Everybody should have some investments in stocks. Although stocks provide zero utility, some stocks provide dividend income and all stocks have the potential for capital appreciation. Since 1926 the S&P 500 has returned about 10% on average a year.

Further, at some point in your life you should sell some stocks to buy what you want. Once you've accumulated or made enough, go out and enjoy some of your gains. Otherwise, there's really no point investing in stocks.

Unlike real estate, you can't sleep in your stocks. Unlike fine art, you can't hang your stocks on your wall to enjoy. And unlike fine wine, you can't drink your stocks.

In other words, stocks are useless if you don't sell them on occasion. Stocks are a means to an end.

The Main Things To Buy After Selling Stocks

There are many reasons why you'd want to sell stocks. But first, let's eliminate as a reason believing stocks are overvalued and you expect the stock market to correct. Timing the stock market is difficult.

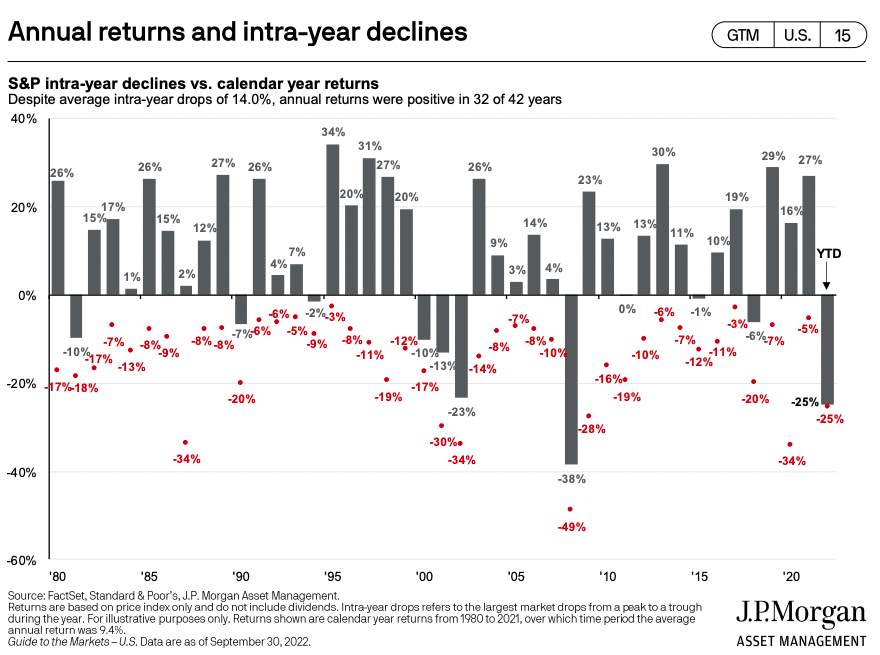

Below is a chart that shows the annual returns and intra-year declines of the S&P 500 since 1980. Despite average intra-year drops of 14 percent, annual returns were positive in 32 of 42 years, or 76% of the years.

Let's talk about some actual things you might want to buy with your stock proceeds. As an investor, you're way ahead of those who just spend all their money now! Here are some top ways to spend your massive stock market gains.

1) Sell stocks to buy a car

If you've been investing in stocks for a number of years, and they have appreciated to where you can purchase a car in cash, then selling stocks might not be a bad idea. The key is to follow, or closely follow, my 1/10th rule for car buying.

If you don't, you will probably regret buying an overpriced car as the stock market tends to go higher annually ~76% of the time. Selling stocks to pay for a car is psychologically more difficult because you're trading a potential wealth builder for a guaranteed wealth destroyer.

But if you need a car for work or to transport your kids to school, then buying a car is a necessity. Just try to pay as little as possible for the safest car you can find.

Example of selling stocks to buy a car

Let's say you want to buy a $38,000 car and the lease or car purchase payment is $400 a month. The goal is to have at least $38,000 in stock investments in your taxable portfolio. But the preference is to have at least $38,000 in stock gains. From there, you can decide to sell stock to pay for the car whichever way you want.

I'd rather pay cash for a car with my capital gains. However, leasing a car or borrowing to buy the car so you don't tie up as much capital may be beneficial. But if you go the monthly payments route, you should be able to pay for the car via your monthly cash flow.

The act of selling stocks to pay cash for a car still gives me the shudders. I drove a sub $9,000 car from 2003 – 2017 because I couldn't stand missing out on potential stock market and real estate market gains.

2) Selling stocks to pay for college tuition

Hopefully, parents start saving for college as soon as their baby is born. One of the most tax-efficient ways to do so is by investing in a 529 plan. After-tax money goes in, but the money gets to compound tax-free and withdrawals are tax-free to pay for qualified educational expenses.

Another strategy is to pay for college with a Roth IRA. The tax implications are similar, but there are fewer restrictions on what you can spend the Roth IRA money on.

Selling stocks and bonds, usually in the form of a target date index fund, to pay for college is easy. For a 529 plan, the funds must be used for college and up to $10,000 a year for private grade school.

In addition, the value of a college degree should equal to at least the total tuition cost you pay to get a degree. Otherwise, you shouldn't be willing to pay it if it won't boost your future income generation power.

If you sell stocks to pay for college, you're actually just shifting assets in your net worth.

Might be hard to use all the 529 funds to pay for college

After potentially 18 or more years of saving and investing for your child's college education, you might not want to use all the funds. I imagine a scenario where I try to convince my children to go to a cheaper public university or a university that offers more scholarships to save money, even if the ranking isn't as high.

This way, leftover 529 funds can be rolled into a Roth IRA to be used for whatever. Alternatively, the 529 plan's beneficiary can be changed to someone else's name, including your grandchild's name. Wouldn't that be nice?

3) Selling stocks to buy a house

Buying a house is one of the main reasons to sell stocks. If you plan to live somewhere for at least five years, it's best to get neutral real estate by buying your primary residence. Those who are able to fix most of their living costs see the economy and life with a more positive light than those who don't.

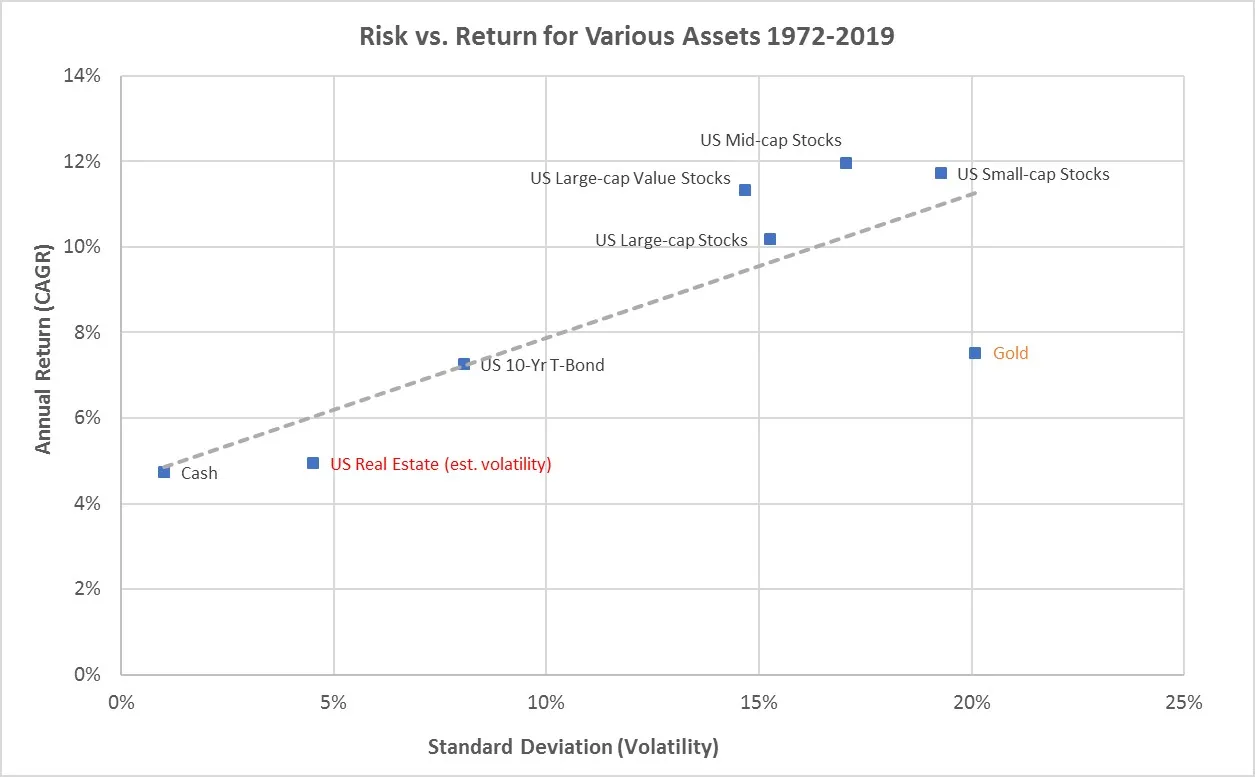

Historically, real estate has appreciated at the rate of inflation plus 1-2% a year, or around 4% – 5%. Therefore, if you sell stocks to buy a house, you're trading a more volatile asset with a higher historical return for a less volatile asset with a lower historical return.

However, depending on the downpayment amount, the returns from real estate could be greater than stocks due to leverage. And if you can enjoy your investment in the meantime, then what a great combination.

If you're afraid of losing money in a home after you sell stocks, consider buying a home with inspection contingencies. If you do, it's like getting a free call option.

Here's my review a year later after I sold stocks to buy a home I didn't need. Although I'm not as rich financially, I'm richer in experience and satisfaction. Life is going by quick with two young kids and I want to provide the best living arrangement possible for my family.

Selling stocks to remodel

Similar to selling stocks to buy a house is selling stocks to remodel. Remodeling is a real pain and will often cost more and take longer than expected. However, once the remodel is finished, you will be enjoy the finished product for years to come.

If you do remodel, I suggest focusing on expansion. Increase the livable square footage of your home to increase the value of your home the most. So long as the cost to build per square foot is cheaper than the selling cost, you are creating instant equity.

After expansion, focus on remodeling the kitchen and bathrooms, then create more outdoor space with a deck. I put together a guide on how much money to spend remodeling for maximum profits.

Buying a dream house with stocks

A dream home came back on the market a year later asking 7% less. I would have bought the home for its asking price last year if I had the money. But I didn’t as the bear market reduced the value of my stock and bond holdings.

Due to my negotiating skills and willingness to let the selling agent represent me, I'm able to purchase the home for 14% less than last year's asking price. As a result, I’m highly tempted.

I wasn't expecting to buy another forever home three years after purchasing my existing forever home in June 2020. But here we are. The only problem is this home requires me to sell a lot of stock to pay cash.

Fortunately, the stock market has rebounded, so I actually didn't mind selling a lot of stock then. I could sell some losers to offset capital gains.

Here are some considerations before selling stock to pay all cash for a house. It's a little trickier than you think, especially with the potential tax consequences.

4) Selling stocks to pay for emergency expenses

Hopefully, everyone has at least six months of living expenses saved up at all times. If so, most emergency expenses can be paid for using the emergency fund plus monthly cash flow and insurance coverage.

However, if the emergency expense costs more than your emergency fund's value, then selling stocks to pay for the shortfall makes sense.

Although there is no appreciation potential paying for an emergency expense, paying for an emergency is a necessity. The money spent could save a life, pay for a deductible for insurance coverage to pay out, or prevent things from getting worse.

5) Selling stocks to fund your retirement

Selling stocks to pay for retirement is usually the main reason why we are encouraged to invest in stocks in the first place. However, after a lifetime of investing in stocks, it's often difficult to decumulate. Instead, it feels much better to invest in dividend-paying stocks and try to live off the dividend instead of the principal.

In retirement, we will hopefully receive income in the form of Social Security benefits, pension, passive investment income, and/or distributions from our tax-advantaged accounts. The more income sources for retirement the better.

However, if we only have Social Security benefits and our 401(k) or IRA to pay for retirement, then selling stocks may be the only way. You can't take your stocks with you, so you might as well sell stocks to fund the remaining years of your life.

The tax consequences of selling stocks in retirement can be significant. Hence, it’s best to have a combination of a Roth IRA and 401(k), if available. Roth IRAs do not require withdrawals until after the death of the owner; however, beneficiaries of a Roth IRA are subject to the RMD rules.

Can be difficult to sell stock if you retire early

When I left work in 2012 I prepared to sell some stocks to pay for retirement. However, I couldn't because I was only 34. Selling stocks then felt like I was short-changing my future wealth. We were only a couple of years out of the global financial crisis and I felt there was a lot of upside.

Instead of selling stocks, I ended up making supplemental income doing things I was curious about or enjoyed, e.g. consulting for startups, writing online. The trend continues today as it’s hard to touch principal.

But I have to imagine that once we're past 65 years old, selling stocks to pay for retirement is easier. We are more aware of our mortality as we age. Further, by then, it's easier to model our financial needs given we have fewer years to plan ahead.

Sell The Losers Or The Winners?

If you are an active investor, one dilemma you'll find when selling stocks to buy something is which stocks to sell first?

In general, winners tend to keep on winning while losers tend to keep on losing. Turnaround stories are rare, but they do happen. Although, all companies have life cycles if we wait a long-enough time.

Given losers tend to keep on losing, it may be best to sell your losers first. This way, you will not have to pay capital gains tax. Instead, you'll get to deduct up to $3,000 in investments losses for the year. Or you can deduct up to the total stock loss if you have an equal capital gain that year. Check the latest tax loss rules.

If the sale of your losers can't cover what you want to buy, then you'll have to sell some winners. Ideally, you sell enough winners with enough capital gains to offset your capital losses. This way, you'll pay zero or minimal capital gains tax.

If you're talking about selling stock in an index fund, like the S&P 500, then you have no other choice. Whenever you sell stock in the S&P 500 to buy something, accept that ~76% of the time you will miss out on future gains over the following 12 months.

This potential opportunity cost is one of the main reasons why prodigious investors find it so difficult to ever sell. That said, you should probably regularly sell your company stock to diversify.

You Don't Have To Sell Stocks With A SBLOC

If you just can't bear to sell stocks and pay capital gains taxes, then you can look into a Security-Based Line of Credit, or SBLOC. It's like a Home Equity LIne Of Credit, but for stocks.

You basically borrow money from a bank and pledge the money as collateral. Then you pay the lender an interest rate for as long as you borrow the money. If your stocks go down in value, you may be forced to pledge more collateral or sell stock to keep your borrowing percentage inline.

Plan As Far Ahead As Possible

Risk control and tax liability management are the two main reasons to plan ahead before selling stocks to pay for something.

The farther in the future your expense, such as 18 years for your newborn's college tuition, the more aggressively you can invest in stocks. The closer your child gets to college age, the more the target date fund will shift its asset allocation towards bonds and away from stocks .

As for buying a house, there's a lot more risk investing your down payment or all-cash payment mostly in stocks. Given the median home price in America is around $420,000, you'll want at least a $84,000 down payment plus a $42,000 buffer if you are following my 30/30/3-5 home buying guide.

If you invest 100% of the $126,000 in stocks and a -35% bear market hits, you won't be able to comfortably afford to buy your target $420,000 home anymore. If you want to pay $5 million cash for your dream home and you make less than $1 million a year, then you can't afford to invest the majority of your dream home fund in stocks.

I wrote a post on how to invest your down payment if you plan to buy a house within various time frames. The closer you are to buying your house, the less of your down payment should be invested in stocks.

Occasionally Sell Stocks To Live Your Best Life

In my 20s, I never considered selling stocks to pay for anything. I was committed to saving and investing as much as possible for retirement. After experiencing fake retirement for over eleven years, I'm OK now with selling stocks to pay for things. At 47, sadly, my life is half over.

In my opinion, the best way to “decumulate” is to upgrade homes. You'll enjoy living in it, especially if you have kids. The maintenance costs and property taxes will be a lot more. However, you'll be happy to spend the money on a home that brings so much value to your life.

I put decumulate in quotes because buying a perfect house at a great price can also act as an investment. The money doesn't just go to zero. On the contrary, the asset shift could appreciate as the home may appreciate over time. But I’m not buying the home to make money. I’m buying the home to upgrade our lifestyle.

There's really no point saving aggressively and investing wisely if we don't occasionally take profits and spend.

Once you're in your 40s and beyond, if your stocks have appreciated to the point it can buy you a dream home, pay for a safe car, or buy whatever your heart desires, I say go for it. You’ve already been investing for 20 plus years.

Replenish Your Stock Exposure, Create New Wealth Goals

Once you sell stocks to buy something, review your new net worth composition. After reviewing your net worth breakdown, create a new net worth goal and composition target.

In my case, if I sell stocks to buy a new house, I will start dollar-cost averaging back into the stock market with my monthly cash flow. My main goal will be to boost my net worth so that my new home becomes less than 20% of my net worth. I want to grow my stock exposure back to about 30% of net worth again.

And maybe I'll get lucky with this house purchase. There's a ~24% chance I could sell stocks before another correction hits. There's also a chance I buy this house before prices start ticking up when mortgage rates decline again. Or the opposite could happen.

Nobody knows for sure. But what I do know is that life goes on. Delaying gratification by investing should only go so far.

Diversify Into Private Growth Companies

One of the most interesting investments I'm allocating new capital toward is the Fundrise venture product. It invests in:

- Artificial Intelligence & Machine Learning

- Modern Data Infrastructure

- Development Operations (DevOps)

- Financial Technology (FinTech)

- Real Estate & Property Technology (PropTech)

Roughly 75% of Fundrise Venture is invested in artificial intelligence, which I'm extremely bullish about. The investment minimum is also only $10, as Fundrise has democratized access to venture capital as well. Most venture capital funds have a $200,000+ minimum.

Fundrise is a Financial Samurai sponsor and Financial Samurai is a six-figure investor in Fundrise funds. I'm actively building a $500,000 portfolio of private AI companies to profit and hedge against an unknown future.

Hi Sam,

I’ve been thinking about Retirement Withdrawal strategies quite a bit lately. We are 54 and 53 respectively and ready to do something else outside of corporate america… tbd what that is yet! We should be able to maintain quality of life from a 3 – 5% of portfolio for the next 40+ years.

I think I have settled on Vanguard’s dynamic spending rule, and maintain about 2 years of expenses in cash when the market is high. Withdrawals will be quarterly, and will pull from stocks or cash depending on performance over the past 12 months. I think the JP Morgan Annual Returns and Intra-Year Declines chart you have in this article really helps validate this approach for me. Thoughts on this?

Also, I’m more inclined to withdraw 4% from index funds than to chase dividends. Curious why you feel a dividend focus is better than a market return based focus?

Thanks,

Rob

As the worst stock picker of all time, I sadly have no idea what Sam is even talking about here……

What an under rated topic to talk about. As someone who has only ever bought stock to hold until “the end of time” thinking about selling stock to buy something else scares me!

Sam, I owe about $180k for my kids’ student loans [via Parent Plus loans]. My highest value stock is Apple with market value of ~ $225k. Should I sell enough Apple shares to pay off the student loans or should I drag out the 10yr payment plan using other income sources and leave my Apple shares alone? I feel angst over the thought of selling Apple!! Thanx.

It’s hard to sell Apple and pay so much in capital gains tax! I’d use cash flow or something else.

Might not sell my stock but I might use some dividends instead to buy my next vehicle. If I can make payments and use dividends to pay off a vehicle in like 2 years might go that route.

I donate my appreciated stocks/mutual funds to charity regularly

Or use my liquidity access line to buy something and not have to pay the gains and/or hedge the position , sell a call for income, etc…

Some of the best things I did was lock in cheap funding via the LAL at very low leverage amounts and not have to sell and take tax hits.

Sold stock to pay for:

Daughters wedding

Wife’s LASIK eye surgery

Bathroom upgrade in previous home

All sound like great uses of stock proceeds to me!

Great idea and you convinced me to finally pull the trigger. Just sold some today to do a renovation. So it’s in the gray area between investment (real estate) and negatively depreciating “asset” (car).

Thanks, Sam.

Good luck with the reno. I’ve kinda sworn never to do another one after my last one took over two years. Ugh.

But renos can add value! Check this post out:

https://www.financialsamurai.com/how-much-to-spend-remodeling-a-house-for-maximum-profit/

Fortunately, it’s not a major reno. Just some things that have a high ROI (garage door, etc.). We’ve already done kitchen, a bath, made an extra room (low ROI, but we love to use it), new HVAC, new floors and new roof.

I notice on the article you linked that the thing that has a highest ROI is attic insulation. Does that count lowered utility bills into it, or is it just resale value?

I would stop after work buy 4 rolls of insulation. 15 minutes to roll out in attic and done in a couple weeks. Do in cool months. Wear safety goggles, gloves, disposable coveralls to cover all skin. Take the small cost off taxes. HVAC bill lower will lower.

My goal at the moment is to keep my shares, but sell options in the same positions (covered calls and cash secure puts) to fund purchases. I count the real cash flow from the options as my passive income to use guilt free. Market has cycles so have to roll them at times but it has paid for our European vacations, buying out our vehicle when lease us up next year, and also some future home improvements.

Can you give an example of selling an option to collect the income and what happens after expiration?

Sure.

On May 4th I sold 4 cash secure put contracts of Bank of America 9/15 $23 strike price.

Premium collected $413.03 on $9,200 collateral.

Assuming held until expiration of 134 days, and the stock stays above $23 the contracts would expire worthless and the return (keeping the premium) would be 4.5% or 11% annualized.

If the price of the stock goes to $23 or below I would be assigned the shares (which I want to own at that price).

For the shares I currently own I have sold covered calls quarterly/semiannual at $32 strike which have paid $319 in total premiums.

I also collect the dividends.

Total premiums paid $732.

If the stock goes significantly below $23 or above $32 I have to decide what to do with the position which there are ways to manage it. Until than I will enjoy the rest of the summer :)

Some notes:

As my own personal rule of thumb I do not like to call cash secure put premiums as income until they are closed. I also don’t like to call covered calls premiums as income unless I have capital appreciation in the stock and they are closed. Thus when I say real cash flow that is what I mean. If I need large sum of money to buy a house this would not apply or have to be planned significantly in advance. However, for smaller purchases it can apply well as a guideline. I can’t stand when these accounts in fintwit brag about the premiums they collect when they don’t talk about the significant amount of risk they took…there are vastly different risk levels to this strategy..

I also understand it is more active management than some prefer, and acknowledge that. However for me I have found the work to be worth the additional money it has brought in over the time I have been doing so, and also have a general enjoyment of the equity markets.

Also FYI I am aligned with your guideline of active / passive management and portfolio and allocation

Good stuff! I see the stock at $28.12 today. If you’re interested in writing a guest post on selling options for income with some examples of what you do, I’d love to have it. I’m sure a lot of people can learn about the rewards and risks of doing so. You’ve already written half the post in the comments!

It’s a strategy I have not done since I lost money buying a call option on MCI Worldcom in 1999. The company went bust soon after haha.

I would love to! What is the process for submitting to you? Thanks

And u can hedge and lock in gains (or limit losses) along the way and/or play the theta game. Ah the things I wish I could still do if not a covered employees. Not allowed to buy or sell any individual stock/bond or related security….

I just retired early at 58 in February and it’s hard for me to sell my stocks to fund my retirement. I have been saving for so long, it’s hard to switch into decumulation mode. The pain is real. I know I need to enjoy my life now, but I also keep thinking about how much those investments could be worth in the future.

Let’s say your current retirement account balance was 100% in cash instead of stocks. If that was the case, how would you allocate it?

I hear you man. It’s so hard to switch from being a saver to a spender.

Take some baby steps, and then start spending more on food or clothes or drinks. Once you get comfortable with increasing spending there, you can spend more on larger ticket items. And, of course, you can always donate more as well.

Cancer arrived 2021 results in 150k alternative treatments not covered by insurance and 2 years of daily work to heal , now OK.

Glad you are doing better!