Are you looking for a 401(k) savings guide? This post will go through how much I think you should have in your 401(k) by age in order to have a comfortable retirement in your 60s and beyond. My goal is for all of you to become 401(k) millionaires before your retire.

In 2009, I helped kickstart the modern-day FIRE movement with the launch of this site. Three years later, I retired / semi-retired in 2012 after working 13 years in investment banking and maxing out my 401(k) each year since 1999. Since 2012, my 401(k), which is now a rolled over IRA, is worth over $1.6 million today. And that is with zero contribution from 2012 until now.

In addition, I've been maxing out my Solo 401(k) each year since 2012. A Solo 401(k) is for small business owners, where you can contribute both the employee maximum and employer maximum, if your business generates enough profits.

Diversify into real estate: In addition to maxing out your 401(k) for a wealthier retirement, diversify into real estate as well. Fundrise manages over $3.5 billion in private real estate investments, mainly in the Sunbelt region where valuations are lower and yields tend to be higher. With the Fed embarking on a multi-year interest rate cut cycle, there should be increased demand in real estate in the coming years. I've personally invested over $500,000 with Fundrise so far.

401(k) As A Retirement Savings Account Is Not Enough

Unfortunately, the 401(k) is one of the most woefully light retirement instruments ever invented. The 2025 401(k) contribution limit is $23,500. However, the 2026 401(k) employee contribution limit rises by $1,000 to $24,500. There's a Catch Up provision allowing those age 50+ to contribute an extra $8,000 for a total of $32,500. Those ages 60 to 63 can contribute up to $35,750.

A 401(k) is part of your new three-legged retirement stool. The other two legs include your after-tax investment accounts and your side hustles. In other words, it's up to all of us to take care of our own retirement needs and not depend on anything else.

Although the 401(k) pales in comparison to a nicely funded pension, even more disappointing than the 401(k) is the IRA. With the IRA retirement plan, you can only contribute $7,500 in pre-tax dollars for 2026. Further, you can only contribute pre-tax dollars if you make under $153,000 a year as an individual and $242,000 as a married couple. What about the rest of us?

Meanwhile, you have to make less than $161,000 a year as a single person or $240,000 as a married couple for the privilege of contributing after- tax dollars to a Roth IRA. You can only contribute the maximum $7,000 in 2024 if you earn less than $146,000 as an individual or $230,000 as a married couple.

Give me a pension that pays 70% of my last year's salary for the rest of my life over a 401k or IRA any time! At least with the 401(k), anybody can contribute.

Free Financial Checkup: If you have over $100,000 in investable assets, you can receive a free financial analysis from an Empower financial professional by signing up here. An annual review is always worthwhile as your asset allocation can shift significantly over time, and your financial situation may evolve as well. We all have financial blindspots that are worth recognizing to build more future wealth.

Average 401(k) Retirement Balances

Based on Fidelity's 2024 report, the average 401(k) balance was around $127,000. Here’s a more filtered breakdown of the average 401(k) balance by age range.

- Age 20-29: $14,600

- Age 30-39: $51,200

- Age 40-49: $120,200

- Age 50-59: $206,100

For historical perspective, according to Vanguard, another money management giant, the average participant 401(k) account balance at Vanguard was $112,572 at the end of 2022, down 20% from the close of 2021. The median 401(k) balance at Vanguard was $27,376 at the end of 2022, an annual drop of 23%.

In 2026, the average 401(k) balance by age is around $140,000 thanks to a rebound in the stock market. However, if you look at the average and median 401(k) balances by generation, they are all still pitifully low.

For more perspective, here is Fidelity's 401(k) balances by generation as of 1Q 2023. You can bump up the figures by 20% for 2026.

The Average 401(k) Balance By Age

Let's focus on what people should have in their 401(k) by age. The entire goal is to accumulate enough money in your 401(k) and other retirement accounts to eventually live financially free.

Given the median age in America is about 36 years old, the average 36-year-old should have a 401(k) balance of around $121,700. Unfortunately, $121,700 is still pretty low. But the median 401(k) balance overall is only about $35,000.

As an educated reader who is logical and believes saving for retirement is a must, I've proposed a 401(k) savings by age recommendation table that shows how much each person should have s(a)ved in their 401k at age 25, 30, 35, 40, 45, 50, 55, 60, and 65. The amounts are much greater than the average 401k savings by age in America.

We stop at 65 because you are allowed to start withdrawing penalty free from your 401(k) at age 59 1/2. Meanwhile, I pray to goodness you don't have to work much past 65. By age 65, you will have had 40+ years to save and investment already!

401k Savings By Age: How Much You Should Have

To determine how much you should have saved in your 401k by age, I've come with some assumptions that have encapsulated in a chart below. The goal is to accumulate as much in your 401(k) as possible to that by the time you can withdraw without penalty after age 59.5, you can live a comfortable retirement life.

The assumptions for the below chart are as follows:

- Low End column accounts for lower maximum contribution amounts available to savers above 45.

- Mid End column accounts for lower maximum contribution amounts available to savers below 45.

- High End column accounts for savers who are under the age of 25. After the first year, one maximizes their contribution every year to their 401k plan without failure.

- Average starting working age is 22. But you can follow the number of years working as a different guideline if you graduate later or earlier.

- $18,000 is used as the conservative base case maximum contribution amount for one's entire working life.

- No after-tax income contribution, although more power to you if you have the disposable income to do so.

- The rate of return assumptions are between 0% – 10%.

- Company match assumption is between 0% – 100% of employee contribution. $61,000 is the total 401k contribution for 2022. But in 2025, the total 401(k) contribution between employee ($23,500) and employer ($46,500) is $70,000. Hence, find yourself a good employer! Employer profit sharing can be a huge benefit for your retirement.

- The Low, Mid, and High columns should successfully encapsulate about 80% of all 401(k) contributors who max out their contributions each year. There will be those with less, and those which much greater balances thanks to higher returns.

- You are logical and not a knucklehead. Just by searching this topic, you are taking ownership of your retirement and are thinking ahead with an action plan.

Financial Samurai 401(k) Savings By Age Guide

Here is my 401(k) savings targets by age.

From the results, we can see that even after 38 years of consistent saving, you'll only have around $1,000,000 to $5,000,000 in your 401k in a realistic cycle of bull and bear markets. In other words, I believe everybody should become 401(k) millionaires by 60.

If you're just starting your 401(k) savings journey, you could get lucky and achieve the high end column with consistent 8%+ annual growth and company profit sharing after 38 years. After all, the maximum 401(k) contributions will be much higher over the next 38 years than the previous 38 years.

But it's most likely that most people reading this article should follow the middle-to-low end columns as a 401(k) savings guide. The median age in America is roughly 36. Meanwhile, the median age of a Financial Samurai reader is closer to 38.

Investing Matters Because Inflation Matters

Let's say you live for 25 years after retiring at 60. You only get to live on $40,000 – $100,000 a year on the low-to-mid end. Sounds feasible in today's dollars, but not so much in future dollars due to inflation.

If goodness forbid you live for 35 years after retiring at 60, then you can only live off of $28,571 – $71,000. If we use a 2% inflation rate to calculate what $1,000,000 – $5,000,000 is worth today, its only worth about $550,000 – $2,355,000.

We know that due to inflation, a dollar today will not go as far as a dollar 30+ years from now. Private university tuition will probably cost over $100,000 a year in 20 years. That is ridiculous since education is now free thanks to the internet.

Then there is the incredible growth of healthcare costs that is the most worrisome for retirees. For example, I've been paying $23,000+ a year in healthcare premiums for a platinum plan for my family of three. This is despite us all in good health.

Does that sound affordable for the average American household who makes $76,000 a year? Absolutely not, which is why employees should not underestimate the value of their overall work benefits.

In fact, inflation is the reason why it takes $3 million to be a real millionaire today. Make sure you own assets like stocks, real estate, and more to let inflation work for you!

Inflation Chart Of Consumer Goods And Services

Below is a great inflation chart by consumer goods and services. Medical, college tuition, food, and housing are categories that have inflated the most. This chart is a great visualization of why you must save aggressively in your 401(k) for retirement and boost your taxable investment portfolio.

To help grow your net worth, I recommend diligently tracking your net worth with the Empower Personal Dashboard. It's a fantastic and free personal finance app. Technology has come a long way since tracking our money by hand or with an Excel spreadsheet. Remember, what is measured can be optimized.

Depend On Nobody But Yourself For Retirement

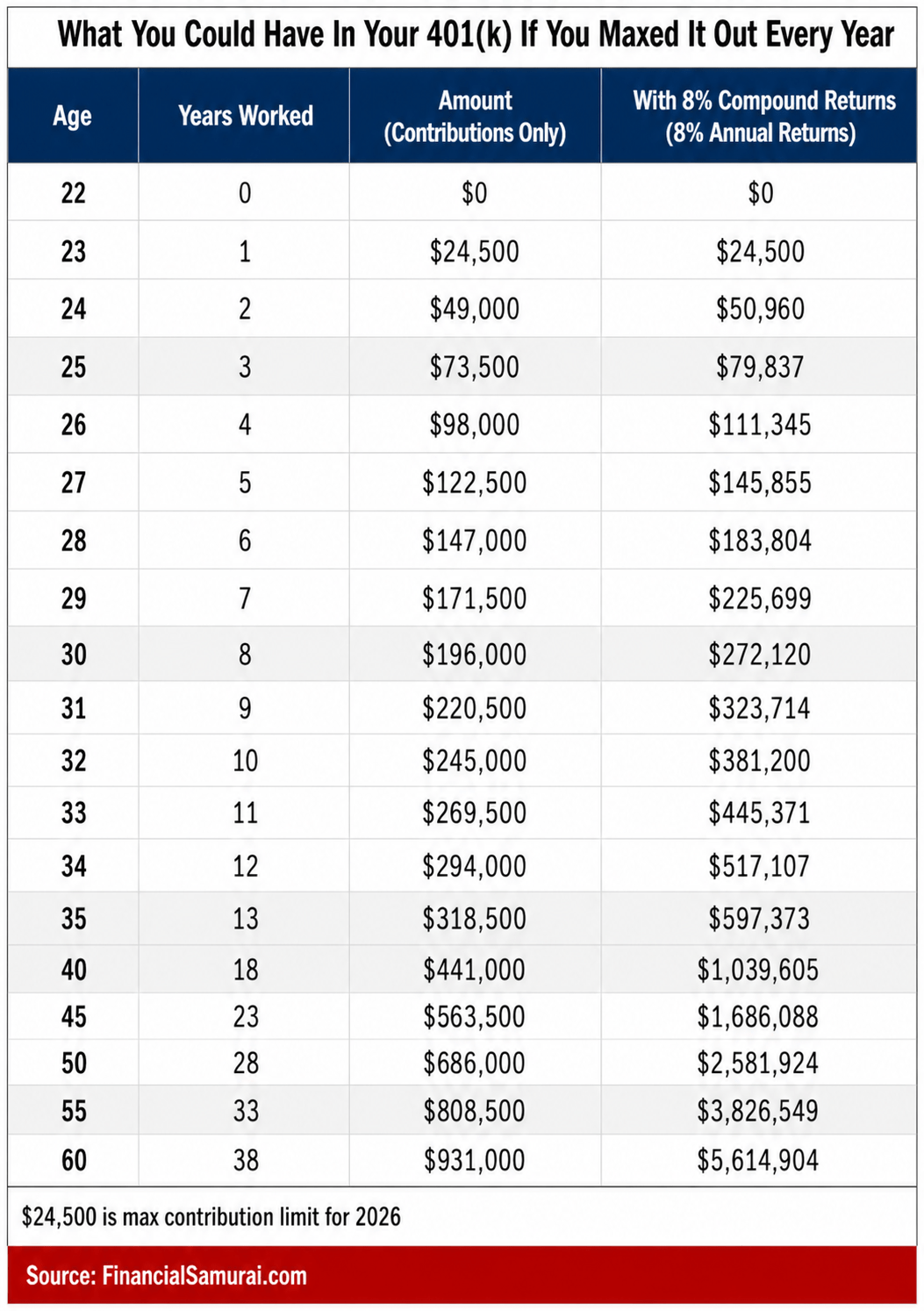

Contribute the maximum pre-tax income you can to your 401(k) for as long as you work. This is the absolute MINIMUM you can do to by on the right 401k savings by age path.

Below is a chart that shows what you could have in your 401(k) if you max it out each year starting in 2023. The right hand column shows what you would have in your 401(k) with 8% compound annual returns.

In other words, everybody who consistently maxes out their 401(k) each year will likely be a 401(k) millionaire by the time they turn 60.

After you contribute a maximum to your 401k every year, try and contribute at least 20% of your after-tax income after 401k contribution to your savings or retirement portfolio accounts.

This way, you will have potentially DOUBLE the amount in total retirement saving if your household income is $100,000 or more. If your household income is closer to $50,000, you should still see a nice 30% boost to your retirement savings if you consistently save 20% of your after tax income. Here is the recommended order to contribute to your retirement accounts.

Do Not Count On Social Security Or Government Funds For Retirement

Treat your 401k just like Social Security and write it off completely from your mind. Do not expect either accounts to be there for you when you retire. It's just like how you should never expect the government to ever help you when you're in need.

Just imagine 30 years from now, the government deciding to raise penalty free 401k withdrawal to age 75 from 59.5? Unfortunately, you need the money at age 60. Because you withdraw, the government imposes a 30% penalty on top of the taxes you have to pay. Don't think it can't happen. Expect it to happen!

Taxable Investment Portfolio Is Key

The only thing you can count on is after-tax money you've invested or saved. This is why after maxing out your 401k, it's good to open up an after-tax brokerage account. Consistently contribute a percentage of your paycheck each mont into your taxable investment portfolio. I recommend at least 20%.

Your goal should be to then build as many passive income streams as possible. The more passive income streams and active income streams you have, the more financially free you will be.

Challenge yourself to raise your after-tax and 401k contribution savings percent to possibly 50%. It won't be easy. But if you practice raising your savings rate by 1% a month until it hurts, you'll find it easier than you think.

A straightforward way to maximum savings is to make your 401(k) maximum contribution automatic. Save every other paycheck for the rest of your working life.

Max out your 401k and save over 50% of your after-tax income for at least 10 years in a row. If you do, you will be financially free to do whatever you want!

Recommendation To Growing A Larger 401(k)

Now that you know what the appropriate 401(k) savings by age is, it's time to manage your finances like a hawk. To do so, sign up for the Empower Personal Dashboard. This top-rated, free personal finance app gives you a clear, real-time view of your entire financial picture.

You can track everything from spending and savings to investments and retirement planning. Empower is a trusted financial services company that helps millions take control of their money and manage their wealth easier.

In addition to better money oversight, run your investments through their award-winning Investment Checkup tool. It can show you exactly how much you are paying in fees. It helped me realize I was paying $1,700 a year in fees I had no idea I was paying. Further, it can give you great insights into your asset allocation.

After you link all your financial accounts, be sure to check out Empower's Retirement Planning calculator. It securely pulls in your real account data to give you a clear picture of your financial future. Definitely run your numbers to see how you're doing and to how you can improve your finances.

To track my 401(k) savings by age guide you must max out your 401k each year. With investment returns coupled with company matching, you'll be amazed how much you can accumulate over the years.

Free Financial Analysis Offer From Empower

In addition, if you have over $100,000 in investable assets—whether in savings, taxable accounts, 401(k)s, or IRAs—you can get a free financial check-up from an Empower financial professional by signing up here. It’s a no-obligation way to have a seasoned expert, who builds and analyzes portfolios for a living, review your finances.

A fresh set of eyes could uncover hidden fees, inefficient allocations, or opportunities to optimize—giving you greater clarity and confidence in your financial plan.

I’ve been using Empower’s free financial tools and speaking with their financial professionals since 2012. From 2013 to 2015, I also consulted part-time at their offices while the company was still called Personal Capital (prior to its acquisition by Empower). As both a longtime user and affiliate partner, I’m genuinely pleased with the value they’ve consistently delivered over the years.

The statement is provided to you by Financial Samurai (“Promoter”) who has entered into a written referral agreement with Empower Advisory Group, LLC (“EAG”). Click here to learn more.

Build More Wealth Through Real Estate

In addition to investing in stocks and bonds through your 401(k), I recommend diversifying into real estate. Real estate is a core asset class that has proven to build long-term wealth.

It's important to own a tangible asset that provides utility and a steady stream of income. Unlike stock values, real estate values tend to be much less volatile. Use real estate to generate passive income and distributions before age 59.5 which is when you can withdraw from a 401k penalty-free.

My Favorite Private Real Estate Platform

Take a look at Fundrise, my favorite private real estate platform. Fundrise runs over $3.5 billion in assets for almost 400,000 investors today. Its funds focus on the Sunbelt region, where valuations tend to be lower and yields tend to be higher.

I've personally invested over $1,000,000 in real estate crowdfunding across 18 projects. My goal is to take advantage of lower valuations in the heartland of America. My real estate investments account for roughly 50% of my current passive income of ~$320,000.

Order My New Book: Millionaire Milestones

Finally, if you’re ready to build more wealth than 90% of the population, grab a copy of my new USA TODAY national bestseller, Millionaire Milestones: Simple Steps to Seven Figures. With over 30 years of experience working in, studying, and writing about finance, I’ve distilled everything I know into this practical guide to help you achieve financial success.

Here’s the truth: life gets better when you have money. Financial security gives you the freedom to live on your terms and the peace of mind that your children and loved ones are taken care of.

Millionaire Milestones is your roadmap to building the wealth you need to live the life you’ve always dreamed of. Order your copy today and take the first step toward the financial future you deserve!

Follow my 401k savings by age guide. But in the meantime, also build a passive income portfolio so you can live a better life today. Given you cannot withdraw from your 401k without penalty until 59.5, it is your passive investment portfolio that matters even more.

How Much Should I Have Saved In My 401k By Age is a Financial Samurai original post. Everything I write is based off first hand experience because money is too important to be left up to pontification. Join 65,000+ others and sign up for my free weekly newsletter as well. In 2009 I launched Financial Samurai and started the modern-day FIRE movement. Then in 2012, I retired at age 34 with about $3 million.

I’m 55. $5m+ in 401k/IRA/HSA. I didn’t do anything special except be consistent. Slow and steady will get you there. Will start converting to Roth when I retire at year end to address looming RMD bomb…

$5 million is impressive for all tax-advantaged accounts. What is your total net worth? Given I wanted to retire early, I focused on building my taxable portfolio and rental properties, so I’ve got less than $5 million in tax advantaged at 49 today.

Related: Taxable Investment Amounts By Age To Retire Comfortably

You not factoring in the impact of severe emotional trauma in the family of origin (in my case, sudden murder of my mother at work by a psychotic patient, when I was a child) and my remaining family never recovered after that). I always worked, but I never achieved what I could have achieved if this trauma did not happen, attested to my several psychotherapists I consulted. People are not machines. What they can do is tempered by the conditions they find themselves in. In most cases, their conditions are a function of poor or unwitting choices. And sometimes, what happened in your life had nothing to do with the choices you made, as in my case.

Thanks for sharing, and sorry for the trauma you experienced as a child. The work of Gabor Mate has been insightful to me for helping address childhood issues as well.

As a reader, I’m glad you’ve come to my site. It’s never too late to start or change.

Hi Sam,

Should I adjust your target 401(k) table for a married couple? Should I just double the amounts or is there a scale factor you would suggest applying?

For context, I am 42, married, have 3 young kids and live in a HCOL area. I have a stable corporate executive job. I have $1.5M in my own 401(k) and additional $700k in my IRAs. My wife also has her own 401(k) and IRAs.

Thanks for your input and all of your articles.

You can definitely double it if both partners work, or multiply it by 1.5 times there’s one Partner works halftime.

Or you can just use this guide for your entire household tax-advantage contributions.

You may enjoy this post: The average net worth for the above average married couple

Reader, first-time poster. 59-year-old IT worker in a public school in a LCOL (and low pay) medium New England town. No debt. Rental income.

What do you folks think of this plan? My annual retirement needs are $60,000/yr. My wife is younger and makes about 40k, no benefits. Let’s say I can hit a million in Roth by 62. I’m an experienced trader in the tech I use and understand, and have a good record a bit above the S&P. I recently discovered that if I take SS at 62, my dependents under 18 and my spouse also get some benefits. I have two kids, one born in 2012, the other in 2015. So, several years of benefits, plus it might be beneficial for financial aid in college. I “Lean FIRE”, keep teaching at the local community college and doing some side gigs, with rental income, a very small pension, so I’m only taking a max of 2.5% out of the Roth a year, until I’m 65 or 66 and both kids are out of the house, and I can get Medicaid.

Welcome, and thanks for sharing your background and plan — great to have you here!

You’ve clearly thought this through. Hitting $1M in your Roth by 62 with no debt, rental income, and a small pension puts you in a solid position, especially in a lower-cost-of-living area. The Social Security family benefits angle is a nice insight — not many realize how meaningful that can be with dependents still under 18. That could definitely help bridge the gap before Medicare kicks in.

I also like that you’re keeping some earned income through teaching and side gigs. It keeps you engaged, provides flexibility, and helps stretch your Roth further. A 2.5% withdrawal rate is very conservative and gives you a nice cushion if markets dip or expenses rise.

Overall, this looks like a thoughtful “Lean FIRE” approach with multiple income streams and optionality. Curious — how stable is the rental income, and do you plan to keep managing the property yourself after 62?

Don’t forget to subscribe to my weekly newsletter as it helps you keep focused in achieving financial freedom sooner.

Cheers

Hi – I am 59 with 1.7 million in my 401k and my mortgage will be paid off in one year. Starting at 62 I will receive 4100 per month from Social Security. Do i have enough to retire now?

Most likely, if your SS payments and investment income covers your living expenses.

Check out my posts:

The Proper Safe Withdrawal Rate In Retirement

Misconceptions About The 4% Rule

This is a very informative article! I especially appreciate the emphasis on not relying solely on a 401(k) but also diversifying investments. Retirement planning is a long-term game, and the earlier you start, the better.

Great stuff here, I have been reading since 2010, while everyone’s journey is different, I like to take what I can and apply it to my own journey. 43 years old 6m in investment accounts, 1.4 m in 401k accounts, homes paid for cars paid for, zero debt. Bottom line I think people save too much for retirement and get in a rut of always comparing and wondering if they can retire that they don’t enjoy life while they can. My grandfather passed away at 93 he had enough left to pay for a casket and buy everyone in the family (4) a coffee. at the end of the day don’t be the richest guy in the graveyard.

Are you finding it difficult to spend down your wealth? It’s definitely important to be intentional. Otherwise, it could easily compound at a much faster rate than you can spend.

Mid-40s is definitely a good time to start IMO.

Related: Best Ways To Decumulate

Hi Samurai, long time reader, first time poster. I feel great comparing my finances to your charts I am definitely above average. 37 years old, $650,000 TSP, $300,000 Vanguard funds, $70,000 savings accounts. Net worth maybe 1.3 million. Own my home, no kids, have a lot of toys, federal pension starts when I retire in 9 years. I need advice, when should I get a financial advisor/fiduciary? I have been making decent gains for my whole career investing by myself, I think I am going to get more anxious the closer it gets to retirement because I might be missing important rules. What do you suggest?

Hi Brandon,

Since you’re doing well so far for so long, you can probably continue to be a DIY investor and planner.

However, it’s always nice to get a second opinion. Empower is doing a promo where you can get a free financial checkup with one of their professionals. They’ll even send you a free $100 Visa gift card via e-mail if you do your two calls with them before November 30, 2024. You just need over $250,000 in investable assets, which you do. You can schedule your call here.

Here’s my experience speaking to an Empower professional back in 2013, which helped me elucidate a blind spot and boost my net worth by an extra $1 million since then.

Finally, here is my consulting page, which I do not highlight anywhere at all due to the demand and my limited time.

Cheers

I am on the low end of your chart, but feel I am on the right track. I am 49 with 500K in my 401k. I also have about 100K in other stock and pensions. I have my primary home paid off and own a vacation/retirement home. I have more equity in my primary home than I owe on my second home. I plan to work as long as I can. I am active am healthy. To me retirement is getting all my children through college, having no mortgage, and working a less stressful job. What advice do you have for me as I get older to maximize retirement while still working?

I would actually take advantage of the Empower promo and schedule a free consultation with one of their professionals. They will go through your goals and existing portfolios in the first session and make suggestions in the second session. After the second session, they’ll even send you a $100 Visa gift card via e-mail if you finish both sessions before November 30, 2024. I’m not sure when their next promo is. You can schedule your call here.

Here’s my experiencing speaking to a financial professional. Ultimately, he made me realize I was overly conservative and encouraged me to put my cash to work. The actions back then have turned out very well today.

Having the goal to get your kids through college and pay off your mortgage are great goals.

Theses numbers are manageable, especially when I reflect on my own personal journey. The key is time in the market, not timing the market. Now that I’m 40 and look back, I’m so glad I started at 22 and prioritized maxing out at a young age. My retirement savings are on the upper end of the FS target range (>$750K), so again, very manageable with time and discipline.

Could not agree more with what you said, Steve. Time in the market is the most important aspect by far, and prioritizing saving aggressively when you are young.

The only word of caution I would throw out there is that there has been a huge tailwind from increasing valuations since you started investing at age 22 (presumably 2006). At that time the 2008 crash had not yet happened, and yet valuations now are more than double where they were in 2006. All this means is that we should count ourselves fortunate for the returns over the past 18 years, while also realizing that a large portion of it came from multiple expansion, which by definition is a non-reproducible factor.

First off, I see the 36 year old median age. Yes the median age is 36, but 2 year old kids do not invest. You need to use the median “working age”, not median age. Even then, most 18 year old’s and/or up to mid 20 something year old’s do not even make enough to start investing yet, so you are looking at more of a late 40 something “investing age” median. Maybe then some of these numbers would start lining up a “little” better. Then go further in where he says max out your 401 k and then put another at least 20% toward non 401k retirement investments, at a 100,000 income. So, 22,500 401k + 25,000+ aprox taxes + another 10,000+ non 401k retirement investment, brings this family down to 40,000ish to live on yearly, talk about investment poor. you are investing so much that you cant even live comfortably in the mean time. Then they go and say 50,000 incomers should try to do the same as best as they can, but will only see about a 30% gain in retirement as apposed to the 100,000 earners. Of course they would see less, as they make less, but that still begs the numbers, 50,000 – 22,500 401k – 10,000ish taxes – 3,500ish non 401k retirement “20%” investment =14,000 left to live on. Come on now. How the heck is someone supporting there family on 14,000. Like anyone making 50,000 can even start investing, more or less investing that much like they are suggesting. Even if you could live off these minuscule amounts after investing, what do you need this 5,000,000 retirement fund for to have a 250,000+ per year retirement, if you lived off 14,000 to 40,000 your whole life to get to that point. If you can live off that little your whole life, it looks like that’s all you would need in retirement. Just total ridiculousness with these figures. Just figure out your must have “needs”, then your must have “wants”, then you would like “wants” and figure what each one of those would come to on a certain basis (monthly of yearly), and do your best to set aside enough to cover those for as long as you think necessary. Anything more is extra and nice, but not a game changer for a happy retirement. As none of these articles ever tell you, nearly 60% of the people who retire, do so on SS benefits and what little savings they have in the bank (less than 20,000), and most of them live just fine off that. No they cant travel the world, but do you have to to be happy? Any retirement investments at all puts you in the top 40ish %, and more that 100,000 puts you in the top 30% of most. Why on earth do you need 5,000,000+.

Live long, Live well, Be happy,

Some people retire in a VHCOL city (NYC, LA, SF) where they will need 5 million or more.

There is always one glaring issue with these 401k balance by age reports. There are very misleading and don’t paint the whole picture. Many people have several 401K accounts or rolled over 401ks to IRA accounts from a previous employer. During my career I have worked for several companies in which I have three 401k accounts, a Roth IRA that was a rollover from a Roth 401k account, and a traditional IRA that was also a 401k rollover. Some of these accounts fall right in line to what the median 401k balance is. If you cherry picked the one 401k with my current employer you would say I was way behind the curve. There is no way Fidelity or Vanguard can truly measure an individual’s retirement savings because they don’t have access to all of a person’s Roth/Traditional 401ks, IRAs, 403b, pensions, ESOPs, or anything else I forgot to mention. Because of this, it is safe to say the median savings for most people’s retirement is much higher than these Fidelity and Vanguard average/median 401k reports are. In which we all would agree it what all of your retirement accounts combined is what matters.

Completely agree, Ike.

This annual report by Fidelity is one of the most annoying things ever. Grr. They don’t disclose their methodology at all. I have 5 Fidelity 401k accounts and an IRA, and I’m betting that Fidelity only looks at _one_ of them. And no, Fidelity – I am _not_ going to roll over anything – I like it just like that :-)

Furthermore, they completely miss spousal account totals as well. To make this “Report” useful, Fidelity should have an opt-in annual survey page where clients can describe their entire retirement portfolios, even those outside of Fidelity (e.g., Vanguard).

I feel like Fidelity _wants_ the figure to be low to drum up business with click-bait headlines and get more clients investing with them. Why wouldn’t they want to show much higher balances that reflect reality?

True. But you can take the data for what it is and compare your combined 401(k)s (rollover IRAs) to the average 401k balance by age figures, or take the average of your 401ks and compare to make the comparison consistent.

The other good thing is that due to rollovers, American workers are in better shape with their retirement savings than the numbers indicate.

On my planet, there are only 2 workers.

They each change jobs every year. Worker 1 always maxes out their new 401k contributing $20K per year, and Worker 2 never contributes anything. 10 years in, Worker 1 has 10 old 401k accounts, Worker 2 has nothing

Fidelity publishes a report saying the average balance 401k balance is only $10,000 (they average Worker 1’s active $20K account and Worker 2’s zero balance account), completely ignoring the fact that Worker 1 has $200,000 in prior 401k accounts.

This annoys me on my planet, as well :-)

So… would part of the solution be to also disclose how many accounts exist? If you learn Planet X has two beings, and 10 accounts with only a mean of $10k, would this not enlighten us to a closer idea of the scope of overall savings?

All accurate observations. Even if they could collect and condense based on SSN, the various brokerages and investement firms have no transparency into each others’ holdings. Nor should they — what an invasion of privacy for us account holders.

However, if their reported numbers are any motivation at all for a culture that is spoon-fed from before birth into mindless consumerism and wastefulness on just about every level — motivated to have some kind of positive personal behavioral adaptation to save/invest more for themselves, that remains a ‘good thing’.

This particular site is geared toward the affluent. The fact of the matter is — to make a profound difference in the US (my myopic universe as I have no knowledge of how the other 7.4Billion of us live), the bottom half of earners would so benefit from not only the balance-by-age reporting, but how to get out of the paycheck-paycheck treadmill and see their own balance sheet improve. These reports could be broken down by salary/gross income. And educational sites like Sam’s, geared toward the earners under the median income level, would make a profound difference. They likely don’t have multiple 401ks, rolled over IRAs, perhaps have never heard of a Roth, and a single account measured against Sam’s posted number means something very much more real.

I just talked to a 40 something hedge fund guy with a wife and 3 kids.

He was saying how even with over 1 million in pre-tax income, he struggles to make ends meet.

A huge house, and a large second home. Private school and extravagant activities for the kids. 3 high end destination vacations a year. Spending a lot on experiences.

Now granted this guy is living rich, very rich, but is in fact poor.

But that still got me thinking, how much do we really need to retire “early” or “early-ish”

I0 million? 15 million? Now after talking to him, 10 is starting to sound a bit dicey/lean.

You know the math, you know how you live, so why does it matter what this 40 something does with his money. He might need $15M to live how he does if he wants to retire in his 40’s and maintain his lavish lifestyle.

You need to ask yourself what your expenses are likely to be and what kind of buffer you want. Apply the 4% rule as a starting point and see how it plays out. Personally I feel I need $5M in investible assets but we live pretty sensibly, have no debt and our joint incomes are less than half of what your friend brings in.

That’s just it, 15 million isn’t enough for the guy. The guy is SPENDING all of their 1 million + income a year. If he were to retire, he would need easily 40 million, minimum

But that got me thinking, if i were to retire, I would have a lot more free time on my hands. And I might need a lot more money that i currently assuming.

right now i am like making money full time. I barely have enough time to spend. but if spending money became a full time job (in retirement), it would be hard to know how much i will need.

Well I’m retired (49) and my income has dropped about 50%. My wife works and I have youngish kids so I’m busy with family stuff, but honestly at 49 I have everything I want. I’ve always felt guilty spending money frivolously and was able to retire because I’ve always thought carefully about what I spend and saved a good percentage of my income. Just because I’ve retired doesn’t change that, and because I don’t have the cash flow, I might be a little more careful. Also consider that once you’re retired you technically don’t need to save so you don’t need the level of income you have while you’re saving for retirement.

I understand what you are saying. And I suspect i will behave more like you than that family i am telling you about. However, I have ALWAYS worked my entire life. I have never tried retirement. If i retire today, i would definitely be retiring EARLY. So i just don’t know if i would just sit home. Maybe I would acquire a taste for family vacations.. Maybe I would want a second home, a RV, or a yacht. In any case, thanks for sharing your experience, this is some thought provoking stuff.

This is such a fairy tale, annual compounding of 8% every single year, that is not reality, and you know it. People don’t believe 8%, yeah it’s in all MBA text books, opportunity cost of funds blah blah.

The key number these days is $300K, once you’ve accumulated that quantity, that is an inflection point for a reasonable compounding effect and it should take you a minimum of 10 years to accumulate that figure if you live in the US, that is 100% doable.

Now what about having a family? no kids, is fine no future for America, you know you need kids for our country to survive–for our economy to thrive–for all of us to get those nice returns, did you frigging forget that detail. Make sure you put in two kids minimum in your little write ups from now on; don’t encourage people to stop having families for our Nation’s sake , look at the big picture, bro.

Something else to consider: the best move I made with the 401K is to take out a loan against the 401k to buy Real Estate, I was patient and spotted the opportunity; you can too; I did not get lucky it was hard work and worked the right relations. You don’t have to invest in Real Estate today, invest on a business, etc, get those funds out the 401K in the form of a loan if the option is available to you and deploy the capital to work into other investment assets, the 401k is a low-low performer.

I’m not sure why you think 8% as a fairytale when the historical return for stocks is 10% and I’m not even including company matching and profit-sharing.

People mostly let their 401(k) investments ride and don’t touch them until after 59 1/2.

I do agree with you on the $300,000 assertion where you start feeling financially independent. https://www.financialsamurai.com/minimum-investment-portfolio-balance-to-start-feeling-free/

I wouldn’t borrow from my 401(k) to invest in real estate. Instead, I would invest in real estate using my savings beyond 401(k) contributions. I think it’s important to compartmentalize.

Why do you diminish Social Security so much? The vast majority of American’s are living and will live entirely off her Social Security income. That’s not going to change or everyone would revolt and burn down the White House. They almost did it just because Trump wasn’t re-elected… so imagine what they’d do if they stopped sending out the Social Security checks. My MIL gets about $3000 a month in social security, her income and some of her deceased husbands benefits. Home is owned outright with low tax basis. For someone that hangs out around the house, watching the news, and feeding her dogs… she doesn’t really need much else.

I feel like once you are in your 60s… You kinda can revert back to living like you did in your early 20s cost wise… just with higher medical expenses. But if you don’t have much besides Social Security in terms of income…. Your medical costs are gonna be heavily subsidized for the rest of your life. Needing long term nursing home care is really the only financial wild card…. But even if you had a lot of money.. luxury nursery home care would eat at your wealth rather quickly. Also who really wants to keep living if you are literally in need of 24/7 long term care.

I’m 46 years old and have heard for over 25 years that Social Security is underfunded. Therefore, I have just learned to expect less or expect nothing actually. As a result, this has motivated me to earn as much money as possible and build more wealth for passive income because I feel like an only depend on myself.

I also interviewed many retirees who do collect Social Security. I asked them if they bothered saving and investing in a taxable portfolio or building a rental property portfolio. They said no because they had a pension or Social Security.

That’s fine, but they had to work until past 60 years old and their retirement spending is capped as a result.

If Social Security is there for me in 20 years, I will treat it as a bonus and spend it or give it away every month. And if it’s not there, then, no problem because I never counted on it in the first place.

This is the way.

I agree, this is a good way to look at it… unless you are saving so much in excess of what you will really need and not enjoying life becasue of it while you are young and able.

The top SS payout, which most of your readers will be receiving after 30 years of work or around age 50ish. That top line amount is almost $5000 and increasing with inflation every year…. That’s nearly $60K in income JUST from Social Security. If they cut that 25%… (which is the MOST it would need to be cut to keep in solvent for decades)… You are talking $45K a year. At the very least that would cover a ton of living expenses for your average Senior Citizen before touching any other savings. And as much as fear mongering there is.. It’s not going away. Every paycheck cut in the US… 14% is going into the pot. The only way it goes away is if Republicans privatize it and invest it all in Bitcoin and we lose it all. haaha.

Sam, in your “Financial Samurai 401(k) Savings By Age Guide” chart. Are these goals by age for a single person or are they for a household? For example, at age 45, does the mid-end of $750K mean that 1 person should have saved that or does this suggest that a married couple combined should be at the $750K mark?

It can be either. I say it’s a recommended household target. A household of income earners can consist of one or two people. It’s generally easier to build more wealth with two people that one.

Hey FS. I’m new here and looking at your projections do motivate me but also concern me. I need feedback. I’m currently 33 with about 27k in my 401k. I recently changed my contribution to 15% and the employer contributes 5 percent, so total contribution is 20%. My question is, do I need to contribute more to have a safe retirement because I only make 70k a year. Or, do I need to move up in my company because maxing out my 401k at 70k is somewhat challenging?

Are you in the US? Assuming so: When do you want to ‘retire’? Are you also maxing out a Roth? Are you using a HSA as part of a retirement toolset? Is there a spouse/family? Is spouse employed – or maxing out a Roth or both. What is your cost of living? Do you expect raises in the future (and you’ll shunt them into investments)? Do you have debts, an emergency fund, living as frugal as you desire? If 15% gets you to retirement at 65, would 30% get you to retirement at an earlier age? Is moving up in your company desirable (is a raise worth added stress)? Any additional contributions now will compound deliciously over 30 years – but at what cost to your current life/happiness?

I think you should try to do both. If the amount of money you’re saving each month doesn’t hurt, I don’t think you’re saving enough.

The max 401(k) contribution in 2024 is $23,000. Have you tried to save that much before? If not, it will hurt, but you will adjust. Once you’ve got your savings down automated, you’ve got to focus on boosting income as much as possible.

Here’s are relevant posts you might like:

Achieving Financial Freedom On A Modest Income

Contributing To Your 401(k) Is A Choice

At 33, you are still very young and have a lot of time left to save and invest. GO FOR IT! Your older self won’t regret it.

Your numbers are too high if for those of us who have a USG pension, like your parents did. The Foreign Service pension is 1.7% of the average of the top 3 salaries per year of service, up to 20 years, then 1% for every year after 20 years of service. The CS pension is 1.1%. Plus, lifetime health insurance. I have just under what you estimate, but I also have a lifetime annuity of several thousand dollars a month. My spouse, on the other hand, has half of what he should have according to your chart, but he immigrated to the US in his 30s and didn’t work for several years as a dependent overseas. We’re not worried because he will get his own pension when he retires — less than mine, but still plenty between us. I know you’ve written articles on the value of pension and I try to tell everyone, especially my kids, that pensions are the gold standard.

Thanks and congrats. See: How To Calculate The Value Of A Pension.

Hi Financial Samurai- I am 30 years old and have $300K in my Roth 401k, 0 in 401k. I have payed taxes on 100% of the 401k (Employer match and after tax contributions). How should i benchmark vs. the charts. Should i assume if it was a pre-tax 401k I would pay a blended tax rate of 20% in retirement so i would have a pre-tax $375K 401k?

I think taxes will go up long term but want to make sure I comparing same numbers.

How accurate can this be? I’ve had multiple jobs over the years and each time roll the 401k into my personal IRA then start a new 401k at my new employer. So I might show up as having a small amount saved in my 401k, meanwhile in reality I’ve saved hundreds of thousands but it’s been rolled into my IRA.

Agreed, and the average 401k calculation seems to be a nearly useless statistic since I also have 5 IRA accounts (one from prior employers and a Roth) plus a 401k and if you take the average of my 401k+IRA accounts, it is only 1/6th of what I have in total. They need to track the total of all retirement accounts associated with a person not individual accounts.

So it means the average total 401(k) balance is probably higher, and Americans are saving more for retirement than this data shows. All the more reason to follow my 401(k) by age guide.

Many advisors says to save for 80% income replacement in retirement. I just don’t see myself needing that kind of nest egg. I’m currently tracking at 62% income replacement on earnings of $180k/year.

When I look at my monthly expenses & debits, 70% of those I would not have in retirement; including 401k contributions, Mortgage P&I, 529 college savings, daycare & school expenses, life insurance (?), plus excess cash for savings. Assuming my retirement savings at least keeps up with inflation, why would I need 80% income replacement at retirement?

Greetings, would you please add the years as a column in the table titled “what you could have [had if you’d maxed out your 401K]”. Next time you refresh this table, it gives us a sense of baseline and what we should be aspiring to if we “max” against that time frame.

I use the chart as a baseline to see how we’re personally doing – are we above or below the max trend. Granted where you work and employer match makes an impact, but it would be nice to know how things could have worked in the theoretical max — by year.

Thank you!

It’s actually flexible for any year based on the number of years you’ve worked or your age.

It’s odd to have a savings chart that doesn’t take into account average working income. Isn’t it impossible to know how much one needs to retire on, without calculating what the retiree was living on while working?

My parents retired early and are doing well. Living in their paid off house, gardening, walks around the neighborhood twice a day, free weekend outdoor concerts at the park, senior golf discounts ect.

My wife and I have a little more expensive tastes and plan to travel more in retirement… so we are being more aggressive. We also want the freedom to follow our only daughter wherever life takes her. So obviously we’ll need more income and are saving accordingly.

So I always wonder about these avg/median 401k balance surveys. Like how are people gonna retire off of that, they’re always soooo low! Like maybe people just have a lot of 401ks with different financial institutions or something? My 401k balance is pretty low, but that’s because I move companies quite a bit and rollover everything into an IRA. So my IRAs make up the bulk of my net worth.

Simple answer? They won’t. Until this country gets their collective heads out of their a**es, proceeding generations are going to continue to “have it worse” than the generations that came before them. If you think most millennials or Gen-Z’ers are going to be able to retire, without companies offering pensions, or with their pathetic 401K’s, you got jokes.

The collective 1%’ers who find this blog are completely out-of-touch with the struggles of most average Americans.

You hit it on the head. The 401k was meant to supplement the Pension for higher paid workers, not replace it entirely. Anyone that can hit these numbers without living out of a van eating top ramen is completely out of touch with 90% of the workforce. If you aren’t a highly successful entrepreneur, STEM worker, or Finance bro, these numbers are literally impossible to meet. I can max out my 401k and roth ira while not being completely broke, but I know that i’m a rare case. Like you said, when you have been given the knowledge and tools/upbringing to work hard and succeed, its hard to relate to many people. It isn’t just knowledge and work ethic, there’s a systemic issue in the USA.

It takes discipline to invest for life sustaining income starting in one’s 60’, but it is possible. If you don’t believe so you haven’t read much into financial literacy. One can make minimum wage for 40 years and simply save 10% of their income and retire a millionaire. That’s a fact.

It is a known fact that one cannot live off of minimum wage today (contrary to previous generations where living off of minimum wage was not only possible, but also the literal goal of the federal minimum wage implementation). With that in mind, please explain how said fictional minimum wage worker can “simply save 10% of their income and retire a millionaire.”

Clint, both Mike & Mike are highlighting the documented systemic issues in this country that affect 90% of the population. While you’re busy playing pull yourself up by the bootstraps, it would behoove you to acknowledge that many Americans simply don’t have shoes. That is a systemic & moral failing of the self appointed richest country in the world. A better use of time would be a two prong approach of both fixing the systemic issues and teaching personal finance.

I am 53 and started saving late in life. I didn’t start making decent income until my 40s. I only have about $150-175k saved in retirement and other liquid accounts. I want to invest in real estate. My parents dabbled a little in it and made out very well. I have about $30k – 50k to invest and wondered what you might suggest if you were in my shoes?

John, truly this is a ‘better late than never’ scenario. I would suggest joining your local REIA groups and partner with someone looking for an underling to mentor. You can bring cash to the table, or energy to do the grunt work, or both. You can join BiggerPockets.com and contribute/learn in the forums as well. Real Estate is get-rich-slow for the most part, a lot like paper investments. But if you still have a W2/1099 job, you can parlay that money into inexpensive buy/hold investments using the BRRRR methods (before the term was popularized, it was simply buy what you can afford to remodel/upgrade, rent it out and refi to release the money for leveraging another property). Yes, the housing market is bloated in pricing now so deals are harder to come by. Yes, it will correct as all things do but will it be this year or 2027? And yes, you can make money if you do your homework.