where you want, to go where you want, to do what you want, to meet who you want. Rich enough to buy the only two things apart from health and love worth fussing about in life. Time. And the option of not having to be in any particular place on any particular day doing any particular thing in order to pay the rent or the mortgage.”

I found these definitions in the book.

Wealth measured by Cash-In-Hand or Quickly Realizable Assets

$100,000-$400,000 – the comfortable poor

$400,000-$1,000,000 – the comfortably off

$1,000,000-$2 million – the comfortably wealthy

$2 million-$10 million – the lesser rich

$10 million-$30 million – the comfortably rich

$30 million-$70 million – the rich

$70 million-$100 million – the seriously rich

$100 million-$200 million – the truly rich

Over $200 million – the filthy rich and the super rich

Wealth measured by total assets (true net worth)

$2 million-$4 million – the comfortable poor

$4 million-$10 million – the comfortably off

$10 million-$30 million – the comfortably wealthy

$30 million-$80 million – the lesser rich

$80 million-$150 million – the comfortably rich

$150 million-$200 million – the rich

$200 million-$400 million – the seriously rich

$400 million-$800 million – the truly rich

$800 million-$1,998 million – the filthy rich

Over $1,998 million – the super rich

This is an old post but I feel compelled to comment.

This is just a slap in the face of an average person. An average person honestly does not need 10 million or more to be financially independent. People know how to live on less if needs be. And getting that kind of income even on the highest pay scales is impossible.

Yes, of course there are lots of entrepreneurs and they drive the economy and some of them should and will get that kind of cash. They will miss other things in life. Believe me, every experience in life is worth living the life of. If you are filthy rich, you are missing the joy of sacrifices (no it’s not a spelling error). Getting everything handed to you on a silver platter can easily ruin you and there are countless examples out there.

So saying that someone with $400K cash is “comfortably poor” is just some rich ass’s way of showing a middle finger to plebs like us. Whatever. It should not matter to someone who meticulously builds a nest egg of $1-2M, has a couple of kids, great friends, and has learnt how to build wealth through sacrifices while simultaneously getting the most fulfillment out of life.

I agree with you completely.

Interesting findings, and solid advice as usual on how to get there. Those living in higher cost of living areas could pack up and move to a lower cost of living area later in life after accumulating a nice nest egg, and either call it a day early or simply live a more comfortable retirement….though some high cost areas are pricey for a reason – they’re great places!

One question: are these figures for individuals or households? A person with $500k is different from a couple with $500k. Just curious.

Excellent post and analysis!

Hi Ray – The PC data is by e-mail sign-up. The person who signs up could include only his/her account info – many times not every single detail – or include their partner’s as well. Hence, a safer conclusion is to treat all the figures as household net worth.

But, it’s always good to build your own wealth. So for those who are so inclined, they can shoot for these figures individually.

Great article! During my free time I read financial blogs trying to gauge my progress and find useful data sparce with little relavence. My life lessons are as follows: 1) Most financial experts on CNBC and Bloomberg are clueless. Your action is to save 25% in SP500 and forget about it for 20 years. When experts scream the world is coming to an end buy more stock. You do not need to be a financial guru, just save consistently. 2) Buy cheap reliable cars and forget about the fancy sheet metal. No one cares what the hell you drive. I had a friend who laughed at me for driving a POS beat up mustang while he drove corvettes and Harley’s . He went bankrupt and lost his marriage. My mortgage is history. 3) Buy a house while you are young and finance with a 15 year mortgage. When you are 45 without a mortgage you will thank yourself. Forget the fancy cloths, vacations, and other junk which robs you of a home. 4) Pay off the credit cards every month or do not own them. They are worse then heroin. 5) Go to church. Giving to others helps provide perspective. Wealth can warp your perspective.

Great Post! Dave Ramsey fan?

Thanks. Dave Ramsey, Warren Buffet, Elizabeth Warren, Financial Samurai, WSJ business section writers,offer great financial advice. Avoid insurance salesmen, TV analyst, and all politically slanted economic advice for example “buy gold now the dollar is going to zero”.

Avoid insurance salesmen

—-

Great advice – until you need it.

I think insurance gets too much of a bad rap. Protecting (Insuring) your wealth is extremely important.

Insurance (i.e. term life, health, umbrella, etc.) is necessary, however sales folks pitching whole life, etc. is not necessary. Big waste of money for consumer, big windfall for salesperson.

And you generally only need life insurance if you have dependents counting on you for their livelihood. The biggest scam, by far, is those companies selling $10k – $20k whole life policies to folks who are in their 60’s, 70’s & 80’s, to be used for final expenses. Give me a break…If your loved ones can’t scrounge up $10k to put you in the ground I would describe that as the height of financial failure…Feels good to vent!

Hey Sam,

My post disappeared…I had a great response to the insurance salesman. Did I offend one of the whole life insurance sponsors?

Stephen

It’s important to bear in mind that if you don’t live in one of the coastal states or one of America’s few truly international cities, you are probably not making enough to sock much away in savings. In a right-to-work state, no one but the most wealthy — who usually arrive from somewhere else — makes a decent living. People who come to my city from the East or West coasts or even from parts of the Midwest are truly shocked when they see their first paycheck. With the exception of NYC and San Francisco, the cost of living in places where people earn better money is not much higher than it is here in the nation’s sixth-largest city, and so the buying power of your salary is much, much lower.

And the counter argument is that it’s too expensive to live in a coastal city to save enough money to get ahead! (See: How To Make $200,000 A Year And Still Not Get Ahead)

Therefore, we’ve all got excuses as to why we CAN’T. Instead, we must start getting into the mindset of why we CAN (Point #10).

Thanks Samurai,

A few random, unrelated thoughts.

I’d like to see your graphs w/ both the median and the means graphed next to each other.

I’m also interested to hear how pensions come into your thinking or this data. One of my parents has a ~10k/month pension whenever he chooses to retire, how do you think about that in terms of net worth or his lifetime health benefits. Obviously these plans are going to be fewer and farther in between as time goes by, newer employees at his agency get far worse retirement benefits than he was able to get access to (he chose to buy into his current plan too over time as well)

As a California homeowner also and from a person who lived through the Loma Prieta quake in 87 what are you thoughts on Earthquake insurance? I think this topic could be post worthy.

Thanks again

Tell your parents CONGRATS for hitting the lottery! $10,000 a month is HUGE, and equals $120,000 a year. That pension is worth about $5 million at today’s risk-free rate. The pension certainly counts.

Public service employees and those with pensions are the truly upper middle class or borderline rich in America!

Definitely a disconnect when you break it down geographically.

Purely by the numbers I’m part of this crowd. But considering I couldn’t buy a single family house in my neighborhood speaks volumes about the relative value of money and the definition of “rich.”

Indeed. But like I write in my first paragraph, the mass affluent aren’t rich, they are upper middle class!

But yes, being in the net worth band, but not being able to afford a house is kind of messed up.

Will you be willing to move?

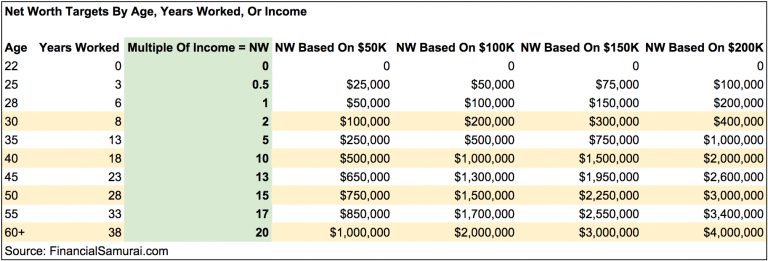

It seems about right. I have a couple of issues with the lower and upper bound. On the lower bound, 100,000 seems off. It would include individuals with below median net worth, which by definition should be excluded from the population. So i would like to see it rerun to be the greater of 100K or the median income bound.

On the upper bound, with the personal capital data, we could probably estimate where a typical mass affluent person hits the cross-over point where the snowball of passive income creates an ever increasing pile of dough. It would just take time series data to identify the point where fewer folks 65 spend down their assets versus where they don’t. That point serves as the upper bound threshold between the mass affluent and the rich, imo. I would guess it’s somewhere around 1.5 – 2M, but it would be interesting to have the stats to back that up.

Back of the envelope, the calcs seem accurate, although i think if you re-run the model, the mid career totals on personal capital would be a bit higher.

Is there a group in between “mass affluent” and “rich” (or top 0.1%)? Like, not super rich / financially free, but doing better than mass affluent. It would be interested to see how that group charts by age.

I found a good article on the income of the top 1% by age, but I think it would be more interesting to understand the net worth trajectory: https://www.theatlantic.com/business/archive/2014/10/the-top-1-percentand-01-percentof-every-age-group-in-america/382094/ (there are plenty doctors and lawyers that fall in the top 1% of income of for their age, but due to very high student loan debt and no early life savings, their net worth is low)

Let’s just call that group the Stealth Wealth class shall we?

The top 1% are everywhere, actually!

Top 1 % income earners are not top 1% in NW, maybe another article to cover top 1% NW people :)

Indeed. Too many people waste their earnings and have nothing to show for.

Hence the post: How Much Should My Net Worth Be By Income! Talk about FS hitting all the main points!

I might have to do a top 1% net worth post by age. Let me see if I’ve got time before my Asia business trip!

Yes please write a 1% net worth post! I need a new bar to reach for, heh.

You got it! I just wrote one and it’s in the queue. I think you’ll find it very insightful and logical!

I would like to see the Personal Capital date as median income, just to get a glimpse at a comparison to the Fed results. As mentioned above I’d like to see housing equity vs stock equity results as a look into asset allocation.

Lastly only data results that would concern me is the clientele bias of Personal Capital and it’s not an issue as long as you consider who is signing up for PC, my guess is the that most people who sign up have positive net worth’s, someone who receives a welfare or unemployment check is highly unlikely to want to know their net worth. very few people would sign up to show negative numbers as well. Also I would think that those signing up are worth in the neighborhood of 100K-1.5mm, just because if you are worth between 2-10 million I’m guessing that your finances are handled by a trusted financial advisor.

Another interesting dynamic would be the state/city data for example San Francisco/Silicon Valley a known tech savvy rich area versus Detroit a city lost in bankruptcy and a state known to have a lower wage overall.

Either way it’s great data to have and look at, thanks.

Or, perhaps people who need the most financial help are the ones who tend to sign up the most in order to receive help? Probably not the majority, but the majority of people who come to Financial Samurai search for an answer online to their financial problem/question e.g.

“How much should I have saved by income?”

“How much should I have in my 401k by 38?”

“How can I retire early and never have to work again?”

“How can I build passive income?”

and so forth. And from there, people follow my advice/thoughts or not, and sign up for products or not.

WHAT?!

Ages 20 – 35 have an average of $349,843 – Apparently there is some fierce competition out there.

Correlating the ‘Average Above Average Net Worth’ and this ‘Average Mass Affluent’ is pretty interesting.

I’m excited to see how the 20-35 group grows wealth. Assuming they are able to keep track (YTY return wise) with the above average; we could see that group shift from ~350 @ 27 as high as ~1,623 @ 40…

Clearly the $349,843 average net worth figure is probably skewed to those closer to 35 than 20. But, the $349,843 figure is significant and very believable based on hundreds of people I’ve personally talked to or interacted with online over the years i this age group, b/c I was in this age group as of pre-2013.

Wow fascinating data. That is very impressive indeed how well the 20-35 year olds are doing that are linked up to Personal Capital. I’m also impressed by the average American net worth by age chart. I wouldn’t have guessed the numbers are that high. Hopefully healthcare and insurance will one day not be so crazy expensive for senior citizens. Doubt we’ll see that happen in our lifetimes though.

Great insights Sam!

It is a self selecting group reporting those numbers between 20 and 35. I had nothing to report until after I was 35. I was flat broke paying off student loans, helping family, buying a business, etc. Even doctors, can’t amass any real savings that early. I certainly would not have joined personal capital pre-35 with my negative net worth and I suspect that is true for others.

As mentioned in the article, I suspect those who leverage technology to manage their finances are probably much more gung-ho about their finances, and probably have more wealth as a result (?) than those who don’t read PF blogs, utilize PC, or create budgets.

But here’s the thing. In this internet world where so much information and tools are free, then who’s to blame if one CAN afford internet access and a device to connect to the internet, and doesn’t take advantage?

Very interesting, but I think there might be some apples and oranges at work.

Do either of these data-sets include primary residence?

There is definitely some pineapples and mango comparisons at work here, which is why I included 3 charts and analysis.

The PC net worth calculation will include all assets a user links, and that can include any homes that are tracked.

I was feeling pretty happy with my progress until I realized this was not per household, but per individual. If you are married and track net worth jointly, you would have to multiply these figures by 2. The average couple/household would have about $1.7M, while the median couple/household would have $500k net worth, at retirement. Am I reading this correct?

I use Personal Capital and enter in the information for both my wife and I under a single account, so our numbers reflect household.

I imagine most people that use Personal Capital and are married do the same thing, so a portion (what portion?) of the numbers in the charts above should reflect a household.

I do the same. It was a real hit to the ego when I figured out the 2x issue. (Honey!!!! We need a lot more scrap money!) Also, I have my mortgages for my home and my investment property included on personal capital so my net worth is skewed down by remaining mortgage balances. Let’s say I owe $100,000 on a $1,000,000 home, personal capital negates my net worth by $100,000 instead of adding $900,000.

You can add your real estate value to Personal Capital so that you don’t run into the problem that you described. In Personal Capital click “+ Link” in the top-left, then the “Add Home Value” button at the bottom of the dialog that appears. You can choose to either manually specify a property value (e.g. $1 million) or put the address and have it auto-populate with the latest value estimate from Zillow.

Actually, don’t get too down on yourself. Every account is registered to a single email address, and we can’t easily determine if that account is for a single person or if it represents a whole household. That is a limitation of the data, as I see it now, and I’m not sure how we solve for that.

Therefore, to make yourself feel better, you can consider the data has household data. And if you want to really get motivated, or depressed, then you can consider the data is per individual.

Check out: The Average Net Worth For The Above Average Married Couple! where I go through your exact same thought process.

Good to know. That was my other question. Any single versus couple data.

I use mint to track household data. But I actually alter the results even further by tracking my investment housing (business) in a separate account, using a separate email. Regardless, the data is still very interesting. And I will definitely think of the data as an individual to keep myself motivated!

I think the most interesting thing about the average net worth of the upper middle class chart, is that it seems to top out at roughly $800k. This says to me that these people seem to figure out a net worth that works for them (that probably keeps them comfortable) and they stop adding to that pot because they don’t feel the need to keep adding to it.

You would think that the older you are the larger your net worth would grow because you have time on your side to keep compounding, but these averages seem to say “I’ve found when enough is enough” and they choose to spend their time on something else besides continuing to grow their net worth.

We may be seeing an artificial cap due to the mass affluent being defined as “accounts of between $100,000 – $2 million” – something to keep in mind.

An even distribution would land the average at over 1 million, which might be worth drawing conclusions from.

This is a good point, which I hope is clear in my post. We created an artificial range of $100,000 – $2,000,000 to define “upper middle class.” Therefore, the averages would definitely be much lower than $2,000,000.

That said, I used the US Federal Reserve average net worth for the second chart, which also shows a top out.

I’m sure there is an “enough is enough” mentality, but I think the appearance of topping out may also have something to do with the data set. The data set looked at the mass affluent ($100k-$2M). Over time the people at the high end of their age bracket remove themselves from the data set and new people come into the data set from the low end. If you run the numbers, $800k is right about the average balance over 20 years for an account starting at $100k and growing by 7%/year with 30k yearly inflation adjusted contributions.

Sam, we like being data nerds too. These posts with real numbers are motivational.

Glad you like the data! It’s hard to draw absolute conclusions, hence the comparison between the PC data, Federal Reserve data, and my data.

I’ve got an upcoming post on “Who Is The Average Financial Samurai Reader” given all the cool surveys folks have filled out over the years. I think the data will be fascinating!

Quite simple. Their investment structure shifts to more conservative models as they enter their late 50’s. Compounding growth slows. Earnings power (outside additions to principal) ceases as the retirement phase begins. Cannibalization of interest and dividends at first; then of principal.

Zee,

I thought the same thing at first too, but then I realized that this is just a snapshot. Remember, there is an upper bound on the net worth of the folks included in the study, so, most likely, a significant percentage of those in the 20-35 and 35-44 age groups will actually end up above the upper limits of upper middle class by the time they get to the older age brackets.

Good point. This is indeed a snapshot. The 35 year olds in the PC study could theoretically end up with MUCH MORE than the 65 year olds in the PC study today.

The next great study would therefore be to track 50-100 current 35 year old PC dashboard users over the next 20-25 years. What a great research study for academics!

The other answer is that the “cap” includes ages up to 64 and a large amount of people are still retiring at ages 62-64 so they basically have ceased the accumulation period and are likely now in the maintenance and drawdown period (e.g. having a nest egg and part time jobs and drawing down from them). Those lucky enough to have existing pensions which replace 50% or more of income no longer need to accumulate and are most likely to draw down but also not as likely to have built a million dollar plus portfolio.

Well what do you know.. I’m upper middle class. :)

Do you have the medians too? Averages can be misleading at times.

Congrats! :)

Besides the median net worth figures in the green chart for all Americans by age, that’s all I got.

For the PC data, you could probably cut the figures in half to find a figure closer to the median net worth by age. The issue is that people don’t track everything on Personal Capital, even though we’d like them to. So, lots of individuals might not have linked stock options, or home values, or 529 plans. It’s hard for us to say definitely that we know what the net worths are of the users.

Median would seem to give a more accurate picture of what US households really look like, but just the averages is interesting.

That is a higher number than expected considering I read very often about how even higher earning households still live from one pay cycle to the next.

Of course, that doesn’t represent everyone, and many people who earn a lot are also smart enough to invest wisely.

Even a very simple and non-sophisticated investor can learn the basics of index/mutual funds and find an allocation that will (probably) earn at least 5-6% over the long term. For people without the interest in learning more and getting closer to a 7-8% return, that’s not bad, and certainly better than the other lazy alternative of putting everything in a savings account and getting <1%.

Some of us spend a lot of time diversifying into new asset classes and increasingly "sophisticated" strategies as we grow, but often forget that even the laziest (or perhaps smartest) person can quite easily capture 5-6% avg returns by simply mirroring the major stock/bond indices.

Hopefully all this knowledge gets out there and the next generation learns about all these tools very early… or at least earlier than the previous generations.

I agree w/ you that investing doesn’t have to be complicated at all.

It’s folks like me who are finance enthusiasts and who love exploring new ways to make a return, who like to complicate the picture.

But I’m always looking for the multi-bagger investment return with about 10% of my investable money. They happen every single month!

I am very surprised by the high average net worth for all Americans aged 55-64. The homeownership rate for that age group is around 80% as of 2012, and the average and median home values are both in the $200-300k range. Even if everyone in that group has finished paying off their home, that’s still 20% with a significantly lower net worth that are averaged out by those above the $844k mark. Am I wrong in thinking that this data suggests that, if you live to 64 in America, you’ll probably be a millionaire on paper?